{kind=link}

In a 2021 Liberty Avenue Economics submit, we documented the “in a single day drift”—a big, persistent return to holding U.S. fairness futures within the slim window between 2:00 and three:00 a.m. Japanese time, when European fairness markets open. 5 extra years of information later, that sample seems to have pale: the two:00–3:00 window that beforehand generated roughly 3.7 % each year has averaged near zero since 2021. On this submit, we revisit the in a single day drift in gentle of the post-publication pattern and use our inventory-risk framework to ask which of three observable channels—the dispersion of closing order imbalances, the extent of return variance, or the risk-bearing capability of liquidity suppliers—accounts for the change.

The In a single day Drift in One Equation

In our earlier work, we argued that the in a single day drift is compensation earned by liquidity suppliers (LPs)—the individuals who submit resting restrict orders and soak up the residual purchase or promote stress on the finish of the U.S. buying and selling day. When institutional flows tilt closely to at least one aspect within the ultimate hour of buying and selling, LPs step in as patrons of final resort and carry the ensuing stock in a single day. That stock is dangerous: in a single day markets are skinny, costs can transfer towards the LPs earlier than they will offload, and inside danger limits tighten when volatility is excessive. To soak up the imbalance in any respect, LPs demand a reduction on the shut. As abroad patrons arrive just a few hours later—most notably on the Frankfurt and London open—costs rebound, and the LPs earn again their low cost. As a result of in a single day markets are skinny, even modest incoming order movement strikes costs considerably, amplifying the rebound. That rebound is the in a single day drift.

As we derive in our paper, in equilibrium, the anticipated in a single day return is the product of three components:

E[RON] = (greenback order imbalance)t × (return variance)t ×

(risk-bearing capability)−1.

Every issue is observable: closing order imbalances (Channel 1), return variance (Channel 2), and LPs’ risk-bearing capability (Channel 3). The drift fades if any one of many three collapses.

Has the Drift Pale within the Put up-Publication Pattern?

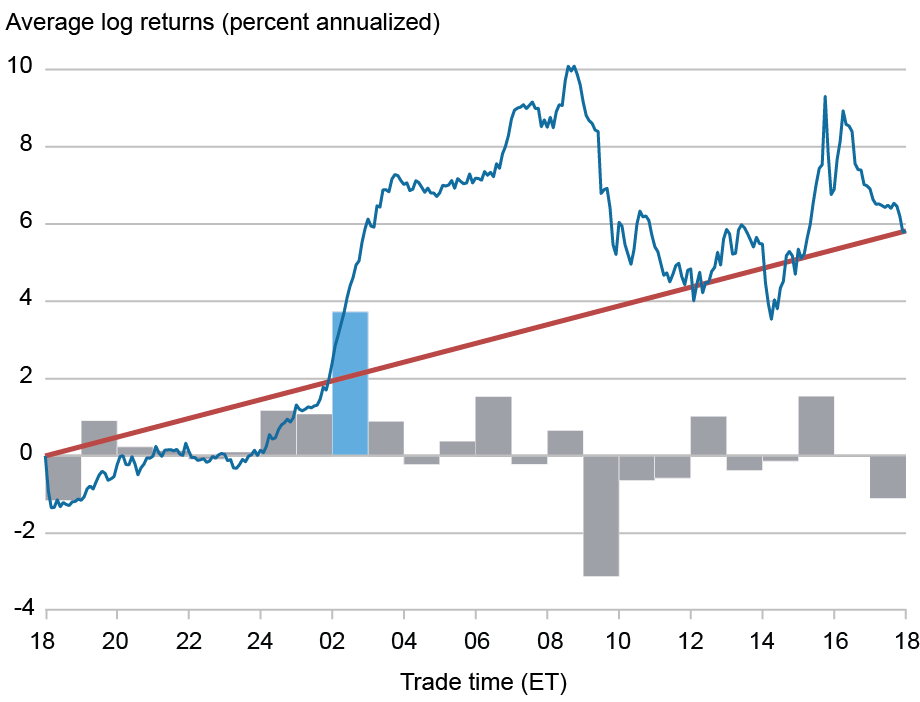

The chart beneath reproduces the signature sample over the 1998–2020 pattern: a pointy acceleration in cumulative returns between 2:00 and three:00 a.m. Japanese time, across the European open.

