On this submit we offer a measure of “international” r* utilizing knowledge on short- and long-term yields and inflation for a number of nations with the method developed in “World Developments in Curiosity Charges” (Del Negro, Giannone, Giannoni, and Tambalotti). After declining considerably from the Nineteen Nineties to earlier than the COVID-19 pandemic, international r* has risen however stays nicely beneath its pre-Nineteen Nineties stage. These conclusions are primarily based on an econometric mannequin known as “stylish VAR” that extracts widespread traits throughout a mess of variables. Particularly, the widespread development in actual charges throughout all of the nations within the pattern is what we name international r*. The submit relies on the dialogue of an insightful paper by Lukasz Rachel on the drivers of r* offered on the Brookings Papers on Financial Exercise Fall 2025 convention.

Is There a World R*? Cross-Nation Convergence in R*

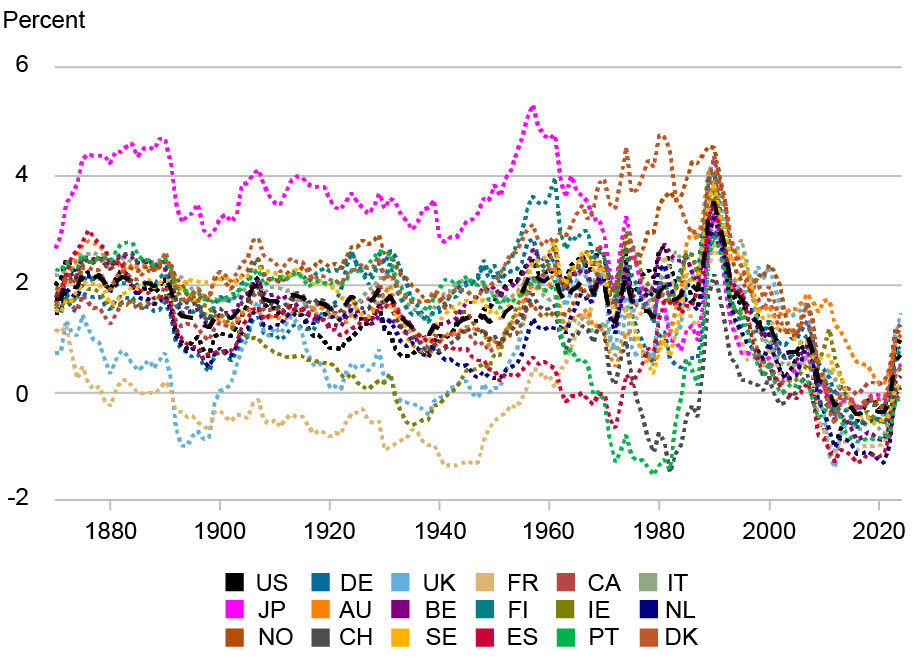

The chart beneath plots estimates of r* utilizing macroeconomic knowledge for the eighteen developed nations included within the Jordà-Schularick-Taylor Macrohistory database. It exhibits that earlier than the Eighties there’s lots of dispersion in r* throughout nations. However after the late Eighties this dispersion disappears unexpectedly, arguably because of monetary market integration. Subsequently, after the late Eighties, we are able to really discuss of a international r*, for the reason that traits in actual charges are one and the identical throughout superior nations. The necessary implication of this discovering, which was first documented in “World Developments in Curiosity Charges,” is that each the decline in r* from the Nineteen Nineties to earlier than COVID and the post-COVID rise that’s evident from the chart are international phenomena.

World Convergence in R*

Notes: The chart plots the posterior median estimates of r* for the eighteen nations within the pattern, particularly Australia, Belgium, Canada, Denmark, Finland, France, Germany, Eire, Italy, Japan, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, the U.Okay., and the U.S. The estimates have been ready for the Fall 2025 Brookings Papers on Financial Exercise (BPEA), © The Brookings Establishment

