The Federal Reserve’s 2022-23 tightening cycle concerned the usage of two financial coverage instruments: adjustments in administrative charges and adjustments within the measurement of its stability sheet. This publish highlights the outcomes of a current Employees Report that explores how these instruments have an effect on cash market situations. Utilizing confidential trade-level information, we discover that each instruments have important results on the pricing of funds sourced via repo. These outcomes counsel that the Fed can handle how financing situations are affected even because it influences financial situations. For instance, the Fed can decrease its administrative charges to loosen financial situations, whereas shrinking its stability sheet to preserve financing situations within the cash markets.

Background

Our evaluation focuses on Treasury repurchase agreements (repo), a crucial monetary market used to safe funding and supply liquidity, with an estimated measurement of over $5 trillion excellent within the first half of 2024 (see the appendix of this white paper). Secured funding trades within the U.S. are sometimes documented as repos, and inside repo, trades involving Treasury securities are the dominant sort. Utilizing information on Treasury repo, then, offers a consultant take a look at secured funding situations within the U.S.

The U.S. Treasury’s Workplace of Monetary Analysis’s (OFR) centrally cleared repo assortment offers such information. This assortment captures most interdealer buying and selling. Moreover, a portion of dealer-to-client repo transactions are gathered via the central counterparty’s Sponsored Service program, offering a window on pricing of trades between sellers and their mutual fund and hedge fund purchasers (see this Employees Report for extra particulars on Sponsored Service).

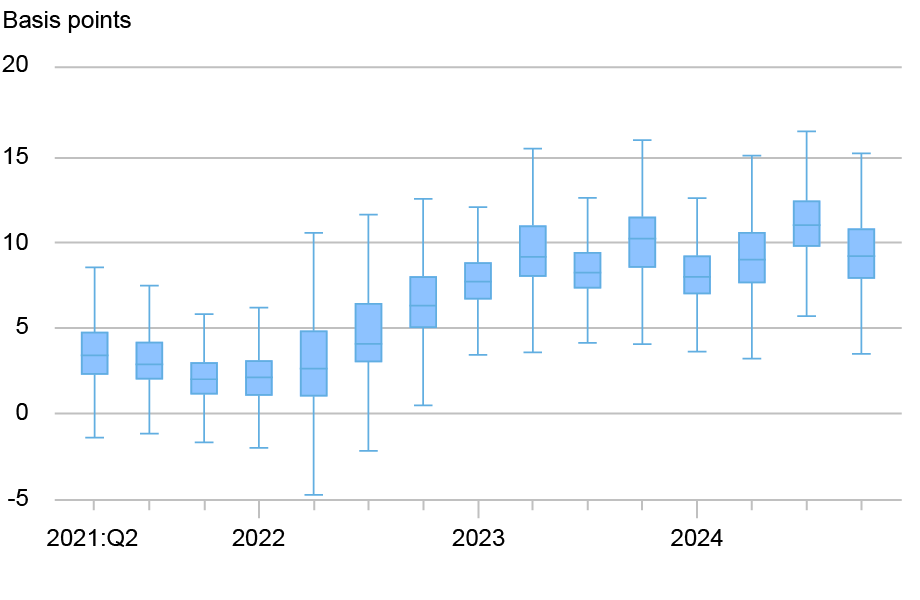

Sellers are the primary intermediaries in secured funding markets, borrowing from cash-rich traders similar to cash market mutual funds and lending to levered purchasers similar to hedge funds (see this complete report on sellers’ middleman actions). The OFR information permit for the development of the spreads charged by sellers to intermediate funds, as we observe the repo price sellers’ cost to lend funds to levered purchasers in addition to the charges paid to borrow funds from mutual funds. The chart under exhibits the distribution of these spreads for in a single day Treasury repo for every quarter from 2020 to 2024.

Distribution of Spreads Charged by Sellers, by Quarter

Notes: This chart is a box-and-whisker plot of the typical every day spreads charged by sellers to intermediate funding amongst purchasers by quarter. Spreads are computed as the speed charged by sellers to lend funds to purchasers in an in a single day Treasury repo minus the speed paid by sellers to borrow funds from purchasers in an in a single day Treasury repo. The three traces of the field signify the twenty fifth, fiftieth, and seventy fifth percentiles of the typical every day unfold. The decrease whisker is the same as the twenty fifth percentile minus 1.5 instances the interquartile vary (seventy fifth minus twenty fifth percentiles). The higher whisker is equally outlined. The plot excludes outdoors values.

