Jerome Powell’s time period as Federal Reserve chair ended Friday, and assessments of his legacy are already rolling in.

At Bloomberg, Amara Omeokwe and Catarina Saraiva describe Powell as “The Fed Chair Who Fought Again.” At Forbes, Danielle Chemtobe says he “leaves behind a legacy of navigating inflation and defending the independence of the central financial institution below strain from the president of america.” Greg Robb, at MarketWatch, says “Powell’s legacy as Fed chair is preventing inflation and Trump.” Jamie McGeever, at Reuters, describes him because the “Defender-in-Chief.” Squawk on the Road’s Sara Eisen recounts Powell’s legacy as “a champion for Fed independence, saving the world financial system from a deep melancholy through the COVID shutdown, and preventing 41-year excessive inflation with out wrecking the financial system or jobs, reaching the uncommon mushy touchdown.”

If these early accounts maintain up, Powell will likely be remembered as a fighter — and a profitable fighter, at that. He’s broadly believed to have protected the financial system within the pandemic and shielded the Fed from political strain. However his file, on each counts, is considerably combined.

Powell and the Pandemic

When the financial system contracted in early 2020, Powell vowed to do no matter it might take to facilitate a speedy restoration. The Fed, below his management, moved shortly to extend the financial base, reduce the rate of interest it paid on reserves, and open a bunch of emergency lending amenities. The Fed’s efforts, Powell advised the Senate Banking Committee in Could 2020, had been supposed “to facilitate extra straight the stream of credit score to households, companies, and state and native governments” to stop them from failing through the pandemic.

At the least in hindsight, nonetheless, Powell’s Fed seems to have accomplished an excessive amount of.

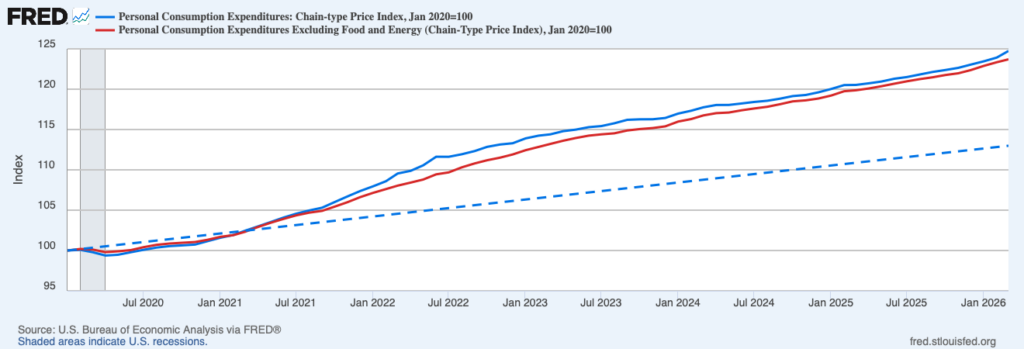

Because the financial system reopened and actual output recovered, the extra liquidity pushed costs increased. The Private Consumption Expenditures Value Index, which is the Fed’s most well-liked measure of inflation, grew 13.9 % from January 2020 to January 2023 — or, roughly 4.3 % per yr. The surplus inflation left costs round 7.8 % increased than they’d have been had the Fed hit its two-percent inflation goal over the interval. The restoration was speedy. However the price was increased inflation.

Little question some will attempt to absolve Powell of the excessive inflation in 2021 and 2022. Many initially attributed the upper costs to pandemic-related provide disruptions and, later, Russia’s invasion of Ukraine. And a few nonetheless imagine constrained provides — not Fed coverage — are largely accountable.

As I defined on the time, nonetheless, non permanent provide disruptions can’t account for the everlasting rise in costs:

Non permanent provide disturbances are non permanent. The pandemic and corresponding restrictions diminished our skill to provide. However they won’t scale back our skill to provide ceaselessly. The lifting of restrictions, vaccine rollout, and gradual acceptance {that a} gentle model of the virus is endemic will finally allow manufacturing to return to regular, even when it has not accomplished so already. […] When manufacturing returns to regular, so too do costs. However that isn’t what the Fed is projecting. As an alternative, the Fed is projecting that costs will stay completely elevated. Why would a brief provide disturbance trigger a everlasting enhance within the stage of costs?

