Over the course of 2025, the common tariff charge on U.S. imports elevated from 2.6 to 13 %. On this weblog put up, we ask how a lot of the tariffs had been paid by the U.S., utilizing import information by means of November 2025. We discover that practically 90 % of the tariffs’ financial burden fell on U.S. corporations and customers.

2025 Tariffs

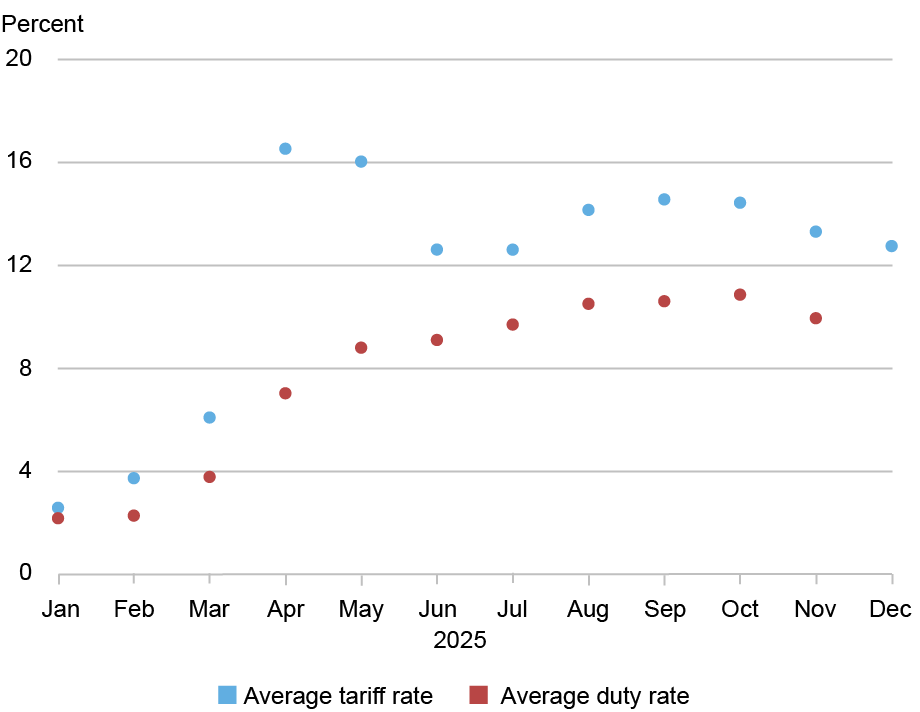

Within the chart under, we plot U.S. import tariffs by month in 2025. The blue dots depict the common statutory tariff charge, weighted by 2024 annual import values. The crimson dots present the common responsibility charge by month, calculated as whole duties collected divided by the worth of whole imports. The typical tariff charge was very low initially of the yr, at 2.6 %. It then spiked in April and Might, when tariffs on Chinese language items had been raised by 125 proportion factors, earlier than being reversed by 115 proportion factors in mid-Might. By the tip of the yr, the common tariff charge was 13 %.

The Common Tariff Price Has Elevated

Notes: The tariff charge is the common statutory tariff charge, weighted by 2024 annual import values. The typical responsibility charge is the whole month-to-month tariff income divided by the whole worth of imports within the month.

The typical responsibility charge is decrease than the common tariff charge due to the various exemptions granted. For instance, though the U.S. levies a 35 % tariff on Canadian imports, 83 % of these imports are exempt from U.S. duties underneath the U.S.-Mexico-Canada Settlement (USMCA). A second cause for the decrease common duties is that importers shift away from high-tariffed items. The distinction between the statutory charge and the responsibility charge peaked in April and Might, when importers shifted away from Chinese language imports in an effort to keep away from the upper tariffs levied on Chinese language items.

