The Federal Reserve Financial institution of New York’s Middle for Microeconomic Information just lately launched its Quarterly Report on Family Debt and Credit score for the fourth quarter of 2025, revealing continued progress in family debt balances. Mixture family debt balances rose by $191 billion to achieve $18.8 trillion, marking a $4.6 trillion enhance because the finish of 2019. Mortgage balances grew by $98 billion to $13.2 trillion, whereas bank card debt elevated by $44 billion to $1.28 trillion. Bank card and auto mortgage delinquency charges seem to have stabilized, albeit at elevated charges. In contrast, the delinquency price for mortgages—though nonetheless close to low ranges on a longer-term foundation—has been steadily rising over the previous few years. Underlying these combination figures, nevertheless, there are notable variations in mortgage credit score efficiency throughout locations with completely different earnings ranges and labor and housing market dynamics. This evaluation, in addition to the Quarterly Report on Family Debt and Credit score, are based mostly on nameless credit score report knowledge from Equifax.

Whereas the inventory of mortgage balances are held by debtors with sturdy credit score profiles relative to historic requirements, mortgage delinquency charges elevated within the fourth quarter. This deterioration has been most pronounced amongst debtors residing in lower-income zip codes. As an example this sample, we use zip-code degree adjusted gross earnings from the IRS Statistics of Revenue and categorize debtors into 4 earnings teams of equal dimension.

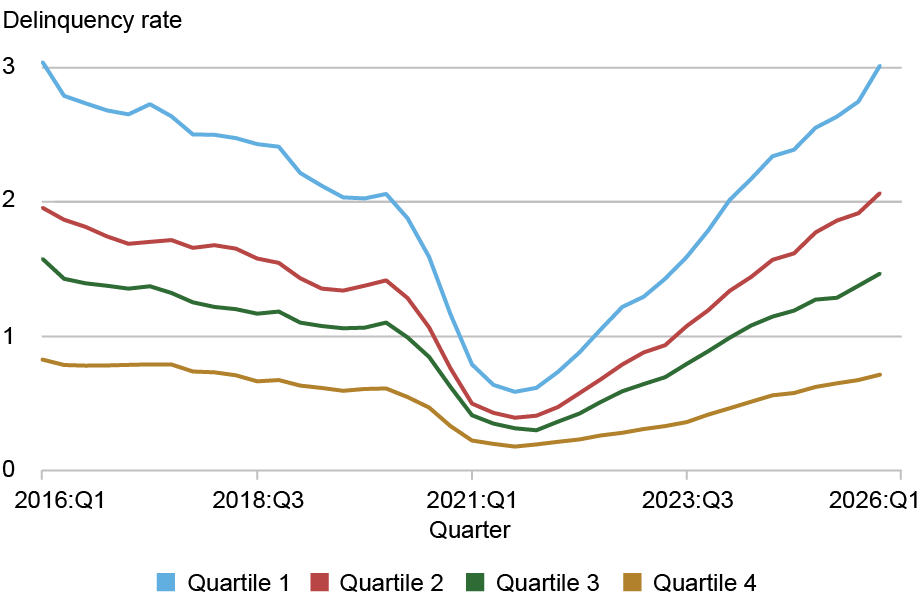

The chart under breaks out the brand new 90+ days delinquency charges by these earnings teams. Whereas debtors within the lowest-income zip codes (quartile 1) have seen their 90+ day delinquency charges surge since 2021—rising from roughly 0.5 p.c to almost 3.0 p.c by late 2025—these within the highest-income areas (quartile 4) proceed to keep up traditionally decrease delinquency charges. Though monetary misery seems to be deepening for households in lower-income areas, debtors in higher-income areas seem largely insulated from these pressures, not less than as measured by mortgage delinquency. The center-income quartiles present intermediate tendencies, with delinquency charges rising however not as precipitously as for the bottom earnings group.

