{kind=link}

The labor share of revenue within the U.S. is presently at its lowest-ever degree within the post-war interval. The labor share measures the fraction of financial output paid to employees as wages and salaries. As such, it’s a helpful benchmark for wage development: when the labor share falls, it implies that productiveness, costs, or each are rising quicker than wages. After much-studied drops within the 2000s, the labor share fell sharply once more after the COVID pandemic. On this put up, we evaluate the dynamics of the labor share post-COVID to earlier intervals to know whether or not the current decline represents the continuation of a pattern or a brand new and distinct phenomenon. We discover that each the cyclicality of the labor share and the contribution of reallocation to the labor share post-COVID are much like earlier intervals.

The Evolution of the Labor Share

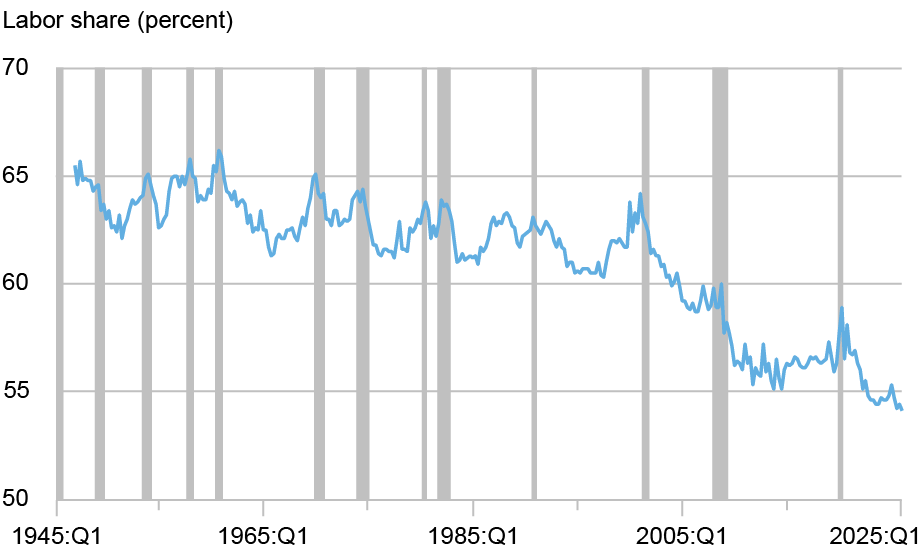

To contextualize the post-COVID decline within the labor share, we first describe its long-run evolution, illustrated within the chart beneath. For a lot of the post-war interval, the labor share was remarkably secure, hovering round 63 % via the late twentieth century. Beginning within the early 2000s, nonetheless, it entered a sustained decline, with a very sharp drop through the world monetary disaster (GFC). The labor share is a core object of curiosity within the tutorial and public debate—it measures the share of mixture revenue going to employees versus capital—and a giant tutorial literature discusses the long-run forces behind this downward pattern, together with technological change, the rise of “celebrity” companies, and growing markups.

The Labor Share Has Declined For the reason that 2000s

Word: Shaded areas point out U.S. recessions.

On this put up, we zoom in on the post-COVID decline within the labor share. After stabilizing within the 2010s, the labor share declined once more through the post-COVID interval, in the end falling 1.6 proportion factors beneath its pre-pandemic degree. The labor share now stands at an all-time low within the post-war interval. Provided that the labor share declined within the two most up-to-date recessions, how does the post-COVID decline evaluate to earlier recessionary episodes?

Is the Put up-COVID Decline Typical Throughout U.S. Recessions?

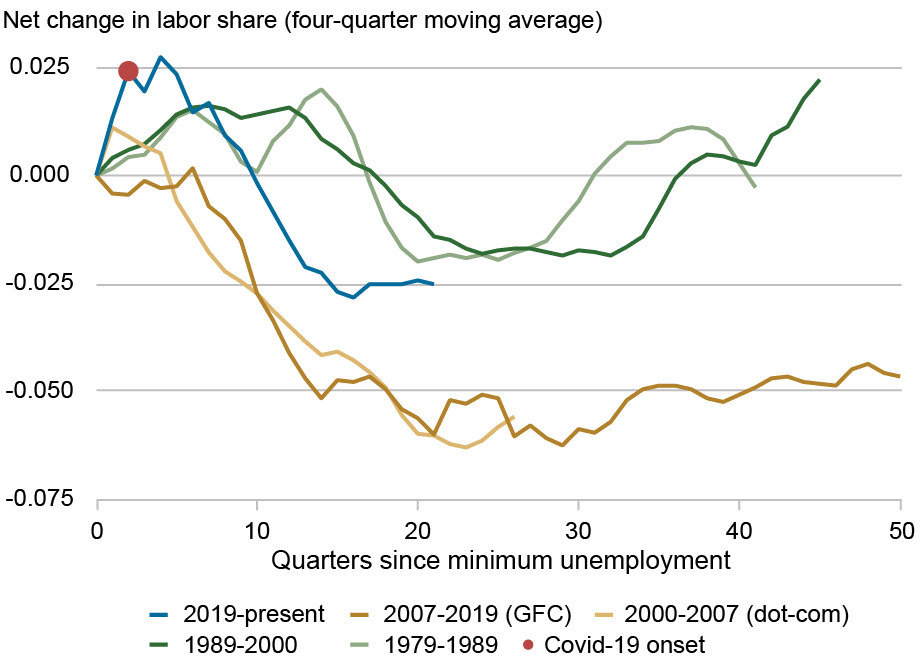

Within the subsequent chart, we examine the trail of the labor share round varied recession–enlargement intervals, tracing its trajectory from the onset of a downturn. We then assess whether or not the post-COVID decline mimics the dynamics of the labor share throughout earlier cycles.