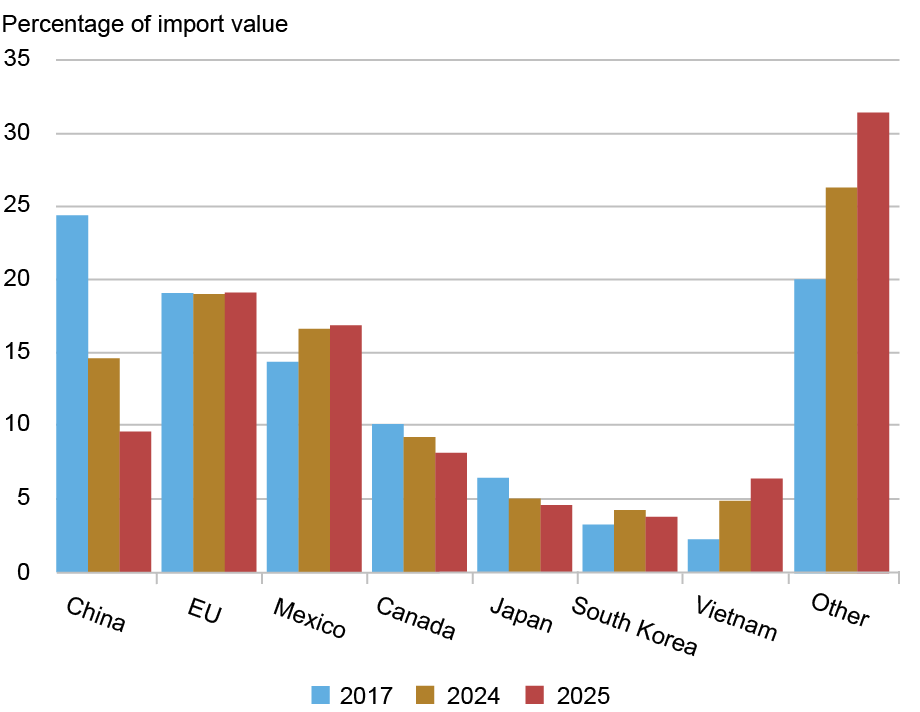

The subsequent chart exhibits how world provide chains shifted in response to the upper tariffs. We plot import shares by nation (or area) for 2017, 2024, and 2025, and nations are ordered by their 2017 import shares. These seven exporters accounted for roughly 80 % of U.S. imports in 2017, with Chinese language items making up practically 25 % of whole imports that yr. Following a 9-percentage-point enhance in tariffs on Chinese language items levied in 2018 and 2019, Chinese language imports fell to round 15 % by 2024. What’s putting is that, within the first eleven months of 2025, China’s share of U.S. imports fell by one other 5 proportion factors, slipping under 10 %. In distinction, Mexico and Vietnam gained probably the most market share. China now faces the very best tariffs among the many nations and areas proven within the chart.

China’s Share of U.S. Imports Has Fallen Markedly

Notes: The peak of every bar represents the worth of non-oil imports from that nation as a share of whole non-oil imports. For 2025 (crimson bars), the info cowl January to November. International locations are ordered by import share in 2017.

Who Bears the Value of Tariffs?

Tariff incidence is the technical time period for a way the prices of a tariff are cut up between international exporters and home importers. Whereas importers pay the responsibility, the “financial burden” of the tariff may be shifted onto exporters in the event that they decrease their export costs. We illustrate this impact by means of a easy instance: Suppose international exporters cost $100 for a superb, and the importing nation decides to levy a 25 % tariff on it. If the international value stays unchanged at $100, the responsibility paid is $25, rising the import value to $125. On this case, the tariff incidence falls fully on the importer; in different phrases, there may be 100% pass-through from tariffs to import costs, and subsequently on U.S. customers and corporations.

In distinction, the exporter may decrease its value in an effort to keep away from dropping market share. If international exporters reply to the tariff by reducing their value to $80 (i.e., $100 divided by 1.25), the value paid by importers will stay $100 (with $20 in duties paid to the federal government). On this case, 100% of the tariff incidence falls on international exporters, who now obtain $20 much less for a similar good; in different phrases, there may be zero pass-through from the tariff for the reason that import value is unchanged.

