Final Friday, I met a journalist in Tokyo and we mentioned amongst different issues, the outcomes of the newest Nikkei/JCER ‘Economics Panel’, which was performed between November 13 and November 18, 2025. The panel entails “questionnaires” being “despatched to roughly 50 economists to collect their evaluations of varied financial insurance policies. The intention is to advertise deeper and extra energetic discussions on financial coverage by clearly conveying the consensus and variations of opinion amongst specialists, together with presenting particular person feedback from every economist.” The outcomes are fairly placing and display that the Japanese tutorial economics occupation is mired in harmful Groupthink which means the occupation is failing to contribute in any efficient and useful solution to advancing the well-being of the Japanese inhabitants or offering insights into how the nation can meet its appreciable and instant challenges.

I mentioned this kind of course of by analysing a College of Chicago survey in 2019 that claimed the outcomes display how silly Trendy Financial Concept (MMT) is.

After all, the survey had nothing to do with the physique of labor we check with as MMT and so was a dishonest train.

The survey respondents have been additionally too insular to understand they have been being duped by these conducting the survey – on condition that none talked about that the 2 questions that have been below the heading ‘Trendy Financial Concept’ bore no resemblance to any core MMT statements or learnings.

Crippling Groupthink dominated.

See this weblog put up for extra particulars – Pretend surveys and Groupthink within the economics occupation (March 19, 2019).

The Nikkei-JCER ‘Economics Panel’ is somewhat completely different as a result of the questions weren’t as clearly rigged and the panel was considerably extra numerous.

However the truth stays that the mainstream dominance was very evident and the mainstream solutions have been dogmatic whereas the panelists who demurred considerably have been much less assured of their reasoning.

You’ll be able to be taught extra in regards to the composition of the panel from this web page – About Economics Panel (posted August 14, 2025).

The panel is chosen by “an appointing committee” who’re principally mainstream teachers at Japanese universities.