Manufacturing had principally returned to its pre-pandemic development path by 2021:Q3. However costs remained elevated. Certainly, they had been rising extra quickly. The implication, as I mentioned then and would repeat within the months that adopted, was clear: a lot of the inflation — and positively the lasting part — was demand-driven.

Though Powell initially thought inflation was supply-driven, he finally got here to simply accept that there was a demand-side downside, as properly. He famously deserted the time period “transitory” in November 2021. And, as Invoice Bergman and I have proven, the Federal Open Market Committee (FOMC) revised its assertion in December 2021 to acknowledge “Provide and demand imbalances […] continued to contribute to elevated ranges of inflation” (emphasis added). I feel Powell — and others on the FOMC — ought to have acknowledged the demand-side downside by September 2021. However he did finally acknowledge it.

One would possibly give Powell a cross for less than belatedly seeing the demand-side downside and the corresponding must tighten financial coverage. However ought to he get credit score for bringing down inflation as soon as the issue was understood?

Powell appears to assume so. “We regarded on the inflation as transitory,” he advised journalists in January 2025. “And when the information turned in opposition to that in late [20]21, we modified our view, and we raised charges rather a lot. And right here we’re at 4.1 % unemployment and inflation approach down.” The Fed, in Powell’s telling, acted “fairly vigorously […] as soon as we determined that that’s what we must always do.”

In reality, the Powell Fed was relatively gradual to tighten financial coverage even after it realized there was a demand-side downside.

Bryan Cutsinger and I have described the coverage response:

Though the FOMC clearly acknowledged the rise in mixture demand by December 2021, it didn’t instantly increase its coverage price. As an alternative, the FOMC started tapering its asset purchases and indicated it might seemingly start elevating its coverage price in March 2022. In keeping with the December 2021 Abstract of Financial Projections, the median FOMC member thought the midpoint of the federal funds price would rise to 0.9 % in 2022, in step with a 0.75 to 1.0 % goal vary.

[…]

To make issues worse, the FOMC was gradual to revise the tempo of its coverage price hikes as soon as it realized the issue was a lot worse than it had beforehand thought. And it realized the issue was a lot worse fairly shortly.

The FOMC would start elevating its federal funds price goal in March 2022, because it had indicated it might. However the actual federal funds price remained unfavourable by way of June 2022. “The Fed had eased off the accelerator,” we write, “however had not but hit the brakes.”

Why didn’t the FOMC increase charges at its December 2021 or January 2022 conferences? Why did it solely increase charges by 25 foundation factors in March? Why did it go away actual charges unfavourable by way of June 2022? Underneath Powell’s management, the FOMC was not merely late to acknowledge the demand-side downside. It was additionally gradual to tighten financial coverage as soon as the issue was realized.

Certainly, it’s nonetheless making an attempt to get inflation again right down to 2 %. Powell cites a “sequence of shocks,” together with President Trump’s tariffs and the more moderen battle within the Center East, for the shortage of progress. However the issue now, as in late 2021, is extra nominal spending development.

Powell and Political Strain

Whereas some assessments of Powell’s legacy acknowledge his combined file on inflation, the declare that he’s a champion of central financial institution independence normally goes unchallenged. In March 2026, the American Society for Public Administration awarded him the Paul A. Volcker Public Integrity Award for “upholding a regular of devoted service impermeable to political strain.” However right here, too, Powell’s file is combined: he allowed the Fed to float into politically-charged areas and seems to have yielded to political strain from the Biden administration.