The Put up-COVID Evolution of the Labor Share Aligns with

Pre-2000 Recessions

Most pre-2000 intervals observe the same sample: the labor share will increase throughout a recession, declines via restoration, after which rises once more later within the enlargement. Whereas we limit consideration to the 2 most up-to-date pre-2000 recession–enlargement intervals (1979-1989 and 1989-2000) and omit earlier episodes for readability, we discover broadly comparable dynamics throughout these cycles.

This conduct modifications within the 2000s. Following each the dotcom recession and the GFC, the decline within the labor share throughout enlargement is steeper than in earlier cycles. Furthermore, in contrast to in pre-2000 episodes, the labor share doesn’t meaningfully rebound later within the enlargement.

The dynamics of the labor share on the onset of the COVID pandemic truly seem extra much like pre-2000 recessions: the labor share will increase sharply adopted by a modest decline earlier than flattening out. Judging by previous recessions, we would wish an extended enlargement to see the labor share rise once more.

One other supply of distinction throughout recession–enlargement episodes is the diploma of reallocation in financial exercise. As companies and households adjusted to pandemic restrictions, financial exercise could have shifted considerably throughout sectors. This raises the query of whether or not these shifts contributed to the current decline within the mixture labor share.

Did Sectoral Reallocation Drive the Put up-COVID Decline within the Labor Share?

Some industries have greater labor shares as a result of they rely extra closely on human labor and expertise. As an illustration, healthcare and schooling are inclined to have greater labor shares as a result of output depends totally on employees’ time and experience, whereas manufacturing and agriculture have decrease labor shares as a result of equipment and automation play a bigger position in output. If, within the post-COVID years, a bigger share of output got here from low labor share industries, the mixture labor share might decline even when labor shares inside industries remained fixed.

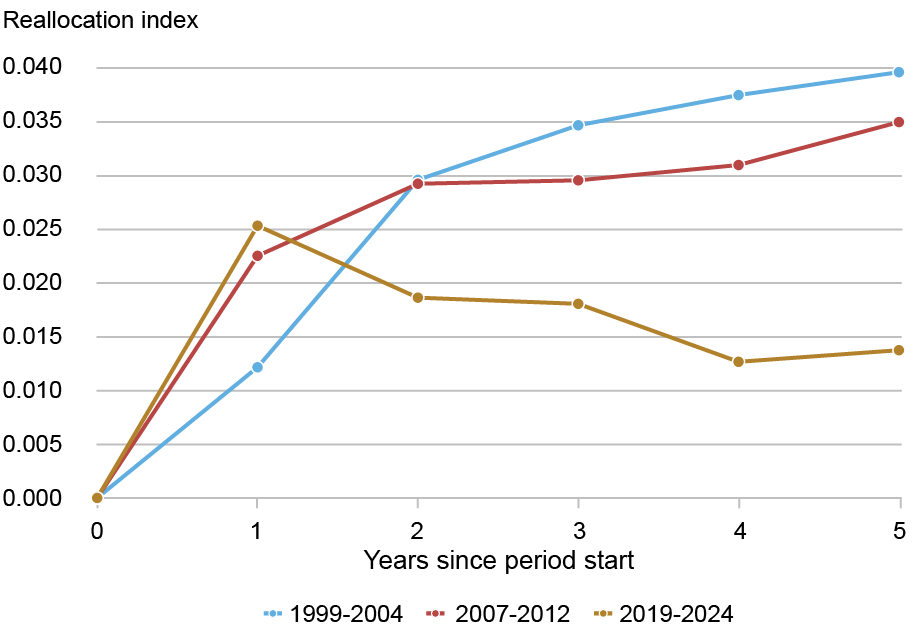

To see if COVID stands out when it comes to reallocation in comparison with earlier recessions, we assemble a reallocation index, outlined as the mixture of absolute modifications in sectoral output shares throughout intervals. The chart beneath plots this index throughout the three most up-to-date recession episodes: 1999-2004, 2007-2012, and 2019-2024. We discover that though sectoral reallocation spiked on the onset of the COVID pandemic, it then moderated and stabilized at a decrease degree. In distinction, earlier recessions exhibited extra persistent and growing reallocation.