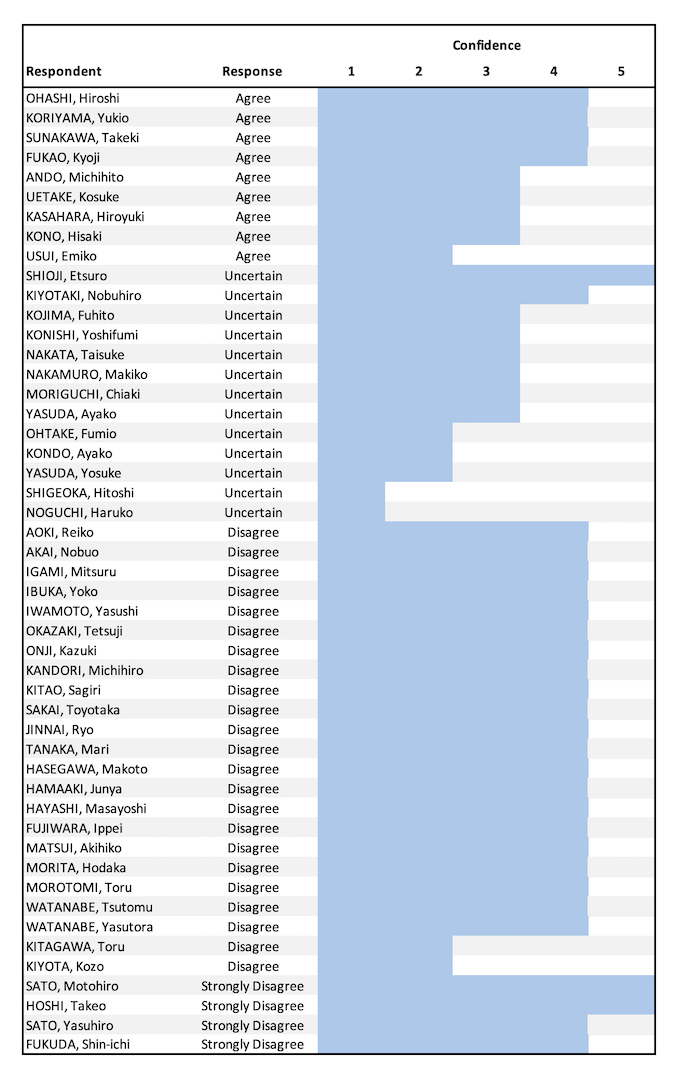

The questions are of the Agree or Disagree kind and “respondents are additionally requested to point their degree of confidence of their solutions on a five-point scale (1 to five, with 5 indicating excessive confidence)”.

There are 50 respondents on the present panel (all Japanese) and drawn from college departments around the globe.

Within the newest survey, there have been 3 questions, one relating as to if the federal government’s cap on working hours has constrained GDP development and one other relating as to if easing the working hours cap would make staff happier.

So underpinning these questions was a dislike of laws that have been designed to cut back the very lengthy working hours that traditionally have outlined Japanese work locations.

The solutions have been blended with no clear pattern.

1. 40 per cent disagreed with the primary query, whereas 18 per cent agreed. 4 per cent strongly disagreed.

2. For query 2, 42 per cent disagreed (4 per cent strongly so), whereas 16 per cent agreed.

There was a big ‘unsure’ group for each questions.

However the query that me essentially the most was the third one.

This had been the subject of the Symposium that I spoke at on the Food plan Constructing in Tokyo on November 6, 2025 and which many Members of the Food plan (Parliament) and their advisers had attended.

The particular query that was requested of the panel was:

Query 3: Making the first stability goal extra versatile from the present single-year foundation is suitable as an strategy to financial and monetary administration.

The context was the truth that the brand new Prime Minister has advocated “accountable proactive fiscal coverage”, which signifies that the:

… strategy to the first stability goal has turn out to be some extent of rivalry

The Major Stability is the distinction between authorities spending web of curiosity funds on excellent debt and taxation income.

The Japanese authorities had turn out to be infested with the mainstream concept that:

As a fiscal soundness purpose, the federal government had aimed for an early achievement of a surplus throughout fiscal years 2025 and 2026.

Upon assuming her position as the brand new Prime Minister, she mentioned that the federal government would interpret this ‘purpose’ as a “multi-year” mixture fairly than attempting to realize stability in any single 12 months.

After all, the federal government deficit (and first stability) has been in deficit since 1992 because of the federal government’s response to the large asset bubble crash in 1991.

The ‘flexibility’ narrative being promoted by Ms Takaichi has despatched many economists and commentators into conniptions, and claims of a ‘Truss’ second have been aired.

On the Symposium, my place was that the precise major stability needs to be ignored and a spotlight needs to be centered on how properly the federal government was progressing to advertise social well-being and environmental sustainability – the important thing MMT building.

Additionally word that after the Survey was performed, the federal government introduced a 21.3 trillion yen stimulus on November 21, 2025.

It’s anticipated that round 50 per cent of that further web authorities spending shall be coated by tax income, given inflation and the booming company income.

Tax income is at document highs, which signifies that the rise within the fiscal deficit shall be significantly lower than the 21.3 trillion yen.

There are different ‘accounting’ offsets similar to dividends coming from government-owned companies and a few non-government subsidies which were refunded by change of circumstance.

They are going to additional lower the precise improve within the fiscal deficit related to the 21.3 trillion stimulus.

Notice I used the time period ‘accounting’ offsets to explain the components that may cut back the change within the fiscal deficit.

An orthodox economist would declare they have been ‘funding’ the spending.

The federal government will improve its spending by 21.3 trillion by crediting varied financial institution accounts and spending will rise by that a lot.

The offsets are simply e-book entries, which implies in an accounting sense the change within the distinction between spending and income shall be lower than the 21.3 trillion yen.

Anyway, again to the query.

