Return to the headlines in 2010 – – “Nations with debt over 90 % of GDP enter a hazard zone”. The 90 per cent threshold entered the media protection on account of a paper launched by Harvard economists Ken Rogoff and Carmen Reinhart – Progress in a Time of Debt. That paper talked about “debt intolerance limits” arising from “sharply rising rates of interest” – after which “painful fiscal changes” and “outright default”. It additionally talked in regards to the “apparent connection” between inflation and excessive public debt ratios – which had me laughing on the time as a result of no-one has actually proven that to be a sturdy relationship in any respect. Everybody began quoting the paper, despite the fact that on the time it had apparent flaws. The predictions did not materialise as did all of the earlier predictions that economists like them had failed. However the press retains giving their views a public platform as a result of the lurid predictions entice audiences. It’s a pity as a result of lame politicians appear to treat the predictions as being based mostly in truth and alter insurance policies for the more serious. Anyway, Rogoff is again on the town predicting that the British authorities will run out of sterling and be compelled to usher in the IMF to deal with the fiscal disaster. That’s what the headlines say. However for those who delve extra deeply, his place is a bit completely different and exposes the chicanery of mainstream economics which holds itself out as a constant physique of principle however often makes use of that pretence to bully governments into political shifts that assist the elites and injury the remainder of us.

Some background character references:

1. Austerity cultist Kenneth Rogoff continues to bore us together with his damaged report (December 2, 2024).

2. Don’t let neo-liberal (idiots) free with a spreadsheet! (August 2, 2016).

3. Elementary misuse of spreadsheet information leaves thousands and thousands unemployed (April 17, 2013).

4. Criticism of failed economists will not be cancel tradition (Could 31, 2021).

5. Apparently the bond vigilantes are saddling up – on their experience to oblivion (February 29, 2024).

6. Discredited educational dinosaurs proceed to hunt relevance (December 12, 2019).

7. It’s basic math (April 10, 2013).

8. Be careful for spam! (January 25, 2010).

When Reinhart and Rogoff’s paper got here out in 2010, I instantly tried to copy the outcomes and failed.

I wrote to Carmen Reinhart as a result of I had met her a couple of years earlier at a operate within the US.

I requested the information.

It seems that I used to be in a queue of researchers asking for the information.

I acquired no reply.

As a long-standing researcher you be taught that if an creator won’t ship you their information then one thing is mistaken.

Maybe they have been too busy.

However extra seemingly, they didn’t need anybody getting their precise dataset as a result of they knew what may be discovered.

It wasn’t clear to me how they generated their outcomes regardless of my laboured makes an attempt to reverse engineer them.

However with out having the precise dataset it turns into meagre surmise and authorized concerns then prevented me from shouting fraud!

However a couple of years after it was revealed, somebody did pay money for the information after which the world discovered what Rogoff and Reinhart had been as much as and it wasn’t fairly.

The examine (April 15, 2013) – Does Excessive Public Debt Persistently Stifle Financial Progress? A Critique of Reinhart and Rogoff – from the Political Financial system Analysis Institute (at College of Massachusetts) – written by Thomas Herndon, Michael Ash and Robert Pollin, offered a devastating critique of Rogoff and Reinhart as a result of it exposes main errors of their fundamental dealing with of the information.

The PERI authors found the rationale for being unable to copy the R&R outcomes lay in “errors” made by the unique authors.

Was it a easy spreadsheet coding error? Or was it a case of educational fraud?

We are going to by no means be ready to tell apart between incompetence or fraud.

On the very least it is vitally sloppy work.

The coverage recommendation that Rogoff and Reinhart tried to promote as evidence-based – that’s, fiscal austerity – was precisely the other to the coverage recommendation that will have been implied if that they had used the information appropriately.

The PERI authors discovered after they used the information appropriately was that nations who’ve public debt to GDP ratios that cross the 90 per cent threshold, skilled common actual GDP progress of two.2 per cent reasonably than -0.1 per cent as was revealed by Rogoff and Reinhart of their authentic paper.

Within the background posts above, I focus on that scandalous incident in additional element.

Leap ahead to 2026

The likes of Rogoff and Co are by no means joyful until they’re within the limelight they usually know they will obtain that stage of consideration by making lurid claims a couple of nation’s solvency.

Within the present state of affairs, it’s the UK that’s the centre of consideration.

The UK Telegraph newspaper ran an article (June 6, 2026) – Labour could need assistance from the IMF, economists warn (behind a paywall – use archicve.is to learn).

The subtitle of the article was sufficiently lurid:

UK hurtling in the direction of disaster by 2030 with nationwide debt set to hit £3tn later this 12 months.