COVID Led To a Spike in Financial Reallocation That Shortly Subsided

Notes: The chart exhibits the sectoral reallocation index, which measures how a lot output has shifted throughout fourteen main sectors. For annually, the index measures the full change in sectoral shares of worth added relative to the bottom 12 months for that interval. Larger values point out {that a} bigger fraction of financial exercise has been redistributed throughout sectors, whereas decrease values suggest that modifications in mixture output primarily replicate a comparatively uniform change throughout industries. An index worth of zero implies that sectoral shares are similar to the reference 12 months.

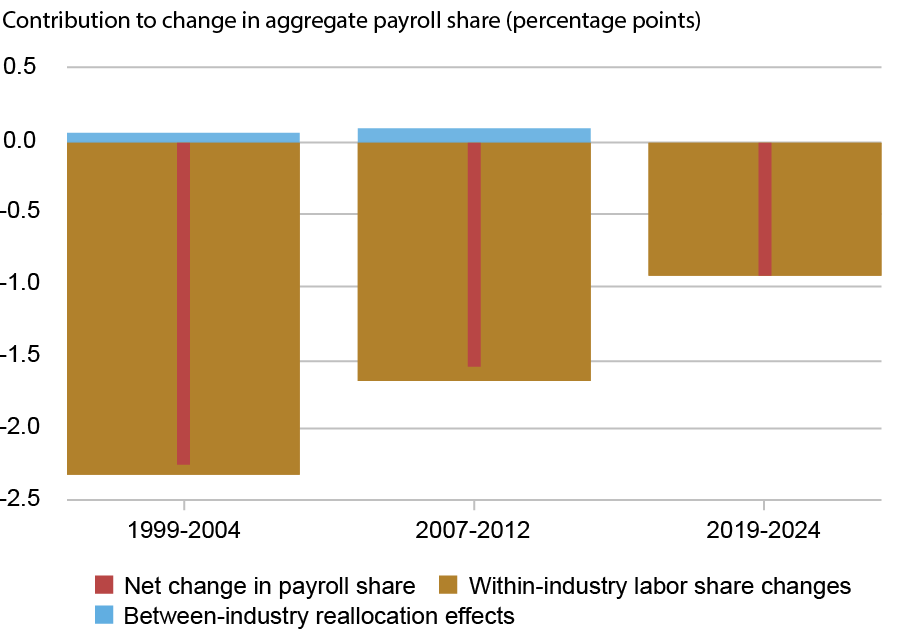

Nonetheless, the general quantity of reallocation doesn’t by itself decide the impact on the mixture labor share. Even modest shifts in financial exercise might cut back the mixture labor share in the event that they transfer output towards industries with decrease labor intensities. To guage this channel, we implement a typical “shift-share” decomposition of the payroll share, which measures labor revenue excluding nonwage compensation. We decompose the change within the mixture payroll share into two components: modifications occurring inside industries (“shift”) and modifications because of financial exercise shifting between industries (“share,” or reallocation). The chart beneath presents this decomposition for a similar recession episodes as earlier than.

The crimson bars present the full change within the mixture payroll share between the primary and final 12 months of every interval. The gold bars seize how a lot of that change within the payroll share was attributable to shifts inside industries—as an example, modifications in how a lot retail pays employees relative to its personal output. The blue bars present how a lot of the change is because of financial exercise shifting between industries—as an example, whether or not output shifted towards sectors that typically have greater or decrease payroll shares.

Inside-Trade Declines, Not Between-Trade Reallocation, Drove the Fall within the Combination Payroll Share

Notes: For every interval, the change within the mixture payroll share is decomposed into (1) a shift element, reflecting modifications in within-sector payroll shares, and (2) a share element, reflecting modifications in sectoral composition. The shift and share element sum to the change within the payroll share throughout the interval.

From this shift–share decomposition, we discover that declines within the mixture payroll share throughout COVID, and the earlier two recessions, have been totally pushed by modifications inside industries slightly than shifts throughout industries. Throughout all three recession intervals, we discover that actions in output throughout sectors contribute nothing or little or no to the change within the mixture payroll share.

Conclusion

This put up paperwork a persistent drop within the labor share following the COVID pandemic. Is that this decline a definite change from the current conduct of the labor share within the U.S.? Alongside the 2 key dimensions we examine, our reply is not any. First, the labor share’s trajectory post-COVID broadly follows the cyclical patterns noticed in earlier recessions, with a decline through the restoration section that mirrors historic dynamics. Second, the decline within the labor share since COVID is pushed primarily by within-industry modifications slightly than shifts in financial exercise throughout sectors. Taken collectively, these outcomes recommend that the post-COVID decline follows the identical cyclical patterns as earlier recessions and is pushed by the identical within-industry forces, and so they present little proof that it’ll evolve in a different way from previous episodes.

Richard Audoly is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Miles Guerin is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Srinidhi Narayanan is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Rachel Schuh is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Find out how to cite this put up:

Richard Audoly, Miles Guerin, Srinidhi Narayanan, and Rachel Schuh, “The Put up‑COVID Decline within the Labor Share,” Federal Reserve Financial institution of New York Liberty Road Economics, June 24, 2026, https://doi.org/10.59576/lse.20260624

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).