A number of nations have carried out a carbon tax or cap-and-trade system to ascertain excessive carbon costs and create a disincentive for using fossil fuels. Primarily, the tax encourages corporations to substitute towards low carbon emission vitality. Prices additionally rise for corporations down the availability chain that use manufacturing inputs with high-emission content material, so the whole affect of a carbon tax could be giant. In observe, nonetheless, corporations even have an incentive to seek out an offset to a carbon tax. On this put up, primarily based on our latest work, we current proof of 1 such adaptation technique. We present that French corporations elevated their imports of high-emission inputs from suppliers exterior the European Union’s cap-and-trade system, generally known as the EU Emissions Buying and selling System (EU ETS), lowering the effectiveness of this strategy to slicing carbon emissions—an adaptation technique that results in “carbon leakage.” To assist cease this leakage, the EU is implementing a “carbon tariff” in 2026, which is the subject of a companion put up.

The EU ETS and Carbon Costs

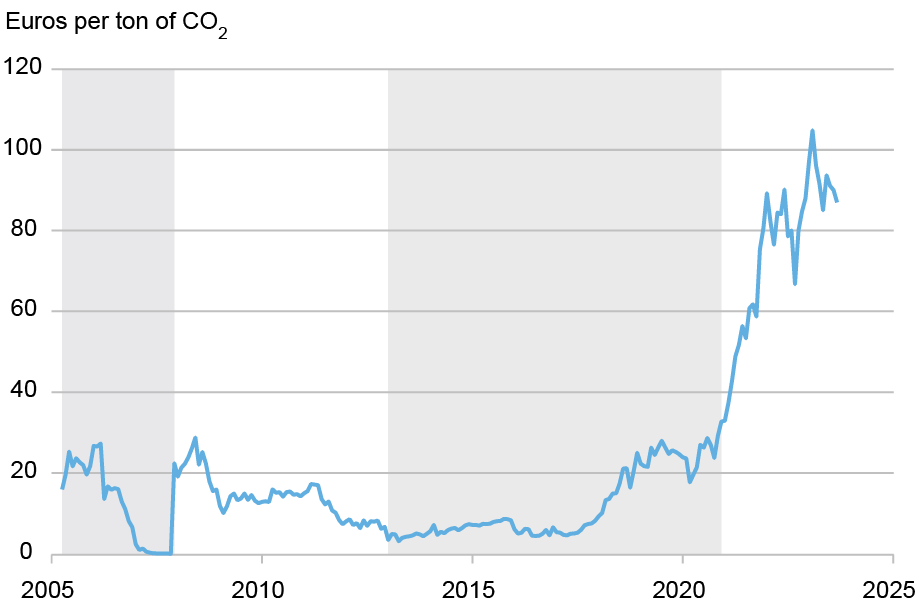

The EU ETS imposes a cap (restrict) of emitted greenhouse gases for a set of corporations in high-emission industries, equivalent to metal manufacturing, chemical compounds, cement, or ceramic items. These corporations can bid on allowances to have bigger emission limits by way of a centralized public sale system. These allowances are then traded on the ETS market, setting a market worth for carbon emissions. The implementation of this method started in 2005 and has developed over three phases to be extra stringent. The chart beneath reveals the evolution of the carbon worth over time due each to modifications in ETS coverage and progress in financial exercise.

Carbon Costs within the EU ETS Have Moved Greater over Time

Notes: The chart is constructed utilizing the end-of-month worth of the closest carbon futures contract sequence sourced from ICE. Every shaded and nonshaded space represents a part of the EU Emissions Buying and selling System (EU ETS).

How We Outline Regulated Items and Sourcing Decisions

We assemble a brand new dataset that classifies “unregulated” and “regulated” manufacturing items by leveraging details about the scope of the European insurance policies. That’s, we outline a listing of regulated inputs primarily based on whether or not these items are coated by the ETS. We merge the listing of regulated items to French corporations’ import knowledge to check the place corporations supply unregulated and controlled items and the way this conduct has modified over time. By specializing in corporations’ imports utilization, we seize the oblique affect of a coverage on downstream buyer corporations.

Outsourcing Excessive-Emission Inputs Alongside the Provide Chain

We draw from this dataset to check whether or not the ETS generated extra regulated imports. Using detailed data permits us to manage for widespread developments and different financial forces that could be driving patterns noticed in French imports, and which might make it tough to establish the affect of the ETS on agency conduct. Particularly, we analyze our dataset throughout three dimensions—importing agency, supply nation, and product sort—to establish how corporations have modified their relative sourcing of regulated imports from non-ETS nations.

We estimate panel regressions and contemplate two margins of adjustment as a dependent variable. The primary measure is the import share of a given enter relative to whole agency imports. The second measure is a dummy variable that signifies whether or not a agency begins to supply a product from a brand new supply nation. A rise in both of those two variables for regulated items relative to unregulated items would point out undercutting of the ETS by corporations. To seize this impact in our regression, we embody an impartial variable that interacts a time dummy with a dummy variable indicating whether or not an enter sourced from a non-ETS nation is regulated or not. We additional embody an array of mounted results to manage for widespread developments and different unobserved variables which will in any other case bias our estimates.

Our regression estimates point out that French corporations elevated their sourcing of regulated inputs from non-ETS nations over time, with that sourcing rising considerably as carbon costs began to rise. This carbon leakage is economically vital: the share of ETS-regulated merchandise sourced from exterior the EU rose by 4.3 share factors between 2004, the 12 months earlier than the ETS was carried out, and 2019. Additional, this improve was partly pushed by a 3.6 share level rise within the likelihood of a agency beginning to import regulated items from non-ETS nations. These estimates verify that French corporations elevated their sourcing of regulated items from exterior the ETS over time and thus decreased the effectiveness of the ETS.

Conclusion

This put up reveals why home carbon coverage is probably not as efficient as supposed in lowering world emissions, since corporations can adapt in an open economic system by altering their sourcing conduct—which merely shifts the place high-emission content material inputs are sourced from and doesn’t lower their world manufacturing.

Different insurance policies, equivalent to carbon tariffs, might help clear up this drawback on the border. In a companion put up, we study the welfare consequence of such a tariff that’s about to be carried out—the EU’s Carbon Border Adjustment Mechanism (CBAM).

Pierre Coster is an economics Ph.D. scholar on the College of Southern California.

Julian di Giovanni is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Isabelle Mejean is a professor of economics at Sciences Po.

Learn how to cite this put up:

Pierre Coster, Julian di Giovanni, and Isabelle Mejean, “What Can Undermine a Carbon Tax?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, January 7, 2026, https://doi.org/10.59576/lse.20260107a

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).