The Decline, and Latest Rise, within the World (and U.S.) R*

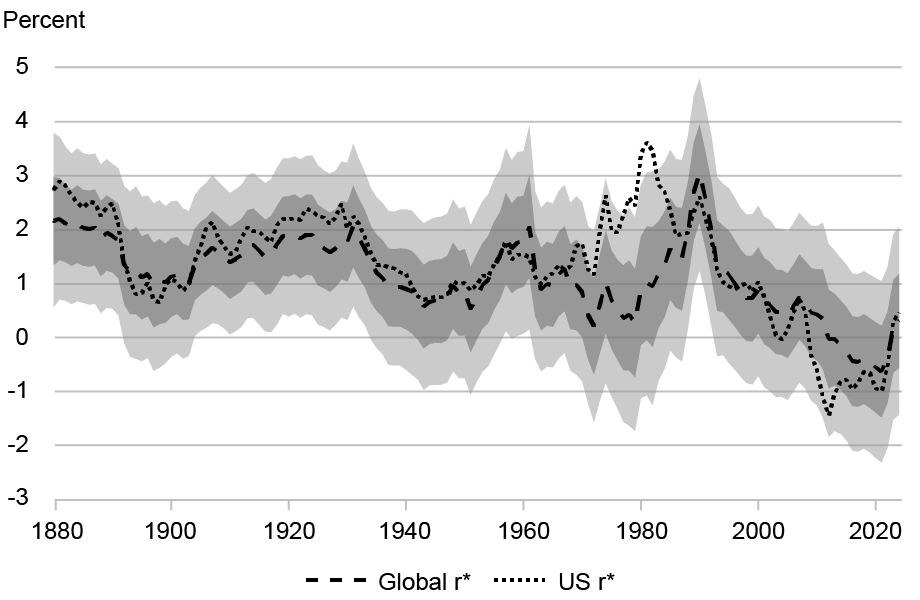

The dashed black line within the chart beneath exhibits the posterior median of world r* with the shaded areas exhibiting the 68 and 95 % posterior protection intervals. The dotted black line exhibits the posterior median of U.S. r*. In line with the mannequin, international r* fell from about 3 % within the early Nineteen Nineties to beneath 0 % after the monetary disaster. It continued declining within the 2010s after which rose by about 1 share level after COVID. By and enormous, the U.S. r* has tracked international r* for the reason that late Eighties, besides that it declined comparatively extra within the aftermath of the monetary disaster. By 2024, the top of the pattern, the median posterior estimates of each international and U.S. r* are round 0.5 % (extra exactly, 0.31 and 0.46). This determine is broadly in line with “the GDP-weighted common of estimates of r-star for … Canada, the Euro Space, the UK, and america,” in response to a current presentation by New York Fed President and CEO John C. Williams, though the U.S. r* level estimate is a bit beneath present estimates of U.S. r* from the well-known Laubach-Williams and Holston-Laubach-Williams fashions, that are about 1 %. Nonetheless, the big posterior protection intervals proven within the chart are there to remind us that extracting development from cycle is a troublesome activity, and that one ought to take level estimates with greater than a grain of salt. The 68 % posterior protection intervals for each international and U.S. r* vary from about -0.5 to above 1 %, whereas the 95 % intervals vary from about -1.5 to above 2 %.

The World and the U.S. R*

Notes: The dashed black line exhibits the posterior median of world r* and the shaded areas present the 68 and 95 % posterior protection intervals. The dotted black line exhibits the posterior median of U.S. r*. The estimates have been ready for the Fall 2025 Brookings Papers on Financial Exercise (BPEA), © The Brookings Establishment

Even when the stage of r* could be very unsure, the mannequin is ready to detect modifications in r* over time with larger statistical confidence. The primary row of the desk beneath reviews the decline in international and U.S. r* from 1990 to 2019, by our calculations. The median estimate of the decline is about 3.5 share factors for each the world and the U.S. Though the width of the 95 % posterior protection intervals (in parentheses) point out that the precise magnitude of the decline is unsure, there isn’t a query statistically that such a decline in r* has taken place from the Nineteen Nineties to earlier than COVID: the posterior likelihood that the change is lower than zero is larger than 97.5 %, as indicated by the three stars subsequent to every quantity.

