International holdings of U.S. monetary belongings are immense, with official estimates placing their present market worth at $69 trillion. U.S. holdings of overseas belongings are additionally spectacular however a lot smaller, at $41 trillion. The shortfall in U.S. overseas belongings relative to overseas liabilities has been mounting for many years. But U.S. funding earnings receipts—in earnings, dividends, and curiosity—comfortably exceeded earnings funds till just lately. We present that the fading of the web funding earnings surplus stems from the upward shift in rates of interest within the aftermath of the pandemic together with the continued internet gross sales of U.S. belongings to overseas buyers.

The U.S. Worldwide Steadiness Sheet

The U.S. worldwide funding place could be summarized through a steadiness sheet, with overseas belongings held by U.S. buyers on the asset facet, and U.S. belongings held by overseas buyers on the legal responsibility facet. The desk beneath, drawn from knowledge compiled by the U.S. Bureau of Financial Evaluation, particulars these claims by asset kind. Figures are estimated market values on the finish of final yr.

U.S. International Belongings and Liabilities in 2025

Trillions of U.S. {dollars}, year-end

| Belongings | Liabilities | Internet Belongings | |

| Complete | 41.0 | 68.5 | -27.5 |

| International direct funding | 13.9 | 20.3 | -6.4 |

| Portfolio fairness shares | 15.1 | 22.3 | -7.2 |

| Curiosity-bearing belongings | 10.8 | 25.9 | -15.1 |

| Fastened-income securities * |

4.1 | 15.9 | -11.8 |

| Different lending ** | 6.7 | 10.0 | -3.2 |

| Gold held as reserves | 1.1 | NA | 1.1 |

Notes: All figures are estimated market values. Complete belongings and liabilities exclude the gross notional worth of by-product positions; these have a internet worth of roughly zero.

* Contains securities held as overseas change reserves.

** Largely financial institution loans, financial institution deposits, and commerce credit score.

Complete U.S. holdings of overseas belongings amounted to $41 trillion. International direct funding (U.S. multinationals’ overseas associates and huge minority stakes in overseas firms) accounted for roughly one-third of those holdings. Portfolio fairness holdings accounted for one more third. A lot of the relaxation was held in interest-bearing belongings, together with overseas fixed-income securities, overseas deposits, and cross-border financial institution loans.

International belongings within the U.S. amounted to nearly $69 trillion. Of this sum, $20 trillion went to overseas direct funding (FDI) claims, greater than $22 trillion was invested within the U.S. inventory market, and $26 trillion was held in interest-bearing claims, with Treasuries and different U.S. fastened earnings securities representing the most important a part of this whole.

The online U.S. worldwide funding place is solely the distinction between U.S. overseas belongings and overseas holdings right here: -$28 trillion on the finish of 2025, or 90 % of U.S. GDP. Word that U.S. belongings fell wanting U.S. liabilities in each main class.

The Steadiness Sheet, Monetary Flows, and Valuation Adjustments

The evolution of the U.S. internet funding place is carefully linked to the present account steadiness, the broadest measure of the commerce steadiness. In worldwide commerce, you solely get what you pay for. When U.S. exports fall wanting imports, the steadiness should be lined by promoting off home belongings. If the USA runs a present account deficit and purchases overseas belongings, nonetheless bigger asset gross sales are required to steadiness the books.

U.S. belongings and liabilities are additionally affected by asset value modifications. For instance, greater overseas inventory costs enhance estimated values for U.S. portfolio fairness and FDI holdings. Actions within the greenback additionally play a job, by altering the worth of U.S. overseas foreign money belongings when translated into greenback phrases. There is no such thing as a significant impression on U.S. liabilities, provided that they’re denominated nearly solely in greenback phrases.

