Throughout 2026:Q1, family debt balances elevated barely, by $18 billion, to succeed in $18.8 trillion, in line with the most recent Quarterly Report on Family Debt and Credit score from the New York Fed’s Heart for Microeconomic Knowledge. Amid upticks in mortgage, HELOC, and auto balances and a seasonal decline in bank card balances, pupil mortgage balances remained unchanged. Nonetheless, the share of pupil mortgage balances late elevated, nearing pre-pandemic ranges at simply over 10 p.c. On this submit, we deal with which debtors entered default on their federal pupil loans over the previous two quarters. We discover that the common borrower getting into default is sort of 40 years outdated, was not late on their pupil loans previous to the pandemic, and is extra prone to reside within the South. Whereas defaulted debtors usually tend to be late on different types of debt, the general scope of pupil mortgage defaults remains to be comparatively low, suggesting that fears of broader contagion to different credit score merchandise are untimely.

| Methodology Notice: This quarter’s report additionally introduces a change within the credit score rating measure we use in a number of of our charts. Beginning with this report, the figures and evaluation that rely on credit score scores will shift to utilizing VantageScore 4.0, as a substitute of Equifax Danger Rating 3.0. We offer some context on how this shift will impression the noticed inhabitants with credit score scores and our evaluation in this technical paper. |

The (Gradual) Return to Compensation

On the onset of the pandemic, pupil mortgage funds had been paused, and rates of interest had been set to zero p.c. As a result of many extensions of the fee pause, debtors weren’t required to make funds for over three years. The pause formally led to September 2023, when funds resumed and curiosity started accruing once more. Most debtors had been anticipated to make their first fee in October 2023. Whereas funds had been required, throughout a 12-month “on-ramp” interval via October 2024, missed funds weren’t reported to credit score bureaus.

As we famous in our earlier submit, the primary pupil mortgage delinquencies had been reported on credit score experiences throughout 2025:Q1. Since then, over 17 p.c of pupil mortgage debtors have fallen a minimum of 90 days late on their funds a minimum of as soon as. Because it takes 270 days of missed funds to enter federal pupil mortgage default, 2025:This fall was the primary quarter when new defaults started showing on credit score experiences. We estimate that roughly 1 million federal pupil mortgage debtors defaulted throughout 2025:This fall, with a further 2.6 million debtors defaulting throughout 2026:Q1. Notice that debtors within the now-defunct SAVE reimbursement plan entered reimbursement, however had been put right into a forbearance through the on-ramp attributable to litigation. Only a few have re-entered reimbursement since missed funds had been reported to credit score bureaus. This delay implies that a second wave of defaults would possibly emerge as these 7 million debtors attain the nine-month mark within the reimbursement interval.

Who Is Getting into Default?

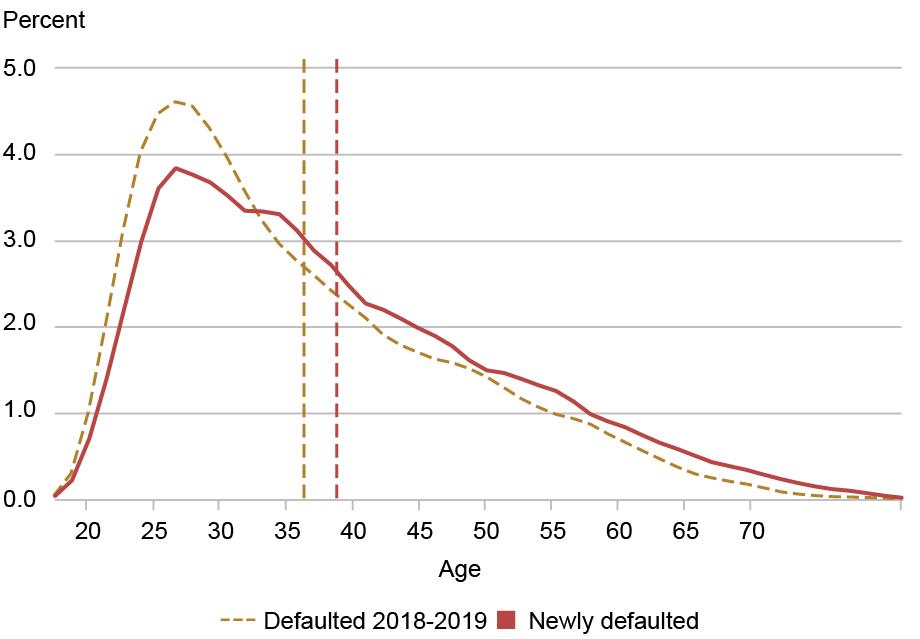

We start our exploration by analyzing the age distribution of newly defaulted pupil mortgage debtors. Within the chart beneath, we plot the age distribution of pupil mortgage debtors who entered default between 2018:Q2 and 2019:This fall (the dashed gold line) towards those that newly defaulted during the last two quarters (the strong purple line). Moreover, we plot the technique of each teams with vertical strains.