Mortgage Delinquency Charges Return to Ranges of Ten Years In the past

Notes: The chart plots new 90+ days delinquent mortgage balances by zip-income quartile. The bottom-income quartile is quartile 1; the highest-income quartile is quartile 4. Mortgage delinquency charges are at an annual price, summing over the 4 quarters.

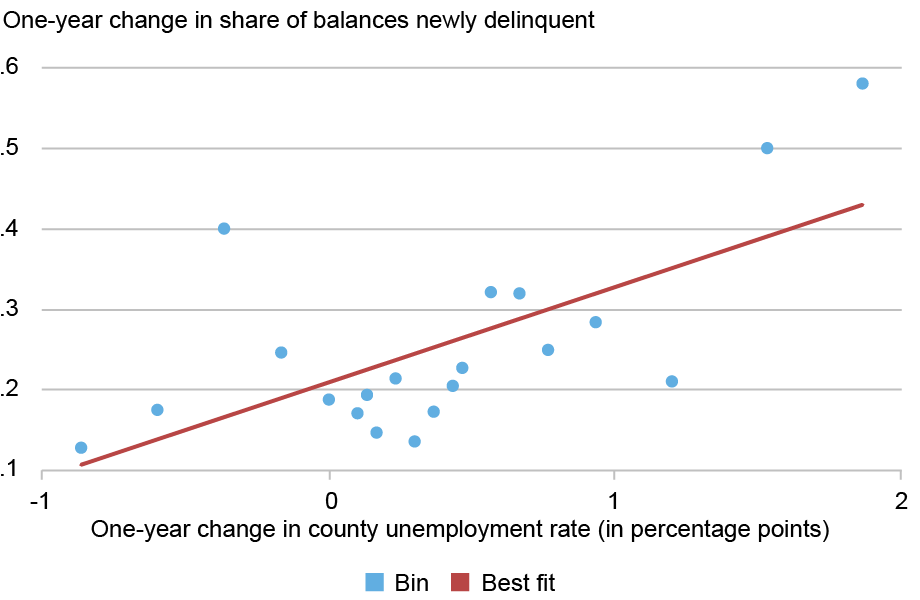

We subsequent look at some potential components which may be contributing to disparities in mortgage efficiency. Might worsening regional labor markets be related to debtors’ lack of ability to stay present on their money owed? The unemployment price nationally bottomed out at 3.4 p.c in April 2023 however has risen about 1 share level since then. Nonetheless, there’s appreciable regional heterogeneity: two-thirds of counties have seen their native unemployment charges rise, and 5 p.c of the inhabitants lives in counties the place unemployment charges have risen by greater than 1.6 share factors (these counties are disproportionally positioned in Florida and Minnesota). The chart under presents a binned scatter plot that reveals a correlation between native labor market deterioration and rising mortgage delinquency charges. We divide counties into twenty teams of equal inhabitants based mostly on their one-year change in unemployment price and compute how mortgage delinquency flows have developed for every group. Counties experiencing the steepest will increase in unemployment noticed a notable worsening in mortgage delinquency by practically 0.6 share factors over the previous yr. In distinction, in counties the place unemployment charges have remained secure or declined, the rise in newly delinquent mortgages has been comparatively modest—round 0.2 share factors. The upward-sloping fitted line illustrates this relationship, suggesting that as native labor markets weaken, households more and more battle to stay present on their mortgage obligations.

Counties with Rising Unemployment Charges Expertise Rising Mortgage Delinquencies

Notes: Counties are grouped into twenty bins based mostly on the change within the unemployment price, with the median change inside every bin reported on the x-axis. Bins are weighted utilizing 2022 county inhabitants from the ACS. Circulation delinquency charges are calculated by grouping debtors by bins of county unemployment change.

