Social Safety is drifting towards a cliff, and Congress retains pretending the shortfall will repair itself. It received’t.

Absent reform, advantages might be minimize throughout the board by roughly 23 p.c inside six years. That end result would hurt retirees who rely upon Social Safety probably the most — whereas barely affecting the residing requirements of those that don’t want monetary help in outdated age.

There’s a higher possibility: cut back distributions to the wealthiest retirees, preserving them for these most depending on advantages.

This shouldn’t be a radical thought. Authorities earnings transfers must be focused to those that want monetary help — not used to subsidize consumption amongst well-off seniors on the expense of youthful working Individuals. This strategy is grounded in what Social Safety was meant to do within the first place: “give some measure of safety to the typical citizen and to his household in opposition to…poverty-ridden outdated age,” in the phrases of Franklin D. Roosevelt.

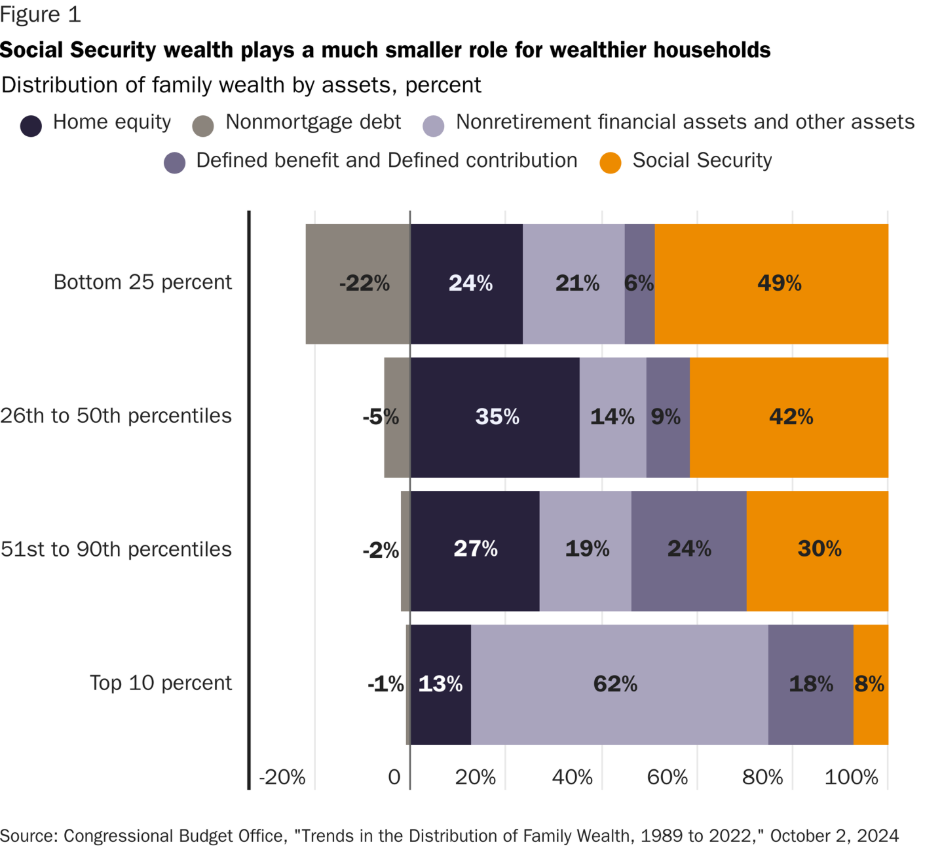

A report by the Congressional Finances Workplace, titled “Developments within the Distribution of Household Wealth, 1989 to 2022,” elucidates the position that Social Safety performs in complete family wealth. By counting not simply monetary property and residential fairness, but in addition the current worth of future Social Safety advantages, it turns into clear that Social Safety represents a considerable share of complete sources for lower-wealth households and solely a marginal share for rich households.

For households within the backside quarter of the wealth distribution, accrued Social Safety advantages account for about half of every part they personal. Social Safety represents solely about eight p.c of complete property for the highest 10 p.c, in comparison with holdings in monetary property, actual property, and enterprise fairness (see Determine 1). But beneath present regulation, rich retirees who declare at age 70 can nonetheless obtain annual Social Safety advantages exceeding $62,000 — roughly 4 occasions the poverty threshold for seniors.

That is an upside-down security internet. When automated profit cuts kick in in 2032, the retirees who rely most on Social Safety might be damage probably the most, whereas rich households will scarcely discover the change.

