The worldwide company nonfinancial bond market is each a big funding asset class and a significant supply of funding for nonfinancial companies. With $19 trillion excellent on the finish of 2024, a broad portfolio of company bonds could be anticipated to be nicely diversified. But, in 37 p.c of months between 1998 and 2024, greater than 80 p.c of bonds within the ICE World Bond Indices—a portfolio with over 10,000 constituents spanning various industries, credit score scores, and areas—moved in the identical course, suggesting a big diploma of synchronization. On this put up, we introduce the worldwide credit score issue, which proxies for the worldwide worth of danger in worldwide company bond markets. The worldwide credit score issue creates a world credit score cycle in bond danger premia and generates predictable comovement in bond costs.

Measuring the World Credit score Cycle

Is there a world credit score cycle in world company bond returns? To reply that query, we assemble a proxy for a world part of credit score danger pricing, which we dub the worldwide credit score issue. Our strategy, described intimately in our Workers Report, is motivated by the literature on middleman asset pricing, which argues that danger costs mirror stability sheet constraints of economic intermediaries. As a result of the tightness of stability sheet constraints fluctuates over time, so do danger costs.

We implement this concept in our setting by estimating a nonlinear predictive relationship between returns on portfolios of company bonds and observable predictors. We type bonds into portfolios by credit standing—AAA/AA, A, BBB, and excessive yield—in order that the worldwide credit score issue makes use of info each from the general time-series variation in returns and from the differential fluctuation in returns throughout bonds with totally different ranges of credit score danger. Specializing in the predictive relationship between predictors and returns permits us to estimate how danger attitudes translate into anticipated, moderately than realized, returns; that’s, into the value of credit score danger.

The observable predictors proxy for the tightness of stability sheet constraints. Specifically, we use the common default-risk-adjusted unfold for U.S. bonds, additionally referred to as the surplus bond premium (EBP), and the Chicago Board Choices Alternate’s CBOE Volatility Index, or VIX. Whereas Gilchrist and Zakrajsek (2012) argue that the EBP is a quantitative proxy of the chance perspective of economic intermediaries in fastened earnings markets, the value of world credit score danger is more likely to additionally mirror the chance attitudes of a broader set of intermediaries. For that reason, we additionally permit the issue to rely on the VIX, a generally used proxy for the tightness of constraints confronted by a broader set of establishments.

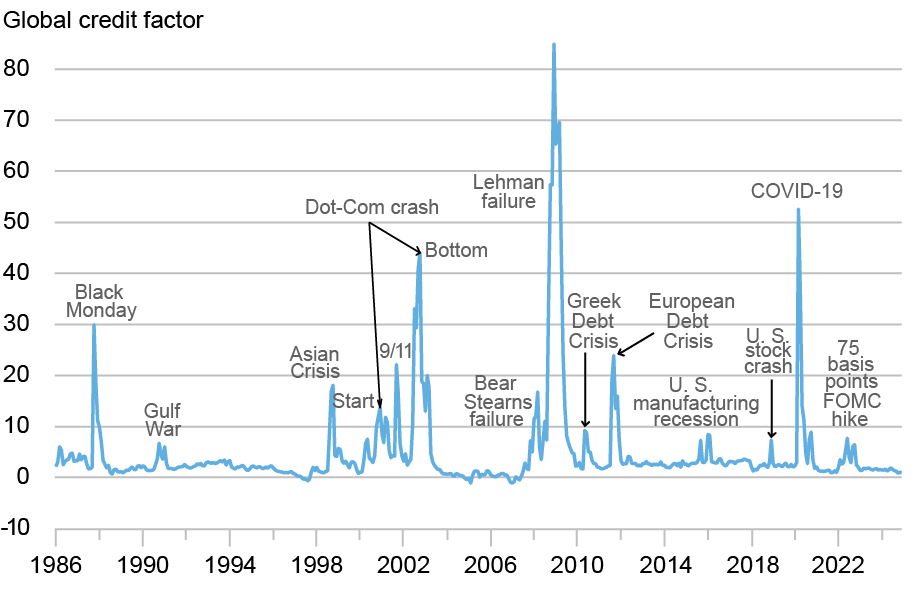

The subsequent chart exhibits the time sequence of the estimated world credit score issue, along with among the largest occasions recognized by peaks within the measure. The worldwide credit score issue tightens when each the EBP and the VIX are excessive, equivalent to in the course of the COVID-19 pandemic (March 2020) and within the aftermath of the Lehman Brothers liquidation (Fall 2008). The issue is as an alternative traditionally low—attitudes in direction of world credit score danger are notably benign—upfront of huge tightenings of the worldwide credit score issue, equivalent to within the run-up to the Asian disaster and the worldwide monetary disaster.

