The battle within the Center East has precipitated a worldwide provide shock—the third in six years following the pandemic in 2020 and Russia’s invasion of Ukraine in 2022. The present shock raises the specter of spillovers to the U.S. by means of each costs and bodily shortages of products. A crucial conduit for spillovers by means of these channels is through Asian provide chains, particularly from middle- to lower-middle revenue nations in southeast Asia, that are key suppliers for items wanted for the AI infrastructure build-out within the U.S. These nations are additionally closely reliant on Center East power imports. This publish examines key elements associated to those Asian provide chain vulnerabilities.

How Giant Are Provide Strains Thus Far?

The Center East battle has induced the digital closure of the Strait of Hormuz (SOH). Whereas the closure has had main implications for world power markets—previous to the onset of hostilities, shipments by means of the SOH account for roughly one-fifth of world crude oil and 1 / 4 of liquified pure gasoline (LNG) exports—the consequences on world provide chains are a lot broader. That is illustrated within the chart beneath of the New York Fed’s World Provide Chain Strain Index (GSCPI). Over the 2 months because the battle started, the index rose by 1.3 factors, to 1.8 normal deviations above its common worth.

The GSCPI extracts the availability sign from survey information on manufacturing {industry} supply instances, order backlogs, and stock shares in addition to transport prices for ocean and airfreight. The index had been step by step climbing even earlier than the battle started, seemingly partially reflecting strains from the increase in synthetic intelligence funding. Throughout the GSCPI mannequin, the will increase within the index have been pushed predominantly by lengthening supply instances and rising order backlogs.

World Provide Chain Strain Index

The rise within the GSCPI has exceeded the extent of the Fukushima nuclear disaster in 2011 however stays nicely beneath the peaks reached throughout the COVID-19 pandemic. Nonetheless, the abruptness of the rise has been among the many largest skilled exterior of the pandemic and the index itself will not be capturing the nuances of the geographic and industry-specific provide pressures which might be presently being skilled, and are the main target of this publish. Furthermore, analysis means that supply-inflation dynamics will be nonlinear at ranges of the GSCPI beneath pandemic peaks.

As implied by the big improve within the GSCPI, current geopolitical occasions have a lot broader provide implications than the oil market alone. Certainly, the petrochemical {industry} performs a key function in a variety of products and companies. The world’s meals provide, for instance, depends on fertilizers which might be a byproduct of LNG manufacturing within the Center East. The petrochemical {industry} produces fuels for plane, ocean transport, and cooking in addition to plastics, rubber, fibers, and helium—all crucial inputs for each low- and high-tech manufacturing, together with funding in synthetic intelligence.

