I learn two articles on the airport early this morning, whereas I used to be ready for a flight, which I want I hadn’t learn. The primary was bemoaning the approaching “$A1 trillion downside” that apparently the Australian authorities and all of us are about to face. It was written by a journalist who’s schooled in paraphrasing press releases from companies and funding banks and holding out the outcomes as someway knowledgeable and unbiased commentary. The second was in regards to the UK and the way it faces a serious challenge with the ‘bond markets’ a la Liz Truss-style and the way it ought to as an alternative do one thing in regards to the Financial institution of England. It was written by a progressive educational (sadly). Neither commentary captures the essence of the problem they search to write down about. However they do current sufficient actuality to supply a pathway into one thing a lot better. Right now, I’ll deal solely with the alleged $A1 trillion downside.

The primary article revealed within the Melbourne Age (Might 25, 2026) – Our $1 trillion debt doesn’t scare markets – nevertheless it nonetheless has a price – stored getting confused as to what the problem they had been attempting to push truly was.

The entree was that nominal gross federal debt is presently standing at $A969.2 billion and can quickly transfer above $A1,000 billion.

The subsequent bond public sale (Might 29, 2026) will challenge $A1,000 million and the subsequent Treasury notice public sale (Might 28, 2026) will challenge $A2,000 million (maturing in two $A1,000 million tranches in late August and early October).

And so what?

The Age journalist truly struggled to say something greater than the “traders who’re lending our authorities the cash aren’t actually fussed in regards to the milestone” and that “Authorities debt has gone up all over the place on the earth and, in contrast with many nations, ours isn’t that top.”

Okay, however then he desires us to be apprehensive as a result of “taxpayers are in the end on the hook for it”.

Are they “on the hook”?

Undoubtedly not.

You would possibly wish to learn these outdated posts:

1. Will we actually pay larger taxes? (April 7, 2009).

2. Taxpayers don’t fund something (April 19, 2010).

3. Who’s in cost? (February 8, 2010).

The superficial look is that taxes are used to pay again debt that the federal government has issued.

However like all superficial appearances they’re sure to be unsuitable.

The purpose is that taxes don’t present the income which the federal government wants with a purpose to pay its payments.

When a authorities bond matures (comes up for redemption), the federal government simply instructs its central financial institution to credit score the checking account of the holder of the bond.

The numbers change in that account (up) and the quantity within the authorities debt account goes down.

There are not any ‘taxes’ in sight.

If the excellent public debt falls over time, because it did on a number of events over the past 50 years (notably between 1996-97 and 2007-08), it’s as a result of the federal government hasn’t issued the identical quantity of recent debt to match the outdated debt that’s maturing.

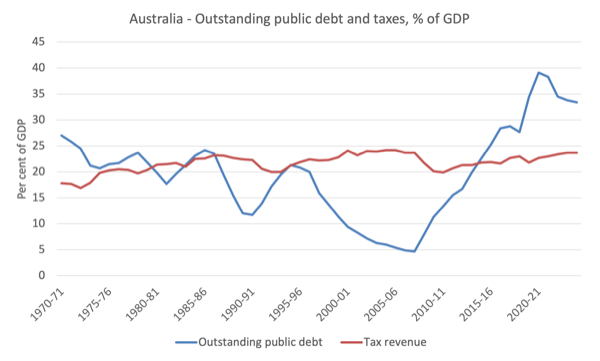

Right here is the time collection for the gross public debt in Australia and the overall federal tax income (each as a % of GDP) since 1970-71.

No relationship evident.

The journalist additionally wrote that it’s the “huge cash managers who fund our authorities debt” and so long as our debt is decrease than the remainder of the world “making us look comparatively prudent”:

… the markets will preserve financing us.

Such poor prose.

Who’s us?

The taxpayers, the nation?

There isn’t a financial sense in any of this.

Authorities debt is threat free for individuals who use it inside their wealth portfolio so long as the federal government that’s issuing the debt additionally points its personal forex.

There isn’t a such factor as “comparatively prudent”.

When the economic system is robust and confidence is excessive, the traders will take extra dangers with the wealth they handle and we then observe the demand for presidency debt decline and yields rise.

The mainstream commentators see that occuring and begin to scream in regards to the traders being about to cease funding the federal government.

However it’s precisely the alternative – issues are going properly.

When threat within the personal monetary markets rise, the cash flows into the danger free bonds and yields fall.

All it tells us is that the urge for food for threat in wealth administration is shifting.

These shifts inform us nothing in regards to the perspective of the personal traders to authorities fiscal coverage decisions.

Furthermore, the inference that these traders are funding the federal government can also be extremely deceptive.