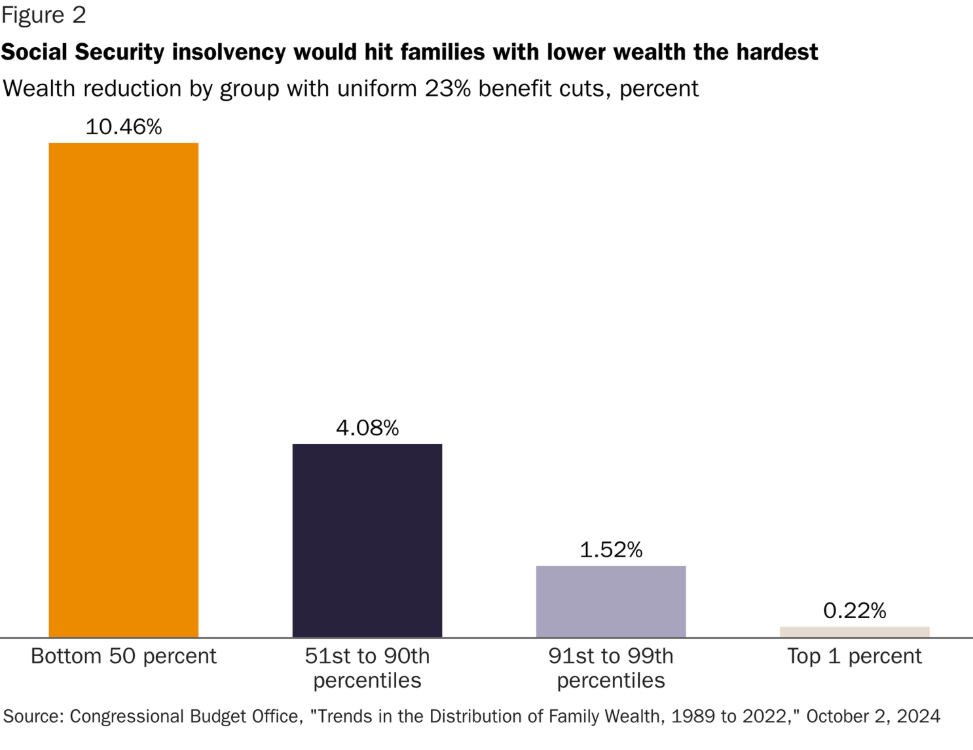

In response to the CBO, that uniform 23-percent minimize would cut back the overall wealth of households within the backside half of the distribution by greater than 10 p.c. For the highest one p.c, the hit could be barely noticeable: about two-tenths of 1 p.c (see Determine 2).

This end result will not be inevitable; Congress can goal profit reductions the place they’re most simply absorbed.

Opponents of top-end profit reductions argue that Social Safety is an earned profit, not welfare, and that reducing advantages for prime earners violates that precept. They’re proper about one factor: staff pay payroll taxes with the expectation of receiving advantages. However that expectation was by no means a assure of open-ended, inflation-beating returns — particularly for retirees who already take pleasure in substantial personal wealth.

Social Safety, whether it is to exist in any respect, ought to concentrate on stopping old-age poverty, not present rich retirees with an ever-growing worker-funded annuity layered on prime of considerable personal financial savings. When advantages develop sooner than inflation and stream disproportionately to those that don’t want them, this system drifts away from its said function and turns into more and more tough to justify.

The answer will not be larger payroll taxes. Eliminating the payroll tax cap would push marginal tax charges above 60 p.c in some states, decreasing work and innovation, whereas nonetheless failing to focus on advantages the place they matter most. Rising payroll taxes for all staff would deprive youthful working households of sources with which to develop their fortunes and construct their very own futures.

Neither is the answer extra borrowing. Social Safety is already projected to add trillions to federal deficits over the subsequent decade. Borrowing to protect full advantages for rich retirees is fiscally reckless and economically pointless.

The smart path ahead is focused profit restraint.

Which means:

- Slowing the expansion of preliminary advantages for larger earners by adjusting the profit system and indexing these preliminary advantages to costs fairly than wages.

- Utilizing a extra correct measure of inflation for cost-of-living changes for ongoing advantages, and phasing out changes fully for high-income retirees.

- Adjusting retirement ages to replicate longer life expectancy, with protections for staff who really can’t work longer — which is the goal of the incapacity element of Social Safety.

In observe, these modifications quantity to a gradual shift away from an earnings-related profit and towards a flat, anti-poverty cost. If Social Safety goes to persist, its position must be restricted to what market earnings and personal financial savings can’t reliably present. Each step that trims extreme advantages on the prime strikes this system nearer to that defensible boundary.

Congress ought to act to forestall across-the-board profit cuts, with out extra deeply indebting youthful generations, nor sucking up extra sources from working Individuals. As an alternative, lawmakers ought to focus reforms the place they do the least hurt and probably the most good — by trimming earned advantages on the prime to safe endangered advantages for these on the backside.

It might not be “truthful,” however it’s the one believable path ahead. The objective of reform shouldn’t be to protect Social Safety in its present type, however to forestall the worst outcomes. Preserving advantages for individuals who rely upon this system, whereas slowing profit development for individuals who don’t, is the one strategy to cut back Social Safety’s position as a reverse switch from youthful staff to rich retirees who don’t want the help.