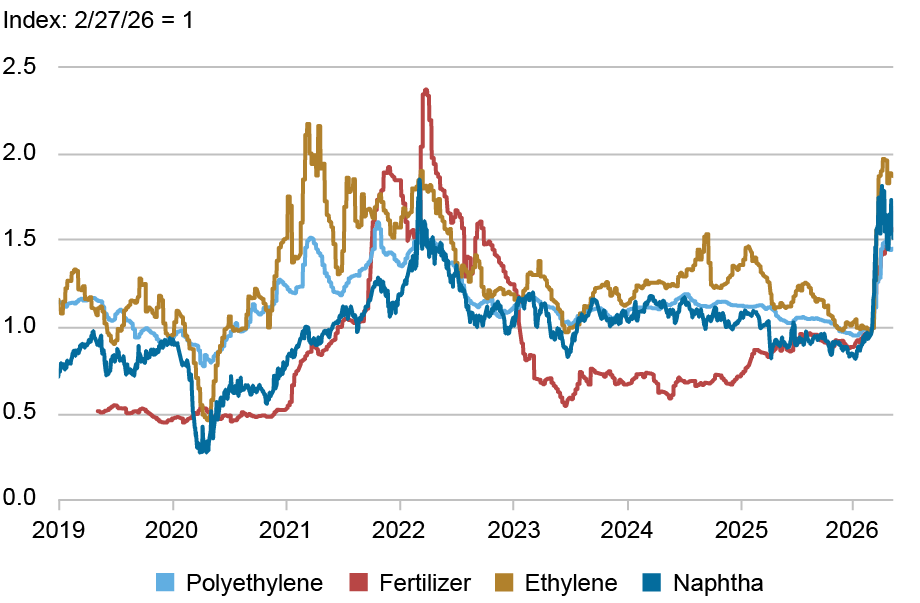

These broader strains are readily obvious in costs for industrial inputs. The primary chart beneath exhibits chosen petrochemical-related costs—fertilizer, feedstocks and merchandise for plastics (ethylene and polyethylene), and naphtha (a hydrocarbon product with a variety of gasoline and industrial makes use of). These costs have all skyrocketed, with current consideration centered on the “plastic shock.” The second chart exhibits that even earlier than the battle, surging demand for AI-related funding was already straining the high-tech provide chain: pc reminiscence costs had skyrocketed, whereas U.S. producer costs for computer-related items had been on a steepening upward development. Semiconductor manufacturing might face further strains if helium falls into quick provide as a couple of third of the world’s provide passes by means of the SOH.

Center East Battle Is Driving Petrochemical Greater

Be aware: Costs proven are averages of spot or near-future indices for Asia, North America, and Europe, the place out there.

Excessive Tech Costs Are Surging on AI Funding Growth

Notes: PPI exhibits PPI for closing demand of digital computer systems and pc gear. PPI information are month-to-month and reminiscence costs are each day.

Asia Provide Chain Vulnerabilities

Though the availability shock up to now has manifested principally in costs, there’s a threat of bodily shortages much like these throughout the pandemic. Manufacturing provide chains in Asia could be a very salient vector for disruptions because the area is very reliant on Center Jap suppliers and performs a central function in high-tech and AI funding.

Because the desk beneath exhibits, Asia is very depending on petroleum merchandise from the Center East, and these provide disruptions threaten the area’s manufacturing provide chains by means of a number of channels. In nations reliant on imported LNG for a significant share of energy technology (for instance, Thailand), electrical energy shortages in a extreme shortfall state of affairs might cut back manufacturing facility working hours. Diminished provide of diesel and jet gasoline are already growing the price of street, rail, water, and air transport—each for inputs heading to factories and closing items headed to ports.

Asia Faces Vital Power Publicity to the Center East

| | Share of Imports From Center East (P.c) | Share of Imports From Center East (P.c) | ||||

| Imported Power Dependence* | Crude Oil | Liquified Pure Fuel | ||||

| ASEAN | ||||||

| Thailand | 58 | 60 | 27 | |||

| Philippines | 54 | 97 | 8 | |||

| Vietnam | 34 | 72 | 26 | ` | ||

| Malaysia | 0 | 72 | 0 | |||

| Indonesia | 0 | 18 | 0 | |||

| Northeast (high-income) Asia | ||||||

| Taiwan | 94 | 69 | 38 | |||

| Japan | 87 | 94 | 10 | |||

| South Korea | 85 | 66 | 19 | |||

| China | 24 | 41 | 30 |

* Internet power imports as a % of complete power use.

The Strait of Hormuz closure has additionally curtailed the provides and raised the value of the petrochemical naphtha, a key feedstock for polymers utilized in a large spectrum of producing items together with plastics, rubber, fibers, and industrial gases. These are crucial inputs for Asian producers from low value-added footwear to auto components to built-in circuits and different excessive value-added electronics.

Petroleum stockpiles fluctuate considerably throughout nations in Asia, which means variations within the timing and severity of a few of the SOH disruption’s results on manufacturing provide chains. In line with U.S. Power Info Administration information, China is estimated to carry the biggest petroleum reserves on the planet of 1.4 billion barrels of crude, sufficient to cowl at the very least 9 months of misplaced internet oil imports from the Persian Gulf. Excessive revenue economies Japan and South Korea are reported by the Worldwide Power Company (IEA) to have roughly six months of complete internet import protection. Based mostly on public feedback from authorities officers, Taiwan seems to carry the equal of about 5 months of crude oil imports (though Taiwan is extra weak to LNG shortages resulting from minimal stockpiles).

