Housing is the most important part of property held by households in america, totaling $48 trillion in 2025. When pure disasters strike, the ensuing harm to houses will be giant relative to households’ liquid financial savings. House owner’s insurance coverage is the first monetary software households use to guard themselves in opposition to property threat. Regardless of the financial significance of home-owner’s insurance coverage, we all know surprisingly little about how insurance coverage contracts are literally designed with respect to property threat. On this publish, which is predicated on our new paper, “Economics of Property Insurance coverage,” we look at how home-owner’s insurance coverage contracts are structured in follow. Utilizing a brand new granular dataset protecting tens of millions of home-owner’s insurance coverage insurance policies, we doc 4 putting patterns about protection limits, deductibles, insurance coverage pricing, and the distribution of property losses.

The Fundamental Construction of House owner’s Insurance coverage Contracts

A home-owner’s insurance coverage contract transfers the monetary penalties of property harm from the family to the insurer in trade for a month-to-month premium. The three essential phrases within the contract are: the premium, the protection restrict, and the deductible. The premium is the worth households pay for insurance coverage. The protection restrict units the utmost quantity the insurer can pay if a loss happens. The deductible is the portion of the loss the family should pay earlier than the insurer begins protecting damages. Collectively, these contract phrases decide how a lot threat is transferred to the insurer and the way a lot stays with the family.

Why do these phrases exist? Financial concept highlights the position of frictions on account of info asymmetries between insurers and policyholders. In a frictionless setting, concept predicts that full insurance coverage could be optimum, that means that losses could be absolutely coated. In follow, nevertheless, frictions exist as a result of insurers can not completely observe how properly owners keep or defend their properties. Deductibles and protection limits assist tackle these frictions. By exposing households to a part of the loss, these contract options can mitigate ethical hazard by encouraging policyholders to keep up their houses and scale back harm threat.

We analyze tens of millions of home-owner’s insurance coverage contracts from 2021 utilizing ICE McDash—contract-level knowledge from residential mortgage servicers—merged with property-level catastrophe threat metrics from CoreLogic. ICE McDash captures every insurance coverage coverage’s premium, deductible, protection restrict, insurer, and related mortgage mortgage. CoreLogic supplies common annual loss and tail threat metrics for every property. By merging these datasets, we observe every policyholder’s insurance coverage coverage particulars and the catastrophe threat their dwelling faces.

Reality 1: Protection Limits Hardly ever Bind

Damages not often strategy the protection restrict. The median protection restrict equals 77 % of the house’s restoration worth (the associated fee to completely rebuild the property). But even in a extreme one-in-one-hundred yr occasion, losses for the median coverage are just one.4 % of restoration worth. This means that realized losses nearly by no means strategy the protection restrict. Because of this, lowering protection limits would have little impact on anticipated insurer payouts.

As a substitute, the economically essential margin of the contract is the deductible. Deductibles decide whether or not any payout happens in any respect and subsequently play a central position in shaping each family threat publicity and incentives for property upkeep.

This sample has implications for the way we interpret insurance coverage costs. Measures equivalent to premium divided by protection restrict are sometimes used as proxies for the worth of insurance coverage. Nevertheless, as a result of protection limits not often bind, such measures will not be informative in regards to the efficient value of insurance coverage. Anticipated payouts rely crucially on the deductible and the distribution of losses relative to it, not merely on the nominal protection restrict.

Reality 2: Deductibles Are Small Relative to Property Worth however Giant Relative to Anticipated Loss

Deductibles are usually supplied in discrete, round-number increments, equivalent to $500, $1,000, $1,500, $2,000, $2,500, or $5,000, with $1,000 being the commonest selection. Due to this fact, in comparison with property worth, deductibles seem small: the median deductible is about 0.3 % of the house’s restoration worth.

Nevertheless, anticipated losses are even smaller. The median annual anticipated loss is barely 0.09 % of property restoration worth, properly under the median deductible. Even after adjusting anticipated losses to account for non-disaster-related parts, we discover that deductibles are giant relative to anticipated losses. As a result of a large portion of losses happens within the vary of losses the place the deductible applies, deductibles play a central position in figuring out family threat retention and in incentivizing house owners to take due care of their properties.

Reality 3: Premiums Considerably Exceed Anticipated Losses

Premiums are a lot bigger than the anticipated claims they pay out. The median ratio of annual anticipated loss to premium is 28 %, indicating that anticipated declare prices account for under a portion of the premium households pay.