Returns Have been Massive and Constructive Across the European Open from 1998 to 2020

Notes:Pattern: S&P 500 E-mini futures, 1998–2020 (5,691 buying and selling days). The bars are common annualized hourly log returns throughout all buying and selling days within the pattern; the stable blue line is the common cumulative 5-minute log return over the buying and selling day. The CME buying and selling day begins at 18:00 ET, so the horizontal axis runs from shut to shut (18:00 to 18:00). Instances are U.S. Japanese. The equation calculating the in a single day return is derived in Boyarchenko, Larsen, and Whelan, “The In a single day Drift,” The Evaluation of Monetary Research, Vol. 36, Difficulty 9, September 2023, Pages 3502–47.

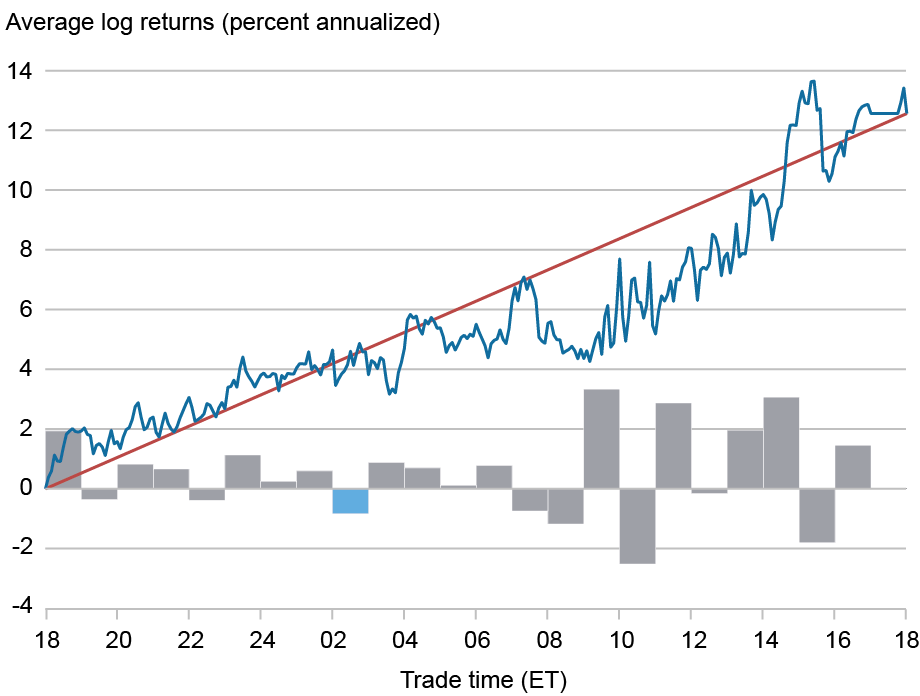

The following chart repeats the train for January 2021 by December 2025. The two:00–3:00 window—beforehand answerable for greater than 60 % of the contract’s 5.9 % annualized close-to-close return—is flat. The identical sample holds within the E-mini Nasdaq-100 (NQ) and E-mini Dow Jones (YM) contracts.

However Returns Have Been Flat on the European Open within the 2021-25 Interval

Notes: Pattern: S&P 500 E-mini futures, January 2021–December 2025 (1,245 buying and selling days). The bars are common annualized hourly log returns throughout all buying and selling days within the pattern; the stable blue line is the common cumulative 5-minute log return over the buying and selling day. The CME buying and selling day begins at 18:00 ET, so the horizontal axis runs from shut to shut (18:00 to 18:00). Instances are U.S. Japanese.

An episode from an asset administration firm is illustrative. In June 2022, NightShares launched two ETFs—NSPY and NIWM—designed to seize in a single day fairness returns by happening lengthy index futures on the U.S. shut and promoting on the U.S. open; the prospectus cited our inventory-risk mechanism. Each funds had been closed fourteen months later, in line with the weakened sample over this pattern (although ETF-specific prices seemingly additionally contributed).

Why Has In a single day Drift Declined?

We now study how the three channels that result in the in a single day drift—the dispersion of closing order imbalances, the extent of return variance, and the risk-bearing capability of liquidity suppliers—have developed since 2020.