Debtors who lately defaulted are 2.5 years older on common than these in default previous to the pandemic (38.9 years in comparison with 36.4 years). After all, this improve in common age may very well be an artifact of the four-year pause on delinquency reporting quite than a real shift within the profile of a borrower in default—somebody who might need in any other case defaulted in 2021 would as a substitute default in 2025, now 4 years older. Nonetheless, evaluating the complete distribution of pre-pause and post-pause defaulters suggests that there’s additionally a shift throughout the age demographic of debtors prone to default. The chart reveals that the curve has not merely shifted 4 years older. As a substitute, there’s uniformly extra mass amongst older debtors, particularly these 50 and older. The flattening within the 25-30 age vary and the elevated mass within the 50+ age vary is additional proof that older pupil mortgage debtors are scuffling with funds at the next fee than earlier than the pause on funds.

The Age Distribution of Defaulted Debtors Has Shifted

Notes: The chart plots the age distribution of debtors who defaulted in 2025:This fall or 2026:Q1 (bolded purple line) and debtors who defaulted between 2018:Q2 and 2019:This fall (dotted gold line). The corresponding vertical strains present the means for every group.

Have been These Debtors Already Battling Funds?

To see whether or not newly defaulted debtors had struggled with funds earlier than the pandemic, we glance again on the 2019 fee standing of these debtors who lately defaulted. The chart beneath reveals that the majority current defaulters weren’t late earlier than the pause. Almost 30 p.c had been present on their loans and making funds, whereas practically half both had not but taken out pupil loans or had no fee due but (attributable to grace intervals, deferment, or $0 funds beneath income-driven reimbursement plans). About 20 p.c had been late however not but in default, and about 4 p.c had been already in default earlier than the pause. So roughly one in 4 lately defaulted debtors had been already late earlier than the pandemic however got a reprieve through the fee pause, then finally fell into default after funds resumed.

Amongst those that did have funds due in 2019, the bulk had been present on their loans at the moment. General, these patterns recommend that the debtors who defaulted over the previous two quarters weren’t concentrated amongst those that had been scuffling with funds earlier than the pandemic—greater than three-quarters had been present or didn’t have a pupil mortgage fee due in 2019.

Many of the Newly Defaulted Have been Not Previous Due on Their Pupil Loans earlier than the Pause

Notes: The chart reveals the 2019 fee standing for debtors who newly entered default throughout 2025:This fall or 2026:Q1.