This sample is powerful to a number of changes. Excluding the flood part barely reduces the ratio to 26 %, whereas adjusting for theft and legal responsibility shares will increase it to 32 %. Even underneath an aggressive assumption the place CoreLogic captures solely disaster occasions fairly than the total loss distribution, the ratio reaches 43 %—nonetheless implying that premiums considerably exceed anticipated losses. This sample is according to risk-aversion of policyholders. Households are keen to pay greater than the anticipated declare payout in an effort to switch catastrophe threat off their stability sheets, producing a threat premium in insurance coverage costs.

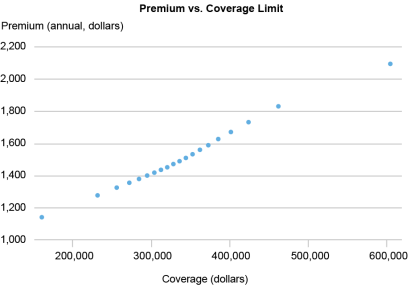

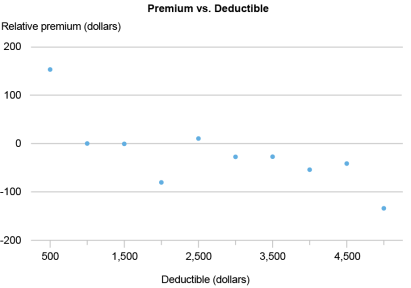

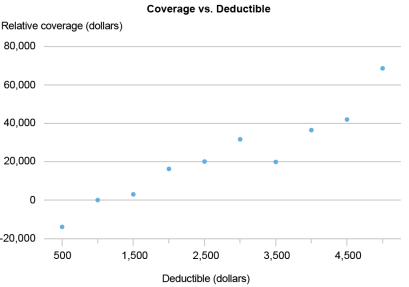

The chart under illustrates how premiums relate to different contract phrases. The highest panel reveals that premiums improve with protection after controlling for anticipated loss, property worth, deductible, and insurer and state mounted results. This displays the truth that larger protection shifts extra potential losses to the insurer. The center panel reveals that premiums lower as deductibles rise, holding protection and threat fixed, according to households retaining extra of the preliminary loss. The underside panel reveals that deductibles have a tendency to extend with protection after controlling for premiums and the identical set of variables.

Relationship Between Premiums, Protection, and Deductibles

Reality 4: Injury Threat Is Low on Common However Skewed to the Proper

Property losses are small on common however will be a lot bigger within the tail of the distribution. The median anticipated annual loss charge is barely 0.09 % of property worth. Nevertheless, losses in uncommon occasions are a lot bigger: the median 98th percentile loss charge is 0.8 %, and the 99th percentile loss charge is 1.4 %. In different phrases, though the anticipated annual loss is lower than 0.1 % of property restoration worth, a one-hundred-year occasion is roughly sixteen instances bigger. This mix of a really small common loss and occasional giant shocks implies that the distribution of property damages is extremely right-skewed, with substantial mass close to zero however a heavy higher tail.

Takeaways

Our evaluation reveals 4 key patterns. Deductibles, not the nominal protection restrict, are the primary financial determinants of home-owner’s insurance coverage contracts. Protection limits not often bind, whereas deductibles regularly do. Premiums considerably exceed anticipated losses, reflecting the worth households place on transferring uncommon however extreme dangers. And the underlying distribution of property losses is extremely skewed, with small common damages however occasional giant shocks.

These findings are sturdy throughout changes. Flood publicity, usually excluded from normal home-owner’s insurance coverage insurance policies, has minimal affect on outcomes when eliminated. We additionally modify for non-disaster claims, equivalent to theft and legal responsibility claims, by evaluating modeled damages with realized claims knowledge. This adjustment modestly will increase estimated losses however doesn’t change the takeaway.

Wanting Forward

A number of questions stay. How are premiums, deductibles, and protection limits collectively decided? How a lot threat is in the end retained by households? Does threat retention fluctuate systematically throughout family sorts and insurers? And the way extreme and pervasive is ethical hazard in home-owner’s insurance coverage? In a future publish, we are going to introduce a structural mannequin of property insurance coverage contracts that hyperlinks family threat preferences, catastrophe threat, and optimum contract design.

Hyeyoon Jung is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jaehoon (Kyle) Jung is an assistant professor on the NYU Stern College of Enterprise.

cite this publish:

Hyeyoon Jung and Jaehoon (Kyle) Jung, “What Hundreds of thousands of House owner’s Insurance coverage Contracts Reveal About Threat Sharing,” Federal Reserve Financial institution of New York Liberty Road Economics, April 13, 2026, https://doi.org/10.59576/lse.20260413

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).