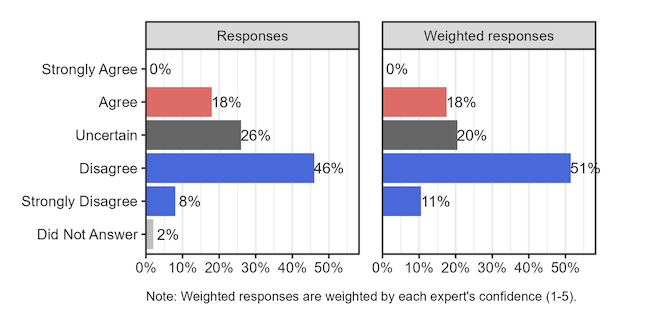

Listed here are the Responses (and Weighted Response – by confidence degree):

So:

When requested whether or not making the first stability goal extra versatile from a single-year foundation is suitable, 54% responded “strongly disagree” or “disagree” (62% after weighting).

I created the next graphic to point out the distribution of the diploma of confidence by response.

I feel it demonstrates how entrenched the mainstream view amongst Japanese economists.

The blue bars vary from 1 to five in keeping with how assured the respondent is of their reply.

Those that agree that flexibility isn’t going to trigger the sky to fall in – a non-mainstream view – are usually not uniformly tremendous assured in that appraisal.

And there are not any respondents who strongly agree.

On the opposite aspect – the 62 per cent towards (both towards or strongly so) are rather more assured of their viewpoint.

I word that such confidence has typically been displayed when characters like this have predicted the worst because of previous fiscal deficits and many others and have systematically been confirmed improper.

Studying from suggestions doesn’t seem like a properly established trait amongst mainstream economists.

That phenomenon is, in fact, a key attribute of Groupthink

The qualitative responses have been additionally fascinating.

A number of respondents indicated they didn’t “have any experience” in macroeconomics – which I discovered fascinating – all ‘unsure’ respondents.

I exploit the time period “standard logic” to point that the individual is absolutely making use of standard (mainstream) logic however isn’t as dogmatic in its utility.

I’ve additionally summarised a number of respondents in every class if their feedback have been comparable.

Among the many respondents agreeing have been statements like (translated from the Japanese):

1. Vital infrastructure, social and environmental challenges require fiscal assist – – pretty standard Keynesian view.

2. Want for fiscal coverage to be conscious of financial fluctuations – pretty standard Keynesian view.

3. Debt ratio falling so no drawback – standard logic.

4. Fiscal enlargement wants to think about bottlenecks in any other case inflation will happen.

5. Fear about market credibility and excellent debt and many others – standard logic.

6. Single-year goal too inflexible – standard logic.

Among the many respondents who have been unsure:

1. Nervous that momentary flexibility will turn out to be everlasting – “weakening of fiscal self-discipline”, “loosening of fiscal self-discipline”, “dangers to fiscal administration” – standard logic.

2. Nervous about the place the spending is being deliberate.

Among the many respondents who disagreed or strongly disagreed:

1. “loosening fiscal self-discipline”.

2. Growing deficit isn’t accountable.

3. Authorities won’t be able to realize PB surplus over a number of intervals.

4. Desires the Prime Minister to resign if a year-to-year PB surplus isn’t achieved.

5. 30 years of deficits ought to finish.

6. “Fiscal self-discipline will turn out to be extra lax”.

7. Flexibility is simply applicable in emergencies (for instance, COVID-19) and different instances compromises the “long-term debt discount objectives”.

8. Not the time to stimulate with unemployment low (Invoice: ignores the truth that there’s excessive underemployment and actual wages are falling).

9. Markets will reject the ‘flexibility’ and confidence shall be undermined.

10. “Reaching a major stability surplus yearly isn’t essentially optimum. Nonetheless, a mechanism is important to forestall limitless expenditure enlargement and keep fiscal soundness” (Invoice: so pursue sub-optimal coverage simply because!).