Pre- and Submit-COVID Adjustments in R*

| World R* | U.S. R* | |||

| 1990-2019 | 2019-2024 | 1990-2019 | 2019-2024 | |

| Baseline mannequin | ||||

| r* | -3.52*** | 0.79*** | -3.27*** | 1.11*** |

| (-4.94, -2.09) | (0.07, 1.49) | (-5.13, -1.36) | (0.18, 2.06) | |

| Comfort yield mannequin | ||||

| r* | -3.83*** | 1.01*** | -3.11*** | 1.14*** |

| (-5.41, -2.27) | (0.30, 1.70) | (-4.45, -1.75) | (0.42, 1.86) | |

| cy | -1.58*** | 0.35 | -0.85** | 0.49* |

| (-2.64, -0.50) | (-0.17, 0.86) | (-1.57, -0.11) | (-0.05, 1.03) | |

| Different | -2.36*** | 0.65** | -2.26*** | 0.65** |

| (-3.55, -0.98) | (0.08, 1.22) | (-3.55, -0.98) | (0.08, 1.22) | |

Notes: For every development, the desk reviews the posterior median, with the 95 % posterior protection interval in parentheses. Statistical significance is indicated with *, **, ***, if the posterior likelihood that the change within the development is beneath (for the 1990-2019 interval) or above (for the 2019-24 interval) zero is larger than 90, 95, or 97.5 %, respectively. The estimates have been ready for the Fall 2025 Brookings Papers on Financial Exercise (BPEA), © The Brookings Establishment

Each the desk and the charts above additionally level to a statistically important rise in each international and U.S. r* within the post-COVID interval: of about 0.8 share level for the worldwide r* and just a little greater than 1 share level for the U.S. r*. It is very important comment that the magnitude of the rise is smaller than that of the pre-COVID decline, therefore r* stays nicely beneath what it was within the Nineteen Nineties. To the extent that one believes the mannequin’s message of a post-COVID enhance in r*, it begs the query of what’s driving it. For the reason that enhance isn’t just a U.S. phenomenon however international—the primary chart within the submit exhibits that r* rose in just about all developed nations—its drivers higher be international as nicely. Purely country-specific explanations for the rise in r* is probably not the entire story.

In earlier analysis, a few of us have argued that a rise within the international comfort yield—that’s, the comfort for security and liquidity that applies to all superior economies’ authorities bonds—is a crucial driver of the pre-COVID decline in r*. In different phrases, buyers’ urge for food for security (and liquidity) drove authorities bond yields throughout superior economies down between 1990 and 2019. To what extent did a sudden decline within the comfort yield between 2019 and 2024 drive r* up?

The underside panel of the desk above decomposes modifications in r* right into a element attributable to the comfort yield (“cy”) and a element attributable to different drivers (“Different”). The desk exhibits that certainly the rise within the comfort yield explains about one-third of the decline in r* each for the U.S. and the world between 1990 and 2019. The decline within the comfort yield for presidency bonds additionally explains one-third to one-half of the post-COVID rise in r*, though it isn’t exactly estimated. This decline, which within the U.S. is mirrored in a compression of company bond spreads, displays the truth that for a wide range of causes, probably together with the surge in authorities debt throughout superior economies, the enchantment of presidency bonds within the U.S. and world wide by way of security and liquidity has declined. On the identical time, the desk exhibits that this decline is clearly not your complete story: the change within the the rest is bigger and statistically extra important than the change in “cy.”

If not the comfort yield, what explains the post-COVID rise in r*? Two believable candidates are: a forthcoming artificial-intelligence-driven uptick in productiveness development and future surges in debt-to-GDP, probably pushed by a perceived unwillingness on the a part of governments in superior economies to boost taxes to cope with the demographic transition, and/or by greater anticipated army spending. Rachel’s Brookings paper considers these eventualities and exhibits that each elements may nicely be driving the rise in r*, though the abruptness of the rise is more durable to rationalize within the mannequin.

In sum, we discover that r* has risen by about 1 share level within the U.S. and in superior economies after COVID, and that about one-third of the change could also be because of a decline within the comfort yield for presidency bonds. The r* estimates mentioned on this submit, and the replication code, can be found on this GitHub web page. We hope to replace these estimates as new knowledge turns into accessible.

Marco Del Negro is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Elena Elbarmi is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Michael Pham is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Tips on how to cite this submit:

Marco Del Negro, Elena Elbarmi, and Michael Pham, “The Submit‑Pandemic World R*,” Federal Reserve Financial institution of New York Liberty Avenue Economics, February 25, 2026, https://doi.org/10.59576/lse.20260225

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).