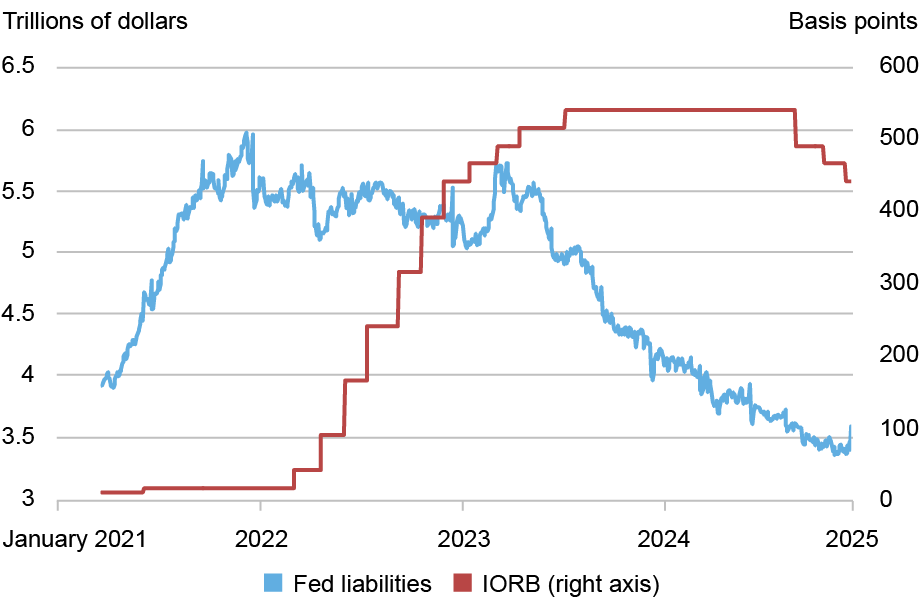

These statistics counsel that sellers charged wider spreads to intermediate funding with the tightening of financial coverage, which started in March 2022. The chart under shows the adjustments to financial coverage, each when it comes to adjustments to the Fed’s administrative price of curiosity on reserve balances (IORB) and to the Fed’s stability sheet (our measure is the quantity of reserves that banks maintain at Federal Reserve Banks plus the amount of money positioned on the Federal Reserve in a single day reverse repo facility, hereafter Fed liabilities). Over the pattern interval, IORB elevated from 15 to 540 foundation factors, with giant steps up in 2022. On the finish of the pattern, within the final half of 2024, there are three decreases in IORB. Fed liabilities are hump-shaped: Beginning at about $4 trillion, they rise steeply in 2021 to virtually $6 trillion. They then keep roughly flat via the start of 2023, earlier than steadily falling via 2024, reaching $3.5 trillion by December 2024.

Financial Coverage Adjustments over the Pattern Interval

Notes: This chart shows the evolution of IORB and the dimensions of Federal Reserve liabilities as measured by the quantity of reserves that banks maintain at Federal Reserve Banks plus the amount of money positioned on the Federal Reserve in a single day reverse repo facility.

Evaluation

Our evaluation focuses on how financial coverage impacts the price to sellers to intermediate funding amongst purchasers. As intermediaries, sellers face dangers, even for short-term trades the place funding is secured by high-quality collateral (see this Treasury Market Practices Group white paper for a distillation of those dangers). To mitigate these dangers, sellers usually maintain a buffer of liquid securities, the place the price of holding this buffer needs to be mirrored within the unfold charged by the seller.

We time period this price the liquidity danger premium and observe that this premium ought to differ with the chance price of holding money. Adjustments in financial coverage, each when it comes to IORB and Fed liabilities, change the chance price of holding money. Our predominant empirical train, then, is to estimate how adjustments in each IORB and Fed liabilities affect the spreads charged by sellers to intermediate funds. The figuring out assumption of this evaluation is that the choice to alter charges or Fed liabilities is exogenous to the spreads charged by sellers, a believable assumption for this era of research when the Fed needed to maneuver from considerable to ample reserves.