The World Credit score Issue over Time

Word: The chart exhibits the time sequence of the worldwide credit score issue, along with some notable occasions within the time sequence.

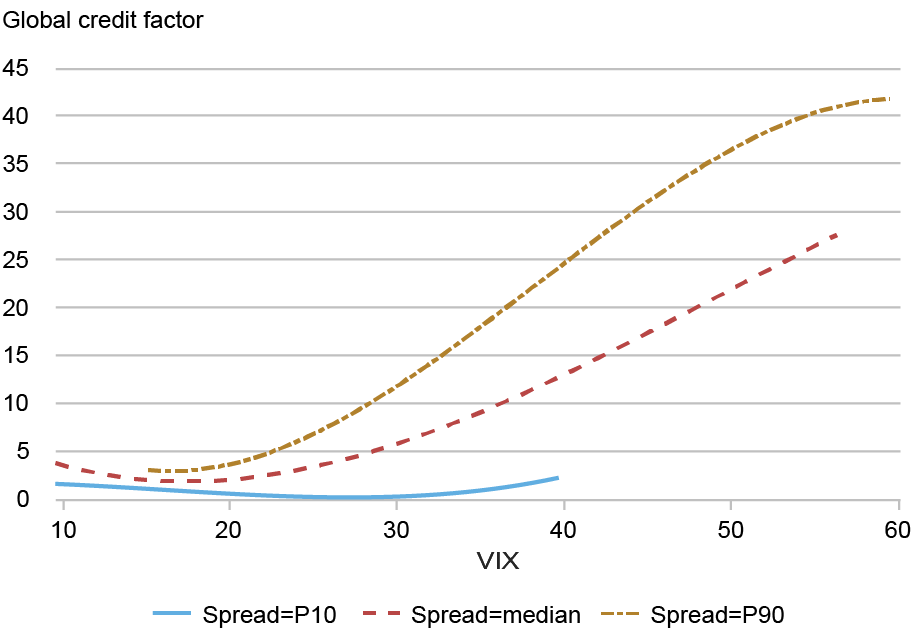

We study the connection between the worldwide credit score issue and the VIX, conditional on the extent of credit score spreads, within the subsequent chart. The chart exhibits that the estimated relationship between the worldwide worth of credit score danger and the VIX is very nonlinear. For ranges of the VIX beneath the historic median of 18, the worldwide credit score issue is to a big extent flat as a perform of the VIX, whatever the stage of credit score spreads. When the VIX is above the median, nonetheless, the slope of the worldwide credit score issue with respect to the VIX will increase as the extent of credit score spreads will increase. In different phrases, the issue is extra delicate to will increase within the VIX at larger ranges of credit score spreads, highlighting the significance of interactions between credit score spreads and volatility in figuring out the worldwide worth of credit score danger.

A Nonlinear Relationship Between the World Credit score Issue and the VIX

Notes: The chart exhibits the connection between the worldwide credit score issue and the VIX, conditional on three ranges of the credit score unfold: the historic tenth percentile (EBP=-0.65), the historic median (EBP=-0.19), and the historic ninetieth percentile (EBP=0.51). EBP is extra bond premium.