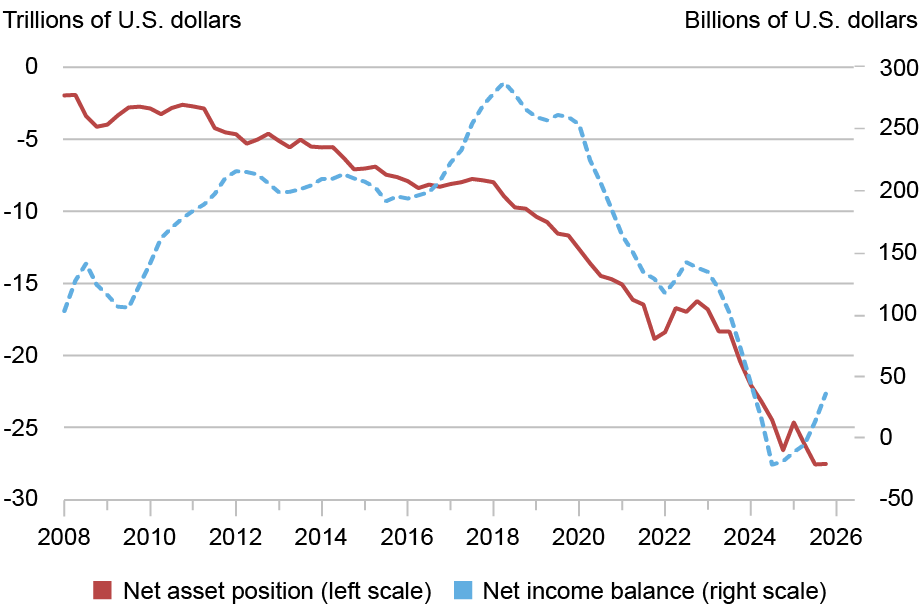

The stable pink line within the chart beneath exhibits the evolution of the U.S. worldwide funding place over the previous twenty years. (We’ll focus on the dotted blue line within the subsequent part.) Word that the web place turned extra damaging by $16 trillion for the reason that finish of 2019, from -$12 trillion to -$28 trillion.

Big Internet Liabilities, however Internet Earnings Nonetheless Barely Optimistic

Notes: Internet asset place is at market worth. Internet earnings is measured as a four-quarter rolling sum.

Monetary flows accounted for -$5.5 trillion of this deterioration, with U.S. purchases of overseas belongings at nearly $6 trillion however overseas purchases of U.S. belongings totaling greater than $11 trillion. Except for the small statistical discrepancy, the -$5.5 billion in internet asset purchases matches the cumulated U.S. present account deficit over the interval, in step with the “You solely get what you pay for” precept described above.

Valuation modifications have subtracted $10 trillion from the U.S. internet place since 2019, including $6 trillion to U.S. belongings however an enormous $16 trillion to U.S. liabilities. A lot of the achieve on each side of the ledger displays the impression of upper inventory costs on estimated portfolio fairness and FDI holdings. (The bigger achieve on the legal responsibility facet owes to a booming U.S. inventory market.) There was little internet impression from change fee modifications.

The Earnings Surplus Puzzle

Whereas U.S. internet liabilities have continued to mount, the U.S. earnings steadiness has appeared to defy gravity. To make certain, the earnings steadiness has fallen lately, from a surplus $260 billion in 2019 to close zero in 2024 and 2025. (See the dotted blue line within the chart above.) Nevertheless it stays far out of line with the huge U.S. legal responsibility place. What explains this disconnect?

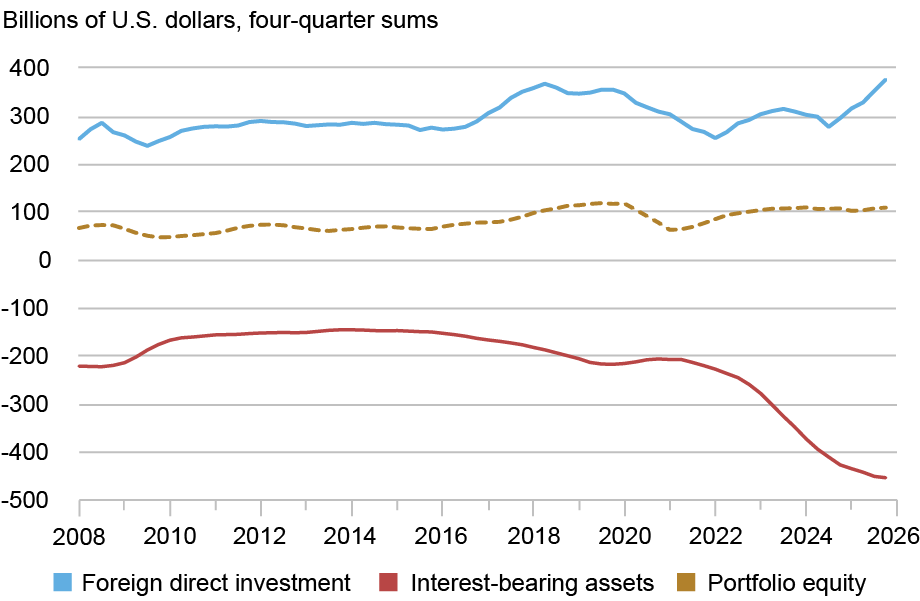

A breakdown of internet earnings flows by asset kind offers essential clues. The chart beneath exhibits flows starting in 2008, damaged down into FDI earnings (earnings), portfolio fairness earnings (dividends), and curiosity earnings.