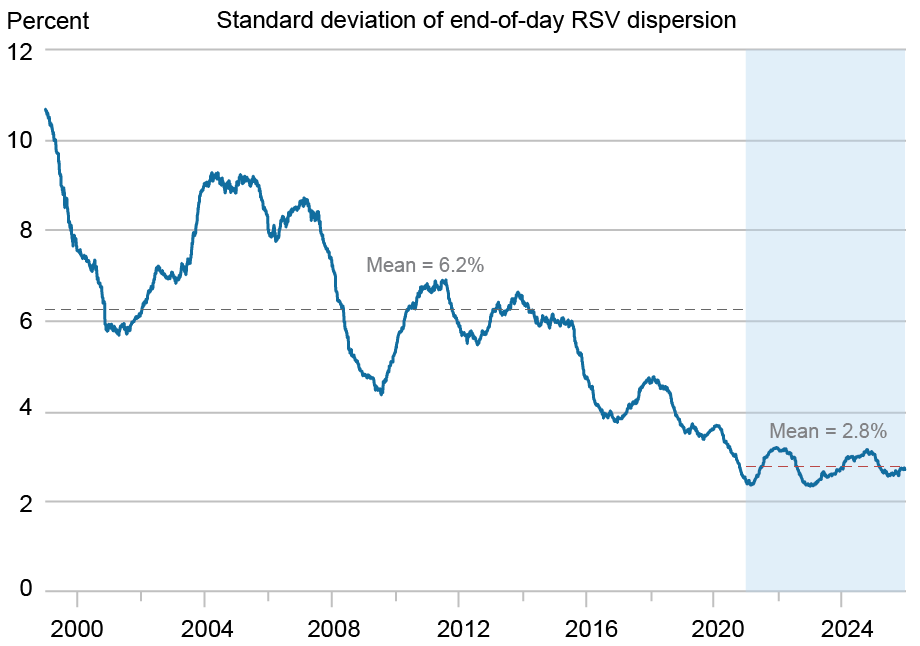

The primary channel is the magnitude of end-of-day order imbalance. Following our paper, we measure relative signed quantity (RSV) throughout the ultimate hour of U.S. buying and selling (15:15–16:15 ET). RSV is the web buyer-initiated share of last-hour quantity, bounded between −1 and +1; it’s giant and adverse on heavy sell-off closes and close to zero on balanced days.

The chart beneath plots the rolling 252-day customary deviation of end-of-day RSV from 1999 by 2025. RSV dispersion trended downward over many of the unique pattern, and the decline has continued by the post-publication interval. Evaluating full-sample averages, the usual deviation of end-of-day RSV fell from 6.5 % to 2.9 %—a compression of greater than half. Excessive closing-imbalance days, which the inventory-risk framework identifies as a supply of in a single day pricing stress, have turn out to be markedly rarer.

Dispersion of Finish-of-Day Order Imbalance Has Halved

Notes: Rolling 252-day customary deviation of end-of-day relative signed quantity (RSV) for the S&P 500 E-mini contract, 1999–2025. RSV is computed over the 15:15–16:15 ET window. Dashed horizontal strains mark interval means. The shaded area signifies the post-publication pattern (2021–25).