I’ve little doubt that the UK is approaching a disaster however its roots don’t have anything to do with its nationwide debt.

The article then opens with this:

Labour dangers being compelled to hunt emergency assist from the Worldwide Financial Fund (IMF) as Britain lurches towards a debt disaster, main economists have warned.

The journalists then quote Rogoff as asserting that “a serious UK debt disaster earlier than the tip of the last decade was now extra seemingly than not.”

The intention is to undermine the possibilities of Andy Burnham changing into the Labour chief and by dint of that place, the subsequent British Prime Minister.

Why the economists are afraid of Burnham is past me – he ihas lately come out and claimed he would decide to following the ridiculous fiscal guidelines that the Labour Get together has hamstrung itself with.

He stated in Could that (Supply):

Let me say this actually clearly. I assist the fiscal guidelines …

There must be a plan to get debt down, however past that, we have to change politics and take the turbulence out of British politics as a result of that could be a reason behind uncertainty that then has that affect within the markets.

That doesn’t sound like anybody who’s about to finish the company welfare system referred to as the British gilt market.

Anyway, Rogoff is now claiming that the British authorities is heading for a large funding shortfall and can has a 50/50 likelihood that it is going to be compelled to request funding from the IMF to remain solvent.

He was joined by the fiscal conservative Charles Bean (previously LSE, then Financial institution of England), who was quoted as saying:

… that IMF intervention was now a ‘materials threat’.

And the Olivier Blanchard, one other IMF clone economist, claimed that:

I believe it could take at the very least a mini fiscal disaster, with some failed public sale, or spreads rising, to get some governments to do what they should do.

You should be questioning what the hell is happening right here.

It’s merely inconceivable for the British authorities to expire of kilos sterling.

The kilos sterling that the IMF may need in its coffers, a method or one other, got here from the British authorities.

No different physique points kilos sterling.

So what the hell is happening?

Rogoff channelled the Mitterand fiasco in 1983 when François Mitterrand appointed Jacques Delors as his Finance Minister, who had develop into infested with Monetarist ideology (later to be manifest in his push for the euro because the President of the European Fee).

I mentioned that sorry interval in French historical past on this weblog put up – Mitterrand’s flip to austerity was an ideological alternative not an inevitability (August 20, 2015).

The flip to austerity in 1983 was actually the results of a battle between two massive ministry’s within the French authorities (planning versus finance), and the shift in authorities pondering (pushed by Delors) to a ‘Franc fort’ coverage to imitate the Germans – Monetarist 101.

The forex instability that Rogoff mentions arose not due to the French authorities fiscal place (Mitterand’s Socialist push) however as a result of it refused to go away the European Financial System (EMS) and its trade charge preparations at a time when it was inconceivable to take care of a robust franc relative to the German mark (given German insurance policies that promoted a robust mark).

When it grew to become apparent (after the third forex realignment in March 1983) that pursuing an bold fiscal agenda was incompatible with fixing the franc (successfully) towards the mark, France had a alternative.

It may retain its coverage sovereignty and pursue its reliable home targets by floating the franc or stay throughout the EMS and subjugate its home coverage freedom to the dictates of the Bundesbank.

Sadly, for the French and for Europe on the whole, they selected the neo-liberal path, nevertheless culturally alien this was.

This episode doesn’t present assist for Rogoff’s assertion that aggressive fiscal coverage will at all times fail.

Importantly, Rogoff gave the sport away.

After rehearsing the usual theoretical assertions about fiscal deficits, an excessive amount of debt, inflation spiralling uncontrolled and bond markets in revolt, the article then famous that Rogoff admitted that the fact was that “the Authorities would seemingly use the IMF as a scapegoat” and quoted him as saying:

They don’t want the IMF, however they’d name the IMF. McKinsey will usually get referred to as in by an organization that is aware of they should hearth their CEO.

So all the idea bluster was simply the smokescreen.

in my e-book (with Thomas Fazi) – Reclaiming the State: A Progressive Imaginative and prescient of Sovereignty for a Put up-Neoliberal World (Pluto Books, September 2017) – we mentioned the idea of depoliticisation.

This includes the federal government utilizing exterior businesses (and its central financial institution) to deflect criticism of unpopular financial insurance policies that it desires to introduce,

The British Labour authorities used this technique in 1976 when it falsely claimed it needed to borrow from the IMF.

The truth was that Chancellor Denis Healey and PM Callaghan had develop into infested with Monetarist concepts however had an issue – the social compact with the commerce unions.

It wished to inflict austerity however knew it will compromise the compact, which risked setting off renewed wage calls for.

So that they invented the story line that there was a disaster and the IMF needed to bail them out and austerity was required as a part of that deal.