Rising Curiosity Deficit Weighs on Internet Earnings Steadiness

Word: Figures present four-quarter sums for earnings receipts much less earnings funds.

The U.S. FDI place has generated a constant internet earnings surplus, dipping as little as $250 billion in the course of the top of the pandemic, however rebounding to $360 billion extra just lately. The U.S. portfolio fairness place has additionally generated a constant surplus, at roughly $70 billion to $120 billion since 2019. The mixture of earnings surpluses and place deficits in these asset classes comes with a transparent implication: U.S. belongings earn greater charges of return than comparable liabilities.

The U.S. place in interest-bearing belongings, in distinction, has generated massive earnings deficits since previous to the 2008 monetary disaster. Internet curiosity funds have swelled for the reason that pandemic, with the curiosity steadiness reaching -$450 billion final yr. This enhance in curiosity funds accounts for the shrinking of the U.S. earnings surplus.

The U.S. Fee of Return Benefit

Charges of return on overseas belongings could be measured by the ratio of earnings receipts to market worth. Earnings on FDI belongings contains dividends remitted to the dad or mum firm plus reinvested earnings. Earnings on portfolio fairness consists of dividends. Earnings on interest-bearings belongings contains coupon and different curiosity receipts.

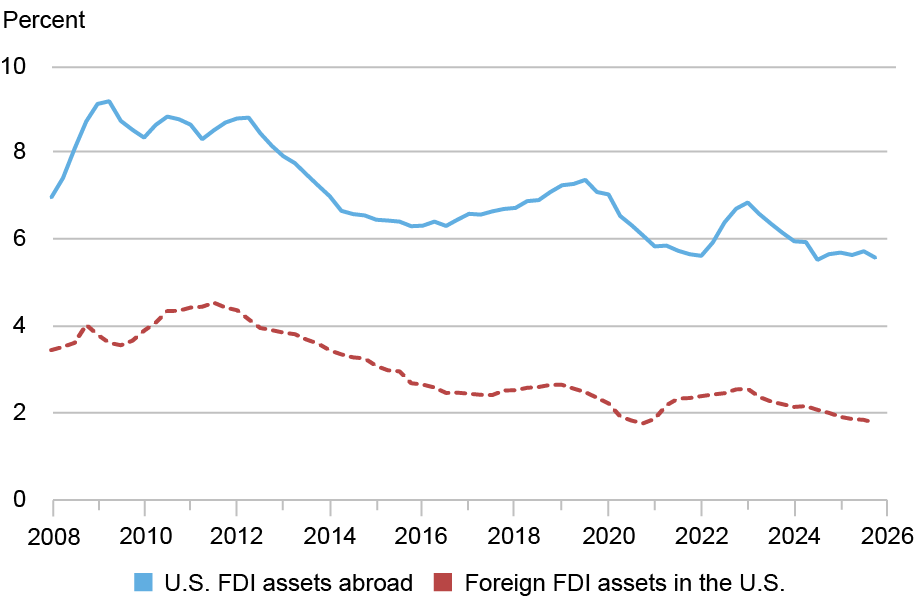

The chart beneath exhibits charges of return for U.S. FDI belongings and liabilities, with far greater returns for U.S. funding overseas. The returns hole explains how a constructive FDI earnings steadiness can exist alongside a damaging internet asset place. (To take the most recent figures, a revenue fee of 5.6 % on $14 trillion in belongings simply exceeds a fee of 1.8 % on $20 trillion in liabilities.) The FDI earnings surplus, in flip, has been the principle issue conserving the general U.S. earnings steadiness in constructive territory.

Persistent Superior Returns for U.S. FDI Belongings

Word: Returns are measured as income-receipts or funds of the previous 4 quarters divided by estimated market values.