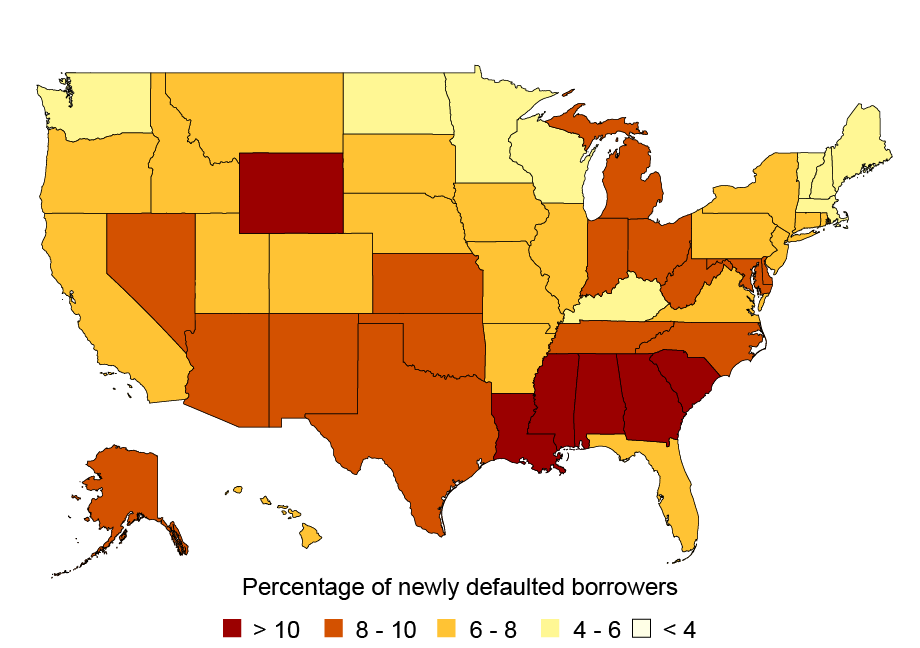

The map beneath reveals the share of pupil mortgage debtors in every state who’ve newly defaulted on their pupil loans. States within the South have the biggest share of newly defaulted debtors, with a minimum of 10 p.c of debtors defaulting in Louisiana, Mississippi, Alabama, Georgia, and South Carolina. Nonetheless, no state was immune from the wave of defaults. Even the states with the bottom focus have a non-trivial share, a minimum of 4 p.c, of pupil mortgage debtors in default.

New Pupil Mortgage Defaults Are Concentrated within the South

Notes: This map presents the share of pupil mortgage debtors in every state who defaulted on their federal pupil loans in 2025:This fall or 2026:Q1.

Implications for Defaulted Debtors and Different Credit score Merchandise

What now for these 3.6 million defaulted debtors? The first consequence of default is garnishment of wages, Social Safety, and tax returns. Nonetheless, assortment efforts for defaulted federal pupil mortgage debtors are at present suspended with no clear timeline for resumption. One other consequence is deteriorated credit score entry. On common, credit score scores for defaulted debtors dropped 91 factors between 2024:Q3 and 2025:This fall (from 567 to 476; credit score scores are Equifax Danger Rating 3.0). Whereas many of those debtors already had subprime credit score scores earlier than missed pupil mortgage funds additional decreased their scores, most can be minimize off from accessing conventional credit score whereas the default stays on their credit score report, which generally lasts for seven years.

However what about their present credit score? The chart beneath reveals delinquency charges for post-pandemic defaulted debtors on different credit score merchandise in 2019:This fall, in 2020:Q3, and in 2026:Q1. These debtors noticed modest declines in delinquency charges through the pandemic, per the development throughout the broader inhabitants. However they now have very excessive delinquency charges throughout all credit score merchandise: practically 40 p.c of these with auto loans are late, 56 p.c of these with a minimum of one bank card are late, and 20 p.c with a mortgage are late. These excessive charges recommend that their fee struggles prolong past pupil loans—and are prone to worsen when assortment efforts resume.

Newly Defaulted Pupil Mortgage Debtors Additionally Are inclined to Be Behind on Different Money owed

Delinquency fee (p.c)

Notes: This chart presents the share of newly defaulted debtors which might be delinquent on auto loans (blue), bank cards (gold), and mortgages (grey) in 2019:This fall, 2020:Q3, and 2026:Q1. Every share is computed conditional on debtors holding that debt sort.

What does this imply for the broader family credit score area? Delinquent and newly defaulted debtors make up solely 2 p.c of the credit score inhabitants and, given their troubled credit score information, typically should not have in depth debt portfolios; spillover from the current wave of defaults and delinquencies to broader credit score markets is prone to be restricted. Balances held by defaulted or delinquent pupil mortgage debtors characterize 2.7 p.c of auto loans, 2 p.c of bank cards, and 1 p.c of mortgages. Additional, Chart 14 within the Quarterly Report on Family Debt & Credit score reveals a decline in new flows into pupil mortgage delinquency, suggesting that the preliminary wave has crested.

Although delinquencies could improve once more when debtors on the sunsetting SAVE plan transition again into reimbursement this yr, we imagine that the biggest wave of pupil mortgage defaults has handed. However the ripples from this wave could proceed to reverberate via the credit score area if the monetary struggles from defaulted loans spill over into relations’ credit score profiles, and when collections on defaulted loans ultimately resume. We are going to proceed to watch pupil mortgage delinquencies and potential spillovers within the coming quarters.

Zara Jacob is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Donghoon Lee is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Daniel Mangrum is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Joelle Scally is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The best way to cite this submit:

Zara Jacob, Donghoon Lee, Daniel Mangrum, Joelle W. Scally, and Wilbert van der Klaauw, “Federal Pupil Mortgage Defaults Return After Pandemic Pause,” Federal Reserve Financial institution of New York Liberty Road Economics, Might 12, 2026, https://doi.org/10.59576/lse.20260512

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).