Contemplating an intermediate case, suppose the exporter lowers its value to $96 to soak up a number of the price in response to the 25 % tariff. The 25 % tariff is then calculated on the brand new, cheaper price, making the tariff-inclusive value the importer pays $120. On this state of affairs, the decrease export value means the exporter pays $4 of the burden, whereas the upper tariff-inclusive value means the importer pays $20. We outline the incidence on the importer because the ratio between the value enhance as a result of tariff ($120 minus $100) and the whole tariff revenues; on this instance, the incidence on the importer is 83 % ($20 divided by $24); the incidence on the exporter (that’s, the value lower they undergo as a ratio of the whole revenues from tariffs) is 17 % ($4 divided by $24).

As a result of tariff incidence hinges on how tariffs have an effect on export and import costs, we now deal with estimating the affect of tariffs on these costs. We comply with the method utilized in our earlier examine, which analyzed the impact of the 2018-2019 tariffs on costs for items exported to the U.S. In that earlier work, we regressed the twelve-month proportion change in international export costs on the twelve-month proportion change in tariffs. We additionally managed for common value adjustments of finely outlined merchandise throughout all nations, and adjustments within the common value of imports into any nation in any month to isolate the differential results of the tariff. Our previous work discovered that international exporters didn’t decrease their costs in any respect, so the complete incidence of the tariffs was borne by the U.S. That’s, there was 100% pass-through from tariffs into import costs.

We now conduct the identical evaluation for the 2025 tariffs, overlaying twelve-month adjustments from January 2024 by means of November 2025 (the newest out there information). We report the leads to the desk under. On this evaluation, we additionally permit the pass-through to alter for various months in 2025. Our outcomes present that the majority of the tariff incidence continues to fall on U.S. corporations and customers. These findings are per two different research that report excessive pass-through of tariffs to U.S. import costs.

Tariff Incidence Falls Totally on U.S. Importers

| Common by 2025 Interval | Tariff Incidence on Overseas Exporters (%) (1) |

Tariff Incidence on U.S. Importers (%) (2) |

| January-August | 6 | 94 |

| September-October | 8 | 92 |

| November | 14 | 86 |

Notes: The outcomes are estimated on a pattern of month-to-month information on the 10-digit Harmonized Tariff Schedule (HTS)-country degree from 2023m1 to 2025m11, with all variables in twelve-month log adjustments. The dependent variable is the log change in import costs (proxied by unit values), unique of tariffs (i.e., international export costs). The unbiased variable is the twelve-month log change in (1 + tariff charge). We work together this variable with a dummy variable equal to 1 for September/October 2025 and one other dummy equal to 1 for November 2025. The regression contains HTS10 product fastened results and country-date fastened results.

We spotlight two foremost outcomes. First, 94 % of the tariff incidence was borne by the U.S. within the first eight months of 2025. This consequence implies that a ten % tariff induced solely a 0.6 proportion level decline in international export costs. Second, the tariff pass-through into import costs has declined within the latter a part of the yr. That’s, a bigger share of the tariff incidence was borne by international exporters by the tip of the yr. In November, a ten % tariff was related to a 1.4 % decline in international export costs, suggesting an 86 % pass-through to U.S. import costs. On condition that the common tariff in December was 13 % (see the primary chart), our outcomes suggest that U.S. import costs for items topic to the common tariff elevated by 11 % (13 instances 0.86) greater than these for items not topic to tariffs. These increased import costs induced corporations to reorganize provide chains, as recommended by the findings introduced within the two charts above.

In sum, U.S. corporations and customers proceed to bear the majority of the financial burden of the excessive tariffs imposed in 2025.

Mary Amiti is head of Labor and Product Markets within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Chris Flanagan is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Sebastian Heise is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

David E. Weinstein is an economics professor at Columbia College.

The right way to cite this put up:

Mary Amiti, Chris Flanagan, Sebastian Heise, and David E. Weinstein, “Who Is Paying for the 2025 U.S. Tariffs?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, February 12, 2026, https://doi.org/10.59576/lse.20260212

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).