Against this, authorities statements and press reviews point out ASEAN nations (Affiliation of Southeast Asian Nations, comprising 11 member states together with Indonesia, Malaysia, the Philippines, Thailand, and Vietnam) maintain comparatively decrease petroleum stockpiles, starting from the equal of round three months of center japanese crude oil imports in Thailand to round a month in Vietnam. The federal government of the Philippines lately reported the nation holds petroleum inventories equal to roughly three months of imports from the Center East.

How Uncovered Is the U.S. to Provide Disruptions in Asia?

The excessive inventories in China and high-income Asian economies present some runway earlier than shortages attain the U.S.—however there may be nonetheless threat that spillovers will materialize extra rapidly by means of the “weakest hyperlinks” in ASEAN. The reason being easy: ASEAN has grow to be tightly built-in into the Asia manufacturing provide chain. Because the starting of 2024, U.S. reported imports from ASEAN have elevated by about 46 %, together with an almost 30 % progress charge final 12 months. Imports from the high-income nations grew by the same quantity, whereas these from China have plunged. Complete U.S. imports from these three teams of nations have grown strongly. Based mostly on evaluation in a earlier publish, ASEAN has grow to be a key provider of products like networking gear (for instance, switching and routing apparatuses) which might be essential inputs for the build-out of AI-related information facilities within the U.S.

The chart beneath exhibits that provide pressures are quickly constructing in Asia exterior of China. This chart exhibits buying supervisor survey indices of provider supply instances for China, high-income northeast Asia (Japan, Korea, and Taiwan) and the three largest exporters to the U.S. from ASEAN (Vietnam, Malaysia, and Thailand), with the 2 areas weighted by U.S. import shares. A rise in these indices signifies a lengthening in supply instances, and the consequences of modifications in demand have been faraway from the supply instances by regressing new orders on the latter. The weighted common of each areas has already exceeded two normal deviations above historic averages and are among the many highest recorded exterior of the pandemic. Solely China has been comparatively unscathed up to now, reflecting its comparatively larger resilience.

Asia ex-China Provide Chains are Strained

Notes: Particular person nation provider supply time indices are adjusted for demand affect, set to imply zero and unit normal deviation, and weighted by rolling three 12 months U.S. import. Excessive revenue NE Asia is Japan, Korea, and Taiwan. ASEAN-3 is Malaysia, Thailand, and Vietnam.

The charts beneath give some perspective on the function that the economies in ASEAN play relative to the a lot bigger economies of northeast Asia. The highest chart exhibits exports to the U.S. of a variety of products—principally intermediate inputs to industrial processes—which might be straight impacted by the SOH closure. ASEAN’s exports of those items are comparable in measurement to these from northeast Asia and considerably bigger than from China. The underside chart offers a way of the significance of the ASEAN area in supplying items wanted for AI and high-tech funding. The rise in ASEAN’s significance for the U.S. has been dramatic and has coincided with a pointy decline in China’s share; ASEAN even exceeded Northeast Asia’s final 12 months.

Asia’s Integral Commerce Linkages to the U.S., Notably for AI Funding

Exports to the U.S. of Items Susceptible to Provide Shock

Be aware: Exports from associate reporter to the U.S. of roughly 60 items on the HS 6 digit stage believed to be notably weak to produce disruptions within the Strait of Hormuz.

Exports to U.S. of Items Essential for AI Funding

Be aware: Exports from associate reporter to the U.S. of roughly 36 items on the HS 4 digit stage that play key roles in AI and information middle funding.

Watchpoints Abound

As a result of U.S. imports of each shopper electronics and AI-infrastructure elements have shifted considerably into ASEAN, power and petrochemical worth shocks from the Strait of Hormuz disruption might cross by means of through increased enter and transport prices and, in extreme instances, bodily shortages. For that reason, ASEAN power vulnerabilities and particular product flows (laptops, reminiscence, networking gear and associated elements) bear shut monitoring for anticipating potential near-term U.S. worth and provide chain dangers.

Hunter L. Clark is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jeffrey B. Dawson is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Shad Turney is a world coverage and technique evaluation principal within the Federal Reserve Financial institution of New York’s Markets Group.

How one can cite this publish:

Hunter L. Clark, Jeffrey B. Dawson, and Shad Turney, “Will Mounting Provide Chain Strains Hamstring the AI Funding Growth?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, Might 11, 2026, https://doi.org/10.59576/lse.20260511

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).