11. Fiscal state of affairs is now extreme and surpluses are essential.

12. Will trigger rates of interest to rise even additional (Invoice: the inaccurate crowding out argument).

13. IMF says the debt ratio is simply too excessive and additional will increase will “jeopardize fiscal sustainability sooner or later”.

14. In peacetime, a major stability surplus is required.

My abstract is that many of the panel have been mired within the mainstream camp.

Even those that assist flexibility articulated issues about on-going fiscal deficits and wished deficits within the downturn and surpluses within the upturn – the basic deficit dove place.

It was onerous to search out any respondent who articulated a useful finance place – though one or two relying on the nuance of the interpretation might need been leaning in that route.

That’s, the overwhelming majority of respondents answered the query inside a framework the place the logic utilized was all about monetary ratios fairly than fascinated about fiscal coverage by way of its perform – to do actual issues like enhance well-being, advance socially-productive establishments, take care of local weather change, repair up the housing inventory to turn out to be power environment friendly, enhance actual wages and many others.

The panel is caught in mainstream pondering the place deficits are basically constructed as being ‘dangerous’ and a few respondents have been ready to have some dangerous for a time so long as the surpluses got here later.

That group are characterised as being within the ‘stability over the financial cycle’ camp – the place they’re ready to concede some web spending should happen when non-government spending falters, however then the ‘debt’ must be paid again when the economic system is stronger.

That’s completely standard logic.

It fully ignores context and goal.

Not one respondent expressed a view that ongoing fiscal deficits are required to offset the excessive saving charges amongst Japanese households and the low funding fee by firms.

Definitely, Japan receives a constructive revenue injection from its exterior sector, which helps ‘fund’ the saving wishes of the home economic system.

However that clearly isn’t ample and so fiscal deficits need to fill the remaining spending hole to assist ‘fund’ the non-government general saving wishes.

Everytime, the Japanese authorities makes an attempt to cut back the deficit and push for a major stability surplus, the economic system heads into recession.

That actuality signifies that steady fiscal deficits are the norm and fascinating.

And given the size of labour underutilisation (at the moment round 6 per cent, with 2 per cent official unemployment and 4 per cent underemployment) the present deficit is clearly too small.

Therefore the necessity for renewed stimulus.

The opposite side of the feedback by the panel members is that single phrase headlines now function a catch all kind rationalization based mostly on years of conditioning the general public to only settle for superficial evaluation.

So, they will say issues like ‘the markets’ and no additional evaluation is required – the message is the monetary markets are all highly effective and can sink the yen if the federal government doesn’t play ball.

The truth is that the precise reverse is the reality.

The markets are mendicants and the federal government (by the Financial institution of Japan) can dominate the wishes of the markets at any time when it chooses.

Even when we accepted the logic that the bond issuance ‘funds’ the federal government spending, the truth is that the federal government at the moment owns greater than 50 per cent of all excellent Japanese Authorities Bonds and there was no inflationary penalties in consequence.

The inflation that the nation is at the moment experiencing is coming by way of meals costs and that has been as a result of hostile weather conditions throughout current harvests – nothing to do with deficits, bond purchases by the central financial institution and many others.

And the federal government, utilizing the identical logic, might purchase all of the debt if it wished to and due to this fact ‘self fund’ itself with none necessities that the personal bond buyers present funds.

After all, that exposes the mainstream logic anyway.

There’s a want for extra schooling among the many public about these issues – as a result of they’re being duped by these well-paid economists who’re given a nationwide platform by way of panels such because the Nikkei/JCER train.

Conclusion

The Groupthink uncovered by these kinds of workouts may be very placing and tells me that we have now a protracted solution to go in altering the narrative coming from my occupation.

I don’t maintain out a lot hope.

That’s sufficient for at this time!

(c) Copyright 2025 William Mitchell. All Rights Reserved.