It was an outrageous lie however has develop into a form of totem pole (together with the Mitterand fiasco in 1983) for the likes of Rogoff and Co. to repeatedly refer again to as if there was substance in what Healey and Calllaghan have been up towards.

I analysed the UK-IMF fiasco on this collection of weblog posts:

1. The British Left is usurped and IMF austerity begins 1976 (June 29, 2016).

2. The conspiracy to carry British Labour to heel 1976 (June 15, 2016).

3. The 1976 British austerity shift – a triumph of notion over actuality (June 13, 2016).

4. The British Cupboard divides over the IMF negotiations in 1976 (June 8, 2016).

5. British Left reject fiscal technique – hypothesis mounts, March 1976 (Could 18, 2016).

6. The Bacon-Eltis intervention – Britain 1976 (Could 11, 2016).

7. Britain approaches the 1976 forex disaster April 21, 2016).

8. The British Labour Get together path to Monetarism (April 13, 2016).

Proof reasonably than Ideological Hypothesis

What’s the bid-to-cover ratio?

Reply (courtesy of DMO):

The ratio of the whole quantity of bids to the quantity on provide at a gilt public sale or a Treasury invoice tender.

Additional dialogue will be present in these weblog posts, amongst others:

1. D for debt bomb; D for drivel (July 13, 2009).

2. Bid-to-cover ratios and MMT (March 27, 2019).

The bid-to-cover ratio is simply the the financial quantity of the bids acquired to the whole financial quantity desired by the federal government from the public sale.

So if the federal government wished to position £20 million of debt and there have been bids of £40 million within the major market (the place the debt is first issued to the market sellers) then the bid-to-cover ratio can be 2.

Observe: using the ratio assumes it issues.

The truth is that it doesn’t matter in any respect the place the federal government points its personal forex and is thus not revenue-constrained.

One query I usually get requested is what would occur if the bond market traders in a nation stopped bidding for the debt devices being supplied within the common auctions.

This, in fact, goes to the guts of the error the likes of Rogoff et al. regularly make.

They assert that if the bond market refused to bid at yields that have been politically sustainable then the federal government would lose funding and a fiscal disaster would outcome.

Observe that in major auctions, the federal government selects the ‘market sellers’ (often the large funding banks) who ‘make the market’ by bidding for the debt.

They bid at a yield, which signifies there need for the debt.

However the level is that in most nations (in all probability all – I simply haven’t researched each nation), the first sellers are compelled by legislation to bid and take the debt on the bid they make (ought to that bid achieve success).

Nonetheless, in relation to the query what occurs if the yields rose to ridiculous ranges (very aytpical) then now we have now witnessed a number of occasions in the previous few a long time the place it has been clearly demonstrated that ought to that state of affairs come up, which might make it politically tough for presidency, then the central financial institution simply steps in an makes use of its currency-issuing capability to drive the yields right down to no matter stage they select, together with zero and detrimental values.

For instance, the Financial institution of Japan via its – Yield curve management (YCC) – coverage which began in 2016 held the 10-year JGB yield at detrimental values, that means that the bond traders have been paying the federal government for the privilege of holding the asset over the course of its maturity.

The likes of Rogoff, in fact, had made the ame predictions about Japan as Rogoff and co at the moment are making in relation to the UK.

Their forecasts have been utterly mistaken in that case.

YCC can work in both route however in latest a long time it has concerned the central financial institution shopping for bonds in limitless portions, which drives bond costs up and their corresponding yields down.

Different examples: RBA launched a 3-year yield goal in March 2020 to cope with the uncertainty surrounding the COVID-19 outbreak.

The US Federal Reserve additionally has used YCC previously.

YCC is a bit completely different to quantitative easing (QE), which focuses on bond volumes, though it has the identical consequence.

YCC and QE display that the bond markets can solely have discretion over yields if the federal government permits them to.

At any time that discretion turns into problematic for the federal government it could actually merely override that discretion through its central financial institution.

Each time.

There may be by no means a time that the bond markets can dominate a authorities if the federal government workout routines its alternative.

This pertains to one other vital level.

Foreign money-issuing governments equivalent to that within the UK select the way in which during which their debt devices are issued.

The organisation of debt issuance will not be dictated by the ‘market’ however a matter of presidency prerogative.

A authorities can alter the preparations any time it wishes as a result of the ‘market’ is a creation of the legislative and regulative constructions that solely the federal government manages.

In a contemporary financial system with versatile trade charges it’s clear the federal government doesn’t should finance its spending so the institutional equipment the place debt is issued is only voluntary and displays the prevailing neo-liberal ideology – which emphasises a concern of fiscal excesses reasonably than any intrinsic want for funds (of which the currency-issuing authorities has an infinite capability).

