Synthetic intelligence has change into the most recent excuse for reviving one of many oldest dangerous concepts in financial coverage: a common primary earnings. Latest items in Newsweek, the LSE Enterprise Evaluate, and Fortune have all helped push the concept that AI might quickly wipe out so many roles that Washington might want to ship everybody a verify.

That makes for a catchy headline. It additionally makes for awful economics.

The suitable query just isn’t whether or not AI will disrupt work. In fact it’ll. The suitable query is that this: after greater than 100 native guaranteed-income experiments, what have we really discovered?

The reply is far much less flattering to UBI than its promoters would love.

What 122 UBI-Type Pilots Present

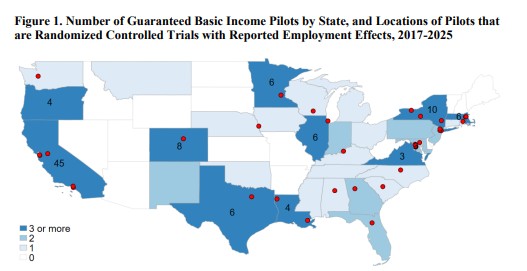

A brand new AEI working paper by Kevin Corinth and Hannah Mayhew offers the perfect current overview of the proof. Per their research, there have been 122 assured primary earnings pilots throughout 33 states and the District of Columbia between 2017 and 2025. These pilots allotted about $481.4 million in transfers to 40,921 recipients, with 61,664 complete individuals together with management teams. The common recipient received about $11,765, the typical pilot lasted 18.4 months, and the typical month-to-month fee was $616.

That appears like a mountain of proof. It’s not.

Of these 122 pilots, solely 52 had printed outcomes. Solely 35 used randomized designs. Solely 30 reported employment outcomes. So the case for UBI just isn’t being constructed on some big pile of clear, clear proof. It’s being constructed on a a lot smaller stack of research, a lot of them weak, restricted, or badly timed.

And right here is the kicker. Among the many 30 randomized pilots with printed employment outcomes, the typical impact was a 0.8 percentage-point enhance in employment. UBI followers will rush to wave that round. They need to decelerate.

AEI reveals that the larger and extra credible research inform a really completely different story. Among the many 4 pilots with remedy teams of at the least 500 individuals, which collectively account for 55 p.c of all treatment-group individuals, the imply impact on employment was minus 3.2 share factors. AEI additionally estimates a imply earnings elasticity of -0.18, which is according to normal labor-supply economics.

In plain English, when folks obtain extra unearned earnings, work tends to fall on the margin. Stunning, I do know. Economics nonetheless works.

Why the Proof Is Weaker Than the Hype

The AEI paper is beneficial not only for what it finds, however for a way bluntly it describes the weaknesses within the proof.

The common remedy group amongst these 30 research was simply 359 folks, and the median was solely 151. That isn’t precisely ironclad proof for redesigning the American welfare state. Among the many 26 pilots for which attrition might be measured, the typical attrition fee was 37 p.c. That may be a big warning signal. If sufficient folks drop out, the reported outcomes can change into badly distorted.

The research additionally assorted extensively in fee dimension, length, pattern composition, and even how outcomes had been measured. The imply annualized fee was $7,177, equal to a mean earnings enhance of about 39.5 p.c relative to baseline family earnings within the research. Some pilots relied closely on self-reported survey information. Some had been carried out throughout or proper after the COVID interval — when labor markets, safety-net applications, and private choices had been something however regular.

AEI’s conclusion is appropriately cautious: these findings might not generalize to a everlasting, common, nationwide UBI beneath present or future circumstances. That alone ought to cool off lots of the AI-fueled coverage hysteria.

AI Will Displace Jobs. It Will Additionally Create Them

None of this implies AI can be painless. Some jobs will shrink. Some duties will disappear. Some employees might want to retrain, relocate, or rethink their careers. That’s what occurs when productiveness rises and expertise modifications how items and companies are produced. It occurred with mechanization, with computer systems, and with the web. It can occur with AI.

However displacement just isn’t the identical factor as everlasting mass unemployment. That leap is the place the UBI argument falls aside. Economies aren’t fastened piles of jobs. They’re dynamic techniques of discovery, adaptation, and change. When prices fall and productiveness rises, assets transfer. Companies reorganize. Client demand modifications. New occupations emerge. Previous ones evolve. Some disappear. That churn is actual, however so is the difference.

The reply to technological change is to not pay folks for financial resignation. The reply is to make adaptation simpler.

UBI Fails the Economics Check

There’s a cause Ryan Bourne at Cato has argued that UBI just isn’t the reply if AI comes in your job. It confuses a transition downside with a everlasting earnings downside. Worse, it assumes that writing checks can substitute for the incentives, alerts, and institutional circumstances that truly create alternative.

UBI additionally crashes into the funds constraint. As Max Gulker at The Every day Economic system has famous, UBI is usually offered via small pilots and obscure ethical language, however the nationwide arithmetic is ugly. And as Robert Wright in one other AIER piece factors out, “common” shortly means sending cash to many people who find themselves not poor whereas piling huge prices onto taxpayers. (Keep in mind, the nationwide debt is already quickly approaching $40 trillion.)

That’s earlier than attending to the public-choice downside. In idea, UBI supporters typically think about changing the welfare state with one easy money switch. In actuality, authorities applications hardly ever disappear. Bureaucracies defend themselves. Curiosity teams defend carveouts. Politicians promise extra, not much less. So a UBI would seemingly be stacked on high of a lot of the present welfare state, not substituted for it. That isn’t reform. That’s fiscal delusion with higher branding.

A Higher Reply: Take away Limitations to Work

If AI means extra labor-market churn, then coverage ought to give attention to mobility, flexibility, and self-sufficiency. Which means much less occupational licensing, decrease taxes, lighter regulation, fewer profit cliffs, much less wasteful spending, and extra room for entrepreneurship and job creation. The federal government ought to cease making it tougher for folks to pivot.

It additionally means reforming welfare the suitable approach. My proposal for empowerment accounts just isn’t a UBI. It could be focused to folks already eligible for welfare, not common. It could embrace a piece requirement for work-capable adults, not detach earnings from effort. And it might consolidate fragmented applications right into a extra versatile account that households management immediately, decreasing forms and decreasing spending over time as extra recipients transfer towards self-sufficiency.

That places it a lot nearer to the classical liberal perception behind changing bureaucratic management with direct help, whereas avoiding the deadly error of turning all the nation right into a everlasting switch state. As Artwork Carden reminds us at The Every day Economic system, there’s a lengthy mental historical past behind cash-based help. However right now’s UBI politics aren’t actually about shrinking the state. They’re principally about increasing it as a result of elites concern AI.

Don’t Make Dangerous Coverage Out of Concern

The UBI revival tells us much less about AI than it does about politics. New expertise arrives, uncertainty rises, and too many policymakers attain for the federal checkbook as if it had been a magic wand. It’s not.

After 122 native experiments, the case for UBI remains to be weak. The very best proof doesn’t present a jobs renaissance. The bigger research present employment declines. The broader proof base is riddled with small pattern sizes, excessive attrition, and restricted generalizability. That may be a flimsy basis for a everlasting nationwide entitlement.

AI will change work. It is not going to repeal economics. The very best response just isn’t fear-driven common dependency. It’s a freer financial system with stronger incentives to work, save, make investments, adapt, and prosper.