The U.S. benefit in FDI profitability has attracted appreciable skepticism, with some observers arguing that it represents a statistical phantasm, maybe from company tax arbitrage methods. This debate has been ongoing for greater than three a long time—see our earlier work—and we don’t suggest to settle it right here.

The U.S. additionally enjoys a longstanding fee of return benefit on portfolio fairness investments. Though this hole is much less stark than for FDI, it stays greater than sufficient to outweigh the big shortfall in U.S. belongings relative to liabilities. The portfolio earnings surplus has been a supporting think about conserving the mixture earnings steadiness in constructive territory.

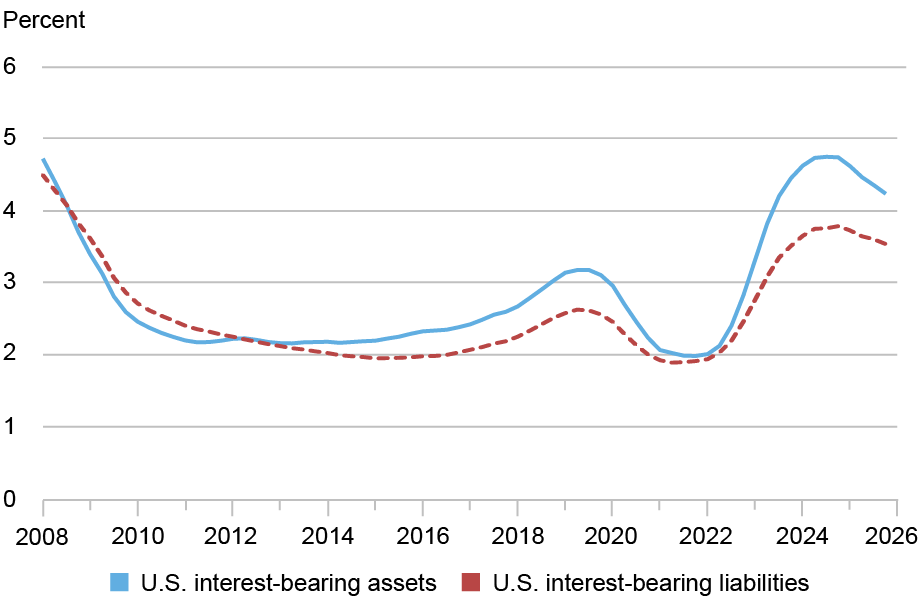

Lastly, the chart beneath exhibits charges of return for interest-bearing belongings and liabilities. Traditionally, these charges have tended to maneuver collectively, partly as a result of each belongings and liabilities are denominated largely in {dollars}. A second motive is that central banks within the U.S. and overseas usually face widespread international shocks.

Comparable Returns on Curiosity-Bearing Belongings and Liabilities

Word: Returns are measured as income-receipts or funds over the previous 4 quarters divided by estimated market values.

Word the sharp rise in U.S. and overseas charges in 2022 and 2023, in the course of the post-pandemic restoration. Given the big U.S. internet legal responsibility place in interest-bearing belongings, greater charges translate into a major drag on internet earnings. In keeping with our calculations, some $170 billion of the $240 billion enhance in internet payouts since 2021 owes to greater rates of interest. The rest owes to ongoing development in U.S. internet liabilities. Notably, solely the partial retracement in market charges since 2024 has prevented the curiosity deficit from rising much more sharply.

Conclusion

Funds on U.S. belongings owned by overseas buyers signify a servicing burden for the U.S. economic system. Earnings, dividends, and curiosity funds that may in any other case accrue to home buyers as a substitute move overseas. Given the necessity to promote U.S. belongings to finance ongoing commerce deficits, this servicing burden appears more likely to mount.

The associated buildup within the U.S. internet legal responsibility place in interest-bearing belongings will even make the earnings steadiness extra delicate to swings in rates of interest. This elevated sensitivity is already in proof. At current, with the asset-liability hole at -$15 trillion, a 1 share level enhance in U.S. and overseas rates of interest would subtract $150 billion from the U.S. internet earnings steadiness. (A 1 share level fall in charges would end in an analogous enchancment.) Solely 5 years in the past, a 1 share level rise in charges would have subtracted $100 billion.

Matthew Higgins is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Thomas Klitgaard is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The way to cite this put up:

Matthew Higgins and Thomas Klitgaard, “Honey, Who Shrunk the U.S. Earnings Surplus?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, Could 18, 2026, https://doi.org/10.59576/lse.20260518

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).