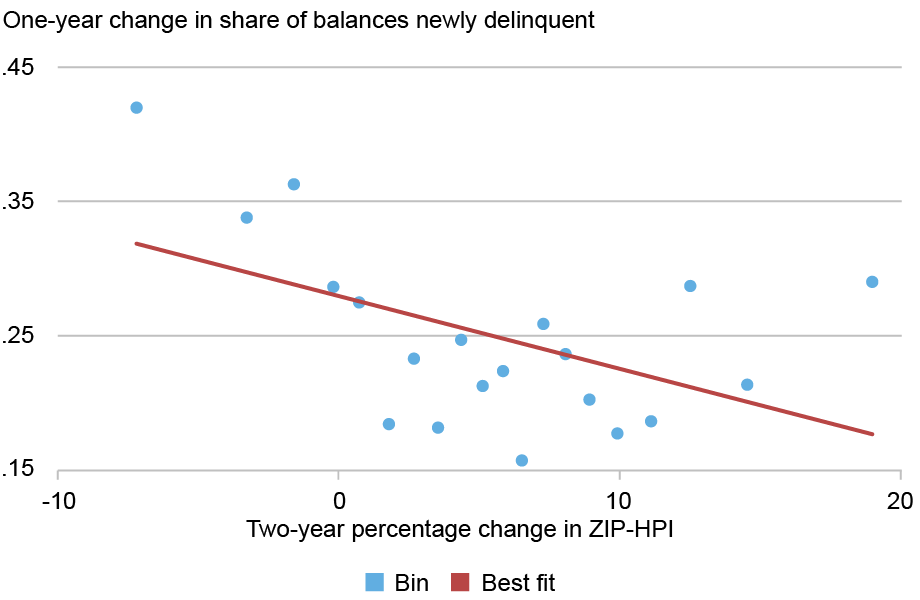

Subsequent, we take into account whether or not native housing market circumstances could assist clarify differential efficiency in mortgage compensation. As of November 2025, house costs in america have been up by 1.0 p.c nationally because the earlier yr however the nationwide change masks monumental regional variation. After we take into account a extra regional look into the evolution of house costs, we see that some areas of the nation, resembling alongside the Gulf Coast of Florida, have seen pronounced declines in house costs. The chart under plots the change in space house costs, utilizing the Cotality/CoreLogic Residence Worth Indices on the zip-code degree, in opposition to the change in mortgage delinquency charges. Mortgage delinquency charges are negatively related to the tempo and course of house worth modifications, though this relationship is just not as sturdy as the connection with unemployment.

Counties with Falling Home Costs Expertise Rising Mortgage Delinquencies

Notes: Zip codes are grouped into twenty bins based mostly on the change in Residence Worth Index (HPI), with the median change inside every bin reported on the x-axis. Bins are weighted utilizing 2022 inhabitants from the ACS on the zip code tabulation space (ZCTA). Circulation delinquency charges are calculated by grouping debtors by bins of ZIP-HPI change.

It is very important word that total, mortgages proceed to carry out nicely by historic requirements and have risen just lately solely after having reached artificially low ranges through the pandemic because of the stimulus and forbearances obtainable to debtors at the moment. On common, about 1.3 p.c of mortgage balances turned severely delinquent throughout 2025—a share that appears similar to the averages noticed exterior of the interval across the Nice Recession (when delinquencies exceeded 8 p.c). Tight lending requirements for mortgages have been a serious contributor to this enchancment; the median credit score rating of newly originated mortgages has remained persistently above 750 since 2009. Nonetheless, in lower-income areas and in areas experiencing worsening labor market or housing market circumstances, we’re seeing mortgage delinquencies develop at a quick tempo.

Andrew F. Haughwout is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Donghoon Lee is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Daniel Mangrum is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Joelle Scally is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this put up:

Andrew F. Haughwout, Donghoon Lee, Daniel Mangrum, Joelle W. Scally, and Wilbert van der Klaauw, “The place Are Mortgage Delinquencies Rising the Most?,” Federal Reserve Financial institution of New York Liberty Road Economics, February 10, 2026, https://doi.org/10.59576/lse.20260210

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).