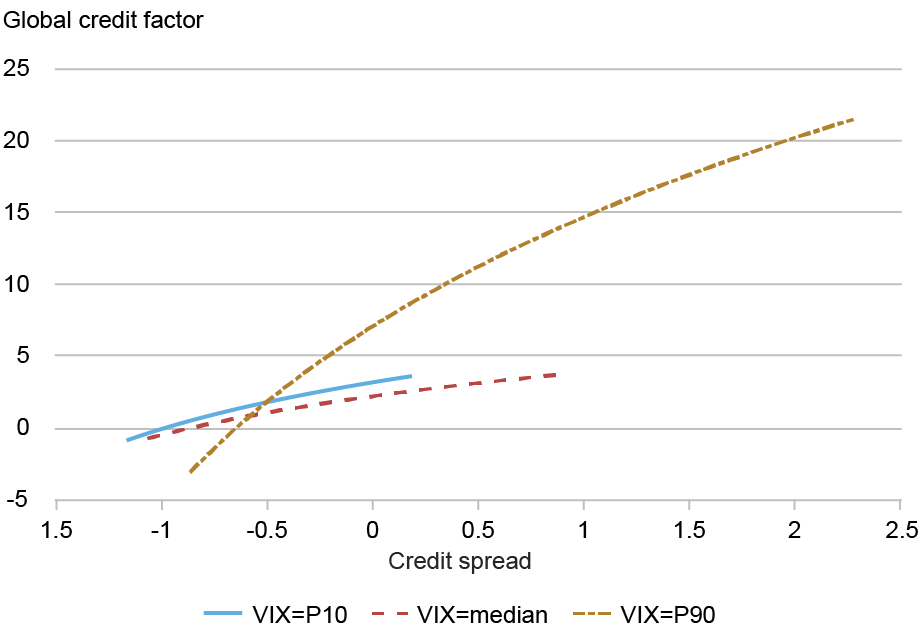

Contemplating the connection between the worldwide credit score issue and the EBP, as an alternative, an identical image emerges. The sensitivity of the worldwide credit score issue to the EBP is comparable for low and intermediate ranges of the VIX. For prime ranges of the VIX, the issue is significantly extra delicate to modifications in credit score spreads.

A Nonlinear Relationship Between the World Credit score Issue and the EBP

Notes: The chart exhibits the connection between the worldwide credit score issue and the surplus bond premium (EBP), conditional on three ranges of the VIX: the historic tenth percentile (VIX=12), the historic median (VIX=18), and the historic ninetieth percentile (VIX=29).

Is the Issue Actually World?

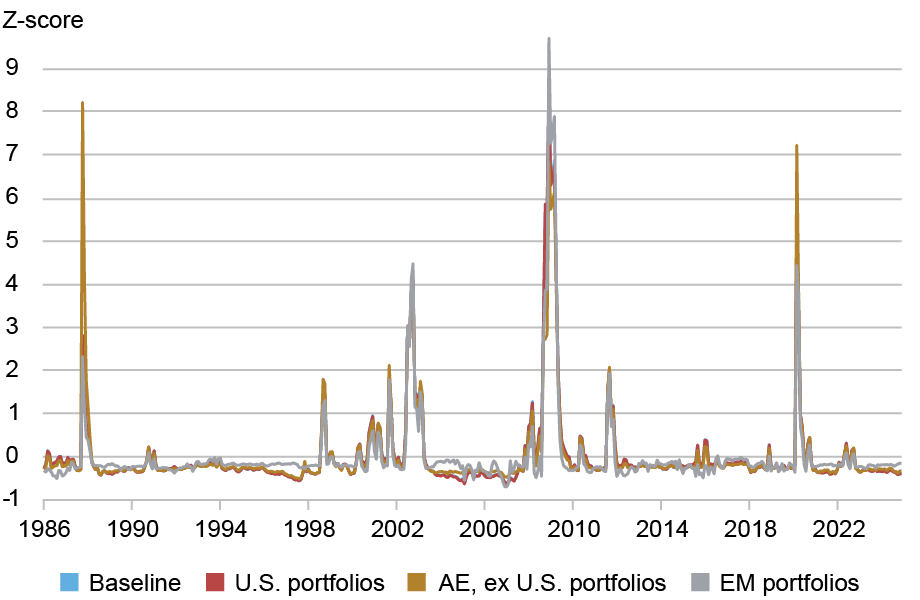

We assemble the worldwide credit score issue to focus on returns on bonds of companies in superior economies, utilizing U.S.-based variables as predictors. Does the credit score issue actually seize world circumstances? To reply that query, we conduct two workouts. Within the first train, we hold the identical predictors—the U.S. EBP and the VIX—and study how the estimate of the worldwide credit score issue modifications as we alter the set of goal returns. The subsequent chart exhibits that the estimated time sequence of world credit score danger are comparable no matter whether or not we use the unique superior financial system portfolios, portfolios of bonds of U.S. companies solely, portfolios of bonds of companies in the remainder of superior economies, or, certainly, portfolios of bonds of companies in rising markets. This discovering is especially outstanding since our information on returns on non-U.S. bonds solely begins in 1998, in order that the connection between the issue and predictors is steady even outdoors of the info used for estimation.