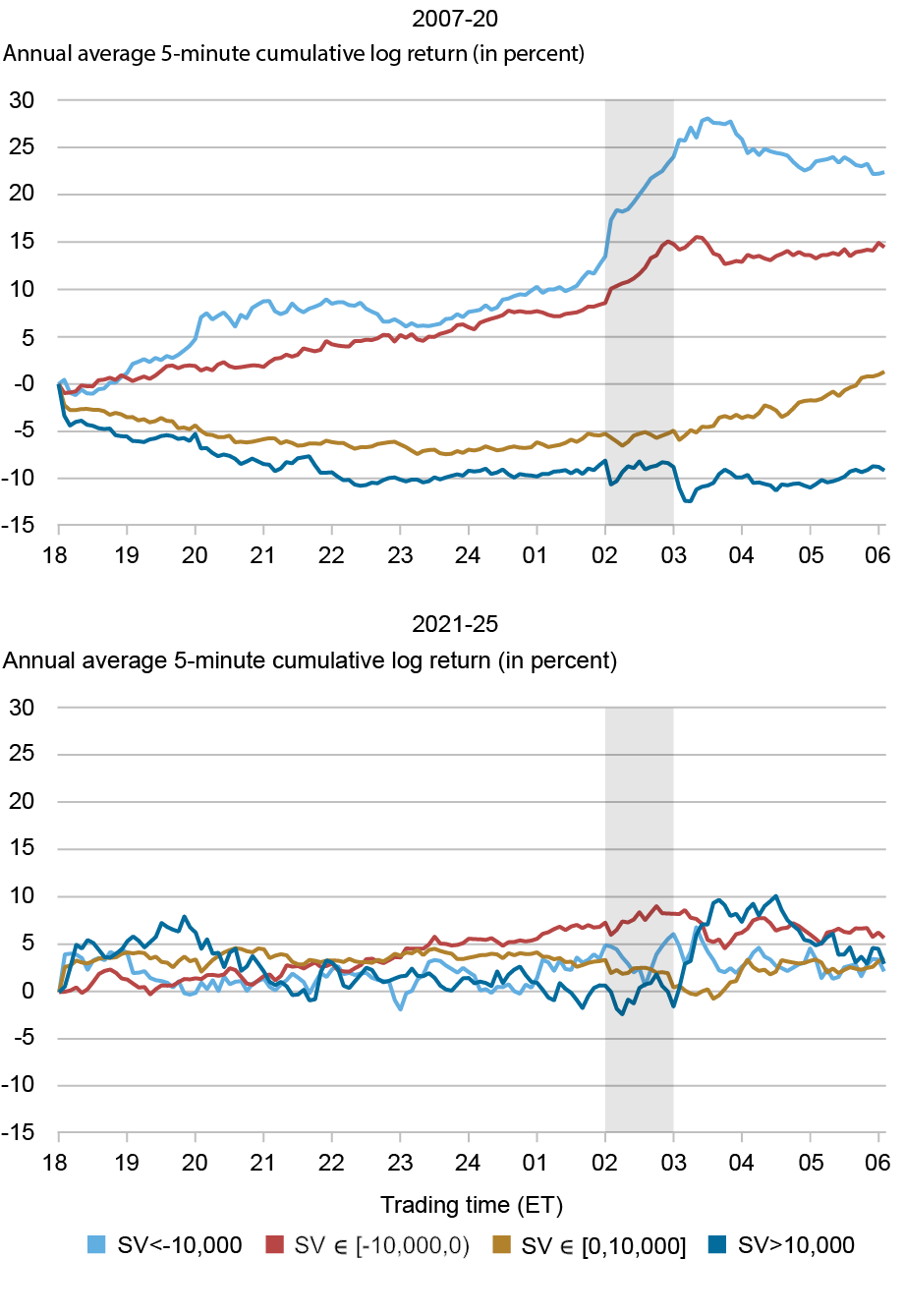

The compression exhibits up within the predictive relationship between closing imbalances and in a single day returns. The following chart kinds days into bins by end-of-day signed quantity and traces cumulative next-day returns. In 2007–20 (high panel), giant adverse closing imbalances are adopted by optimistic in a single day returns whereas giant optimistic imbalances are adopted by flat or adverse returns—a large unfold concentrated within the in a single day window. In 2021–25 (backside panel), the unfold is way narrower, in line with a weaker predictive hyperlink within the post-publication pattern.

The Order-Imbalance–In a single day-Return Relationship Has Damaged Down

Notes: Cumulative next-day log returns are sorted into 4 bins by end-of-day signed quantity. Shaded areas mark the in a single day drift window (2:00–3:00 ET) and the opening reversal (8:30–10:00 ET). Prime: 2007–20. Backside: 2021–25.

Volatility and Liquidity Have Barely Moved

If the compression in closing imbalances accounts for the fade within the drift, our proxies for the opposite two channels shouldn’t themselves have shifted a lot. Certainly, each seem like roughly unchanged throughout samples.

The VIX, a normal proxy for return variance, is little modified: its imply fell solely modestly from 20.4 within the unique pattern to 19.4 within the post-publication interval, with median values of 18.6 and 18.2. In a single day liquidity has remained related within the pre-2020 and post-2020 samples as effectively—the in a single day share of whole E-mini quantity has edged up solely modestly, from 15 % to 16 %. On the measures out there then, the compression in end-of-day imbalance dispersion is the one enter to the pricing equation that has shifted considerably over this era.

What Modified Between the Two Samples?

Our decomposition attributes the majority of the decline to at least one enter to the pricing equation—the compression in end-of-day imbalance dispersion, whereas our measures for volatility and in a single day liquidity are little modified.

In ongoing work, we discover that restrict orders posted on the shut have turn out to be smaller within the post-publication pattern, in line with algorithmic liquidity suppliers slicing movement extra finely and transmitting much less residual stock onto end-of-day counterparties.

Our framework yields a falsifiable prediction: if order-imbalance dispersion widens again towards its pre-2020 vary, the in a single day drift ought to reappear in the identical 2:00–3:00 window, with the identical cross-contract signature. Testing this straight requires a future interval of elevated closing-imbalance dispersion, which the present pattern doesn’t comprise.

Nina Boyarchenko is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Lars C. Larsen is an assistant professor at Copenhagen Enterprise College.

Paul Whelan is an affiliate professor at The Chinese language College of Hong Kong (CUHK) Enterprise College.

How one can cite this submit:

Nina Boyarchenko, Lars C. Larsen, and Paul Whelan, “The Disappearing In a single day Drift,” Federal Reserve Financial institution of New York Liberty Avenue Economics, July 1, 2026, https://doi.org/10.59576/lse.20260701

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).