The bid-to-cover ratio refers back to the demand within the major market by the personal sellers for the federal government debt on provide.

I clarify intimately how the first market works within the beforehand cited weblog put up – Bid-to-cover ratios and MMT (March 27, 2019).

Of significance is that it’s extremely interpretative as to what the bid-to-cover ratio indicators.

It actually indicators power of demand however how sturdy turns into an emotional/ideological/political matter.

Even for those who believed that the federal government was financing its internet spending by borrowing, then a bid-to-cover ratio of 1 can be wonderful – sufficient lenders to cowl the difficulty.

Some commentators suppose that 2 is a magic line beneath which catastrophe is imminent. There isn’t a foundation in any respect for that.

There may be additionally no foundation within the assertion {that a} ratio above 3 is profitable and by implication a ratio beneath 3 is unsuccessful.

However keep in mind, as earlier than, for a sovereign governments the bid-to-cover ratio is considerably irrelevant as a result of such a authorities may simply abandon the public sale system at any time when it wished to if the ratio fell to say, 0.00001.

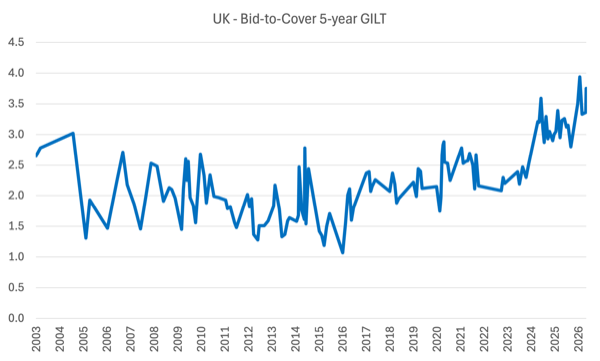

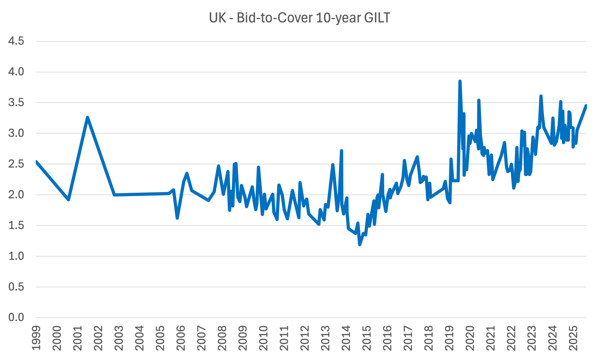

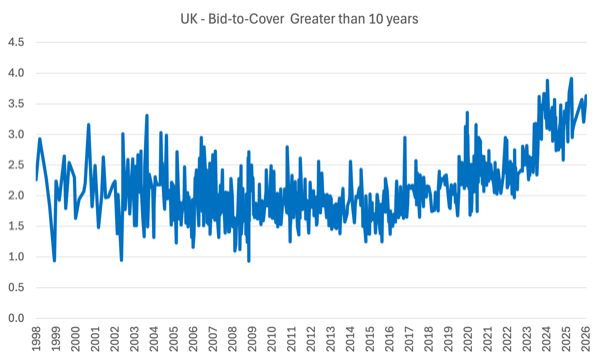

Take into account the next three graphs.

Observe the primary two look a bit odd as a result of the horizontal axis is the date of the gilt public sale in query and the auctions will not be steady in time, which Excel finds tough to deal with.

The three graphs present the bid-to-cover ratio for the UK gilt market managed by the Debt Administration Workplace (a part of the HM Treasury).

They’re so as the 5-, 10-year and all debt above 10-years in maturity.

The ratios are constantly above 3 within the latest years, because the excellent UK authorities debt rose.

The info tells us that the bond traders within the major market are falling over one another to get their palms on the UK authorities debt.

And there’s often greater than 3 occasions as many bids as there’s obtainable debt to purchase.

Observe: The short-term ratios (beneath 5-year maturity) are additionally excessive.

Given the turbulence within the financial world over the past 15 or so years, the information supplies no assist for the assertions from Rogoff and others – who repeat the identical predictions periodically.

Conclusion

The media will proceed to offer a public platform to Rogoff and his ilk as a result of they at all times come out with lurid headlines.

The most recent that the UK will go to the IMF is about as lame as all of the previous predictions which have did not have any veracity.

Maybe Ken ought to focus on his spreadsheet expertise.

That’s sufficient for right this moment!

(c) Copyright 2026 William Mitchell. All Rights Reserved.