Till very lately, Powell seems to have accomplished little to abate the Fed’s mission creep into social justice matters. Louis Rouanet and Alex Salter doc the “rising curiosity by Fed officers in ‘social justice’ matters, versus matters strictly associated to the targets set forth by Congress,” within the years simply previous to the pandemic. Then, in 2020, the Fed revised its Assertion on Longer-Run Targets and Financial Coverage Technique to explain its employment goal as a “broad-based and inclusive purpose,” which appeared to counsel the Fed was contemplating racial employment gaps. “Whereas such gaps clearly exist,” Rouanet and Salter write,

they’re structural: They persist no matter short-run mixture demand fluctuations. This implies the Fed has adopted a purpose that it can’t obtain with out additional embracing direct useful resource allocation, which is de facto fiscal coverage, on the expense of liquidity provision. It additionally pulls the Fed additional into the political area by making central bankers allocators of scarce sources in keeping with political, and maybe partisan, standards. Such actions are, at minimal, in rigidity with democratic governance.

The Fed dropped the phrase from its 2025 revision, regardless of Powell having explicitly affirmed it in prior years.

Powell additionally permitted the Fed to float into local weather coverage. The Fed joined the Community of Central Banks and Supervisors for Greening the Monetary System in 2020 and commenced pressuring banks to reveal local weather dangers and develop regulatory instruments for local weather stress testing thereafter. In 2023, Powell mentioned the Fed has “slim, however necessary, duties concerning climate-related monetary dangers” and that the “public fairly expects supervisors to require that banks perceive, and appropriately handle, their materials dangers, together with the monetary dangers of local weather change.” The Fed withdrew from the Community of Central Banks and Supervisors for Greening the Monetary System in 2025 — simply three days earlier than President Trump’s inauguration.

No matter what one thinks about social justice or local weather coverage, these matters clearly fall past the Fed’s mandate. Permitting the Fed to dabble in these politically-charged areas didn’t bolster its independence. It eroded it. And, though the Fed has since stepped again in each areas below Powell’s management, the injury to its independence has already been accomplished.

Some have additionally claimed political elements are liable for the delayed response to rising inflation in late 2021 and early 2022, as Gregg Robb reviews:

Billionaire macro-trading legend Paul Tudor Jones advised that Powell held off on elevating rates of interest — which had been caught near zero for all of 2021 — as a result of he needed then-President Joe Biden to reappoint him. Biden hoped a robust financial system fueled by decrease charges would assist him get re-elected.

After Biden nominated Powell for a second time period, ‘it was go time’ for price hikes, Jones mentioned in a podcast interview final month.

The timing is actually curious. The Fed clearly acknowledged the demand-side downside in December 2021. However it didn’t increase its federal funds price goal till March 2022, and solely by 25 foundation factors then. When the Fed raised its goal by 50 foundation factors in Could 2022, Powell mentioned “a 75-basis-point enhance just isn’t one thing the Committee is actively contemplating.” Then he was confirmed and the tenor modified. The Fed raised its federal funds price goal by 75 foundation factors at every of the 4 conferences that adopted Powell’s affirmation.

Additional proof that Powell relented to political strain below the Biden administration comes from his go to to the White Home in Could 2022. Whereas it isn’t uncommon for a Fed chair to go to the White Home, the conferences usually happen behind closed doorways. They don’t normally contain a press gaggle within the Oval Workplace. Many considered the occasion as a chance for the president to “deflect blame again to the Fed” or “passing the buck” to the Fed chair forward of the election, and Powell appeared to function a prepared political instrument.

Inflation, Independence, and Powell’s Legacy

There is no such thing as a denying the difficulties the Fed has confronted below Powell’s management, and he deserves credit score for constructing consensus and instilling confidence in unsure instances. He has a remarkably cool demeanor and has managed to maintain his cool regardless of ongoing strain from politicians on each side of the aisle. However one mustn’t let affection for Powell — or, disaffection for President Trump — cloud one’s judgment.

A sober evaluation of the particular selections made and outcomes realized reveals a combined file for Powell. His legacy just isn’t nice, but it surely may have been a lot worse.