Our predominant outcomes are that each a rise in IORB or a lower in Fed liabilities raises the liquidity danger premium, driving up the price of intermediating funding. The estimates suggest {that a} one customary deviation enhance in IORB, or 226 foundation factors, drives up the liquidity danger premium by 2.1 to three.5 foundation factors. A one customary deviation enhance in Fed liabilities ($750 billion) drives down the premium by 1.6 to 2.5 foundation factors. These are economically important results, as evidenced by the truth that the typical unfold sellers cost purchasers to intermediate funding within the pattern interval is 7.5 foundation factors.

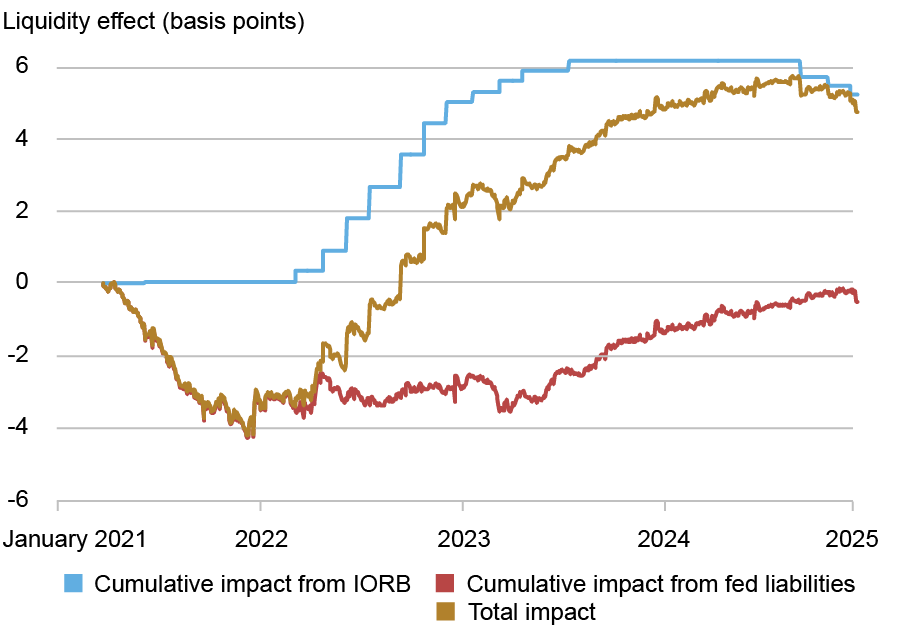

The cumulative impression of every financial coverage software on the liquidity danger premium is illustrated within the chart under. The estimated cumulative results naturally mirror their respective financial coverage instruments, though the magnitudes barely differ due to the estimated nonlinear results. For instance, a $1 billion change in Fed liabilities has a bigger estimated impact on the liquidity danger premium when IORB is low in comparison with when IORB is excessive.

Estimated Cumulative Impact of Financial Coverage on the Liquidity Danger Premium

Notes: This chart shows the cumulative impact of financial coverage on the liquidity danger premium as implied from the estimated outcomes, the place the cumulative impact is ready to zero in the beginning of the pattern. A decomposition can be supplied, individually exhibiting the impact of adjustments to IORB and Fed liabilities on the liquidity danger premium.

Takeaway

Over the past financial tightening interval, the Fed’s enhance in IORB and reduce in Fed liabilities each drove up the chance price of cash, pushing up the liquidity danger premium. A key perception from the outcomes is the potential for a wider vary of outcomes on how the Fed impacts the cash markets. For instance, in a hypothetical scenario the place the financial system wants help and the extent of economic sector leverage is regarding, the Fed has instruments obtainable to offset each points: decreasing rates of interest and reducing its liabilities. Reducing charges would bolster the financial system via the same old channels, and a big sufficient lower in Fed liabilities would end in a widening of the unfold sellers cost purchasers to intermediate funds, dampening total monetary sector leverage. We will quantify these results on the liquidity danger premium. Utilizing the values of charges and Fed liabilities on the finish of the pattern interval, our outcomes suggest {that a} 100-basis-point lower in IORB and a $400 billion lower in Fed liabilities would have largely offsetting results on the liquidity danger premium.

Adam Copeland is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Owen Engbretson is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The best way to cite this publish:

Adam Copeland and Owen Engbretson , “The Fed Has Two Instruments to Affect Cash Market Situations ,” Federal Reserve Financial institution of New York Liberty Road Economics, April 6, 2026, https://doi.org/10.59576/lse.20260406

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).