The federal government – for the nth time – just isn’t a family.

I’ve to fund my expenditure – in varied methods – by way of earnings, by way of prior saving out of earnings, by way of gross sales of belongings purchased with prior earnings, and/or from borrowing from banks and so forth.

Why?

As a result of I, such as you, am financially constrained, like all households that makes use of the forex.

However the Australian authorities points the forex and may by no means be intrinsically financially constrained.

Which implies it doesn’t ‘fund’ its spending from debt.

It may need an accounting system that strikes numbers round to present the impression that it’s utilizing the $s from the traders for its spending.

However the intrinsic actuality is that may be nonsensical, on condition that the $A funds that the traders have in surplus have come from earlier authorities deficits, which might logically result in the conclusion that the federal government is funding itself, with a lag.

The article additionally turns into fictional when it says that’s that we ought to be apprehensive in regards to the rising public debt in Australia as a result of it “racks up curiosity” and:

… we shouldn’t ignore the truth that curiosity funds have gotten a rising demand on the federal government, leaving much less capability to spend on different issues.

However there is no such thing as a point out of whether or not the economic system is at full capability or not.

The “much less capability” is implicitly outlined by way of the federal government solely having a lot cash and that finite sum is restricted by the traders.

Which, in fact, doesn’t make sense, once we know the federal government spends by crediting financial institution accounts – including numbers to ledgers.

That’s not a finite course of.

The purpose is that the one significant capability constraint is the provision of productive assets that the federal government can deliver into productive use.

Positive sufficient, if the nation is working at most productive capability then a rise in nominal public spending, whether or not or not it’s from rising nominal curiosity funds on excellent debt or a contract to construct a hospital will most likely generate inflationary pressures.

That may be a totally different challenge from the federal government having “much less capability to spend on different issues”.

And if the nation was at full employment, for instance, and it actually wanted to construct a brand new hospital, then the central financial institution may simply purchase up some excellent debt, drive the yields all the way down to zero, and that may remedy that downside.

Keep in mind the RBA bought about 94 per cent of the general public debt issued within the early days of the pandemic – no questions requested.

And if the curiosity funds had been actually a sport changer, the federal government may instruct the RBA to kind a zero towards the debt it held and that may positively remedy the ‘downside’.

Additional, like all these articles, the journalist has a guidelines of scare subjects that have to be lined.

The final one entertained is that:

… the individuals who find yourself paying extra of that curiosity will likely be future taxpayers – together with youthful generations

And a quote from a child boomer economist who the press likes to quote (ex Treasury official):

My era has seen gorgeous will increase in Australian dwelling requirements and wealth, and but we’re passing on somewhat extra in debt than we should always, and that’s a little bit of an embarrassing fail.

Sure, I’m a part of his era.

Our entry to public infrastructure and providers elevated dramatically once we had been younger and the alternatives {that a} robust public sector gave us by way of training, well being, and so forth made even poor youngsters wealthier.

But I don’t should pay larger taxes than the era that got here earlier than me.

And I don’t count on the youthful generations pays larger taxes both.

Whether or not they get pleasure from higher public providers and so forth is moot given the neoliberal austerity mindsets which have reigned supreme in current a long time – they most likely is not going to have enduring entry.

The purpose is that every era, through the political course of, will get to decide on its personal tax burden, which is unrelated to what went earlier than them by the use of public spending.

I’ve by no means been despatched a invoice to pay taxes to pay again the debt that was incurred by my mum or dad’s era.

Lastly, the final merchandise on the guidelines:

… having extra debt offers governments much less room to reply with fiscal spending throughout an financial disaster

Completely unsuitable.

The federal government has as a lot fiscal spending capability because it needs at any time when it needs no matter what went earlier than.

That capability is restricted when the economic system is sizzling as a result of an excessive amount of nominal spending will trigger inflation.

However throughout a disaster, the ‘fiscal house’ expands dramatically and the federal government can fill any personal spending hole – with out query.

Conclusion

I suppose in spite of everything these years I ought to simply ignore these articles.

However I do know folks learn them as a result of they write to me usually both confused and asking for clarification, or, abusive telling me that I do know nothing and the ‘following article’ proves it.

I dislike Donald Trump considerably, however by coining the time period ‘pretend information’ he was onto one thing, besides his goal was astray.

The ‘pretend information’ is the mainstream macroeconomic commentary that goes beneath the guise of knowledgeable (professional) opinion.

This text is consultant of that swill and systematically misleads the readership.

It’s a main disservice within the quest for an enlightened society.

That’s sufficient for in the present day!

(c) Copyright 2026 William Mitchell. All Rights Reserved.