Components Constructed to Goal Different Portfolios Are Much like the Baseline

Notes: The chart exhibits the time sequence of the worldwide credit score issue, along with elements constructed to suit three different units of portfolios: portfolios of U.S. company bonds solely, portfolios of superior financial system (AE) bonds excluding the U.S., and portfolios of rising market (EM) company bonds. All elements are rescaled to have a imply 0 and a regular deviation 1 for comparability.

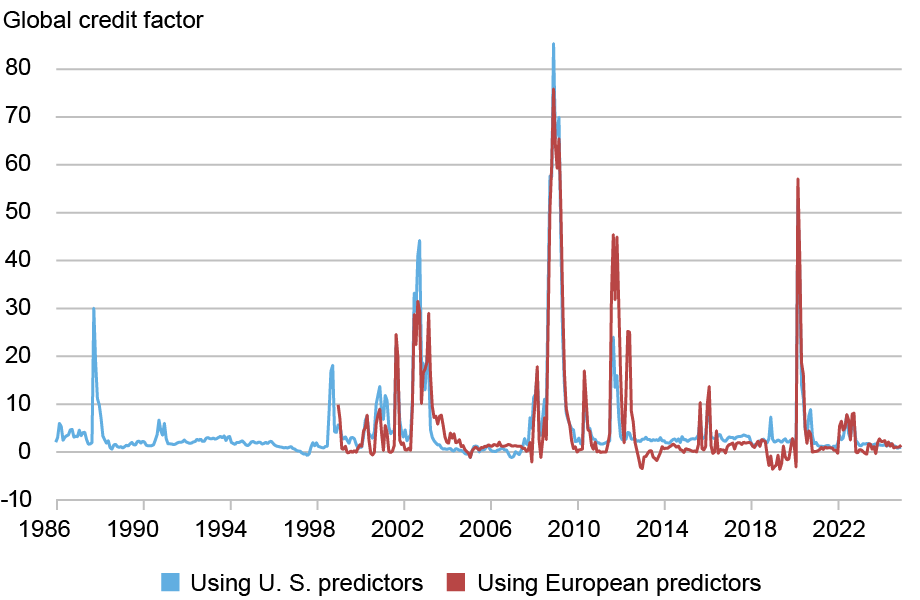

Within the second train, we contemplate how the estimated world credit score issue modifications once we use European predictors as an alternative of U.S.-based predictors. Specifically, within the chart beneath, we use the Euro Stoxx 50 Volatility, or VSTOXX, as an alternative of the VIX and the weighted common default adjusted unfold throughout eight main European international locations as an alternative of the U.S. EBP. The chart beneath exhibits that the issue constructed utilizing European predictors is just like our world credit score issue, albeit every issue displays some native occasions. For the issue constructed utilizing European predictors, the European debt disaster is a considerably bigger occasion than for the baseline world credit score issue. Equally, the baseline credit score issue tightens in the course of the U.S. inventory market crash in December 2018, whereas the credit score issue constructed with European predictors identifies the identical interval as an episode of free credit score circumstances. Thus, whereas the value of credit score danger is certainly world, the locality of predictors used could affect particular person observations.

Components Constructed Utilizing U.S. and European Predictors Are Comparable

Notes: The chart exhibits the time sequence of the worldwide credit score issue, along with the worldwide credit score issue constructed utilizing the Euro Stoxx 50 Volatility (VSTOXX) as an alternative of the VIX, and the weighted common extra bond premium (EBP) throughout eight European international locations as an alternative of the U.S. EBP.

Wrapping Up

World credit score markets are deeply interconnected. On this weblog put up, we have now argued that there’s a frequent part to world company bond returns. In our Workers Report, we present that prime ranges of the issue predict excessive company bond returns and deteriorations in native credit score circumstances, and are related to outflows from world bond funds. Taken collectively, our outcomes are in line with the issue proxying for a typical, time-varying world worth of credit score danger.

Nina Boyarchenko is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Leonardo Elias is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this put up:

Nina Boyarchenko and Leonardo Elias, “The World Credit score Cycle in Company Bond Returns,” Federal Reserve Financial institution of New York Liberty Road Economics, Might 19, 2026, https://doi.org/10.59576/lse.20260519

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).