International components, like financial coverage charges from superior economies and threat situations, drive fluctuations in volumes of worldwide capital flows and put strain on change charges. The parts of worldwide capital flows which are described as world liquidity—consisting of cross-border financial institution lending and financing of issuance of worldwide debt securities—have sensitivities to threat situations which have advanced significantly over time. This threat sensitivity has been pushed, partly, by the composition and enterprise fashions of the monetary establishments concerned in funding. On this publish, we ask whether or not these identical options have led to modifications within the pressures on foreign money values as threat situations evolve. Utilizing the Goldberg and Krogstrup (2023) Change Market Stress (EMP) nation indices, we present that the options of monetary establishments within the supply international locations for worldwide capital do affect how vacation spot international locations expertise foreign money pressures when threat situations change. Higher shock-absorbing capability in monetary establishments moderates the pressures towards depreciation of currencies throughout adversarial world threat occasions.

Worldwide Capital Stream Pressures and Danger Sensitivity

The normal technique to measure the outcomes of worldwide capital circulation pressures is to trace the habits of nation change charges outlined as models of home foreign money wanted to buy a unit of overseas foreign money. This conventional change price measure masks the a part of the pressures that overseas governments work to mood by making use of instruments like overseas change intervention and financial coverage price modifications. To appropriate this shortcoming, the Goldberg and Krogstrup EMP mannequin represents these interventions in change price depreciation equal models after which supplies a consolidated various to the precise change price change that may be in contrast throughout international locations and over time. By nation, this measure captures a mixture of foreign money depreciation, overseas change intervention, and financial coverage modifications.

The associated International Danger Response index (GRR) estimates the correlation between month-to-month values of the EMP and variations in a measure of threat that, usually, is the VIX index of the implied volatility in S&P 500 inventory index choice costs from the Chicago Board Choices Change (CBOE). Optimistic values point out an inclination towards foreign money appreciation pressures when threat situations worsen, whereas adverse values suggest foreign money depreciation pressures. Analysis exhibits that worsening threat results in appreciation pressures on comparatively secure safe-haven currencies, such because the U.S. greenback, the Swiss Franc, and the Japanese Yen, and depreciation pressures on different currencies.

Through the interval following the worldwide monetary disaster (GFC), the chance sensitivity of world liquidity declined considerably, as mentioned on this latest Liberty Road Economics publish. Have evolving overseas monetary establishment situations formed how a home foreign money is pressured in response to altering threat situations, much like the case for world liquidity flows?

Unpacking EMP Danger Sensitivity Drivers

We use regression evaluation to estimate the connection between the EMP (outlined in depreciation models of the native foreign money versus the U.S. greenback), and the VIX, U.S. financial coverage, and a number of other world and borrowing country-level controls. We use the time period Different Superior Economies (OAEs) to confer with superior economies aside from these which are characterised as so-called protected havens. Regressions use knowledge for a pattern of thirty-eight “international locations” that features eight OAEs, three protected havens, and twenty-seven rising market economies (EMEs) over the interval 2000:Q1-2024:This autumn. The Euro Space is taken into account as a single superior financial system resulting from its shared foreign money.

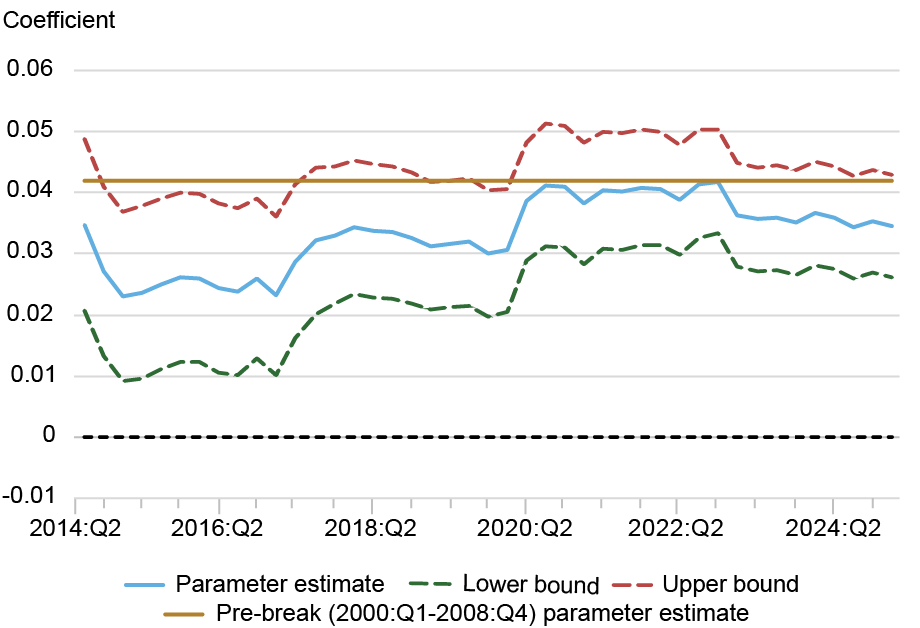

The chance sensitivity of the EMP varies over time for OAEs and EMEs. The panel chart beneath exhibits the post-GFC interval, with a pre-break sensitivity line. Pre-GFC, OAE EMPs had a threat sensitivity of about 4.6 proportion factors. Then, the chance sensitivity declines within the post-GFC interval, remaining beneath pre-GFC ranges via the top of 2024. The sample is analogous for EMEs, though notably the pre-break sensitivity for EMEs is greater at 4.2 proportion factors beneath the EMP measure than the change price at 3.3 proportion factors. (Change price depreciation figures aren’t proven however might be offered upon request.) Through the interval instantly following the GFC, we see a spike in threat sensitivities throughout each OAEs and EMEs. The EMP’s threat sensitivity jumps from 4.2 to 12.3 proportion factors via 2013, reflecting elevated threat sensitivity globally in response to the disaster. Within the following interval, threat sensitivity drops to beneath pre-GFC stage throughout each financial system varieties, probably resulting from tighter regulation ameliorating capital circulation pressures in response to threat. For EMEs, the response to elevated threat is captured extra strongly by the EMP in comparison with what can be measured if the change price alone was thought-about, with the chance sensitivity 3.5 proportion factors for the previous versus 3.1 proportion factors for the latter. For OAEs, the EMP and the change price carry out equally, with a full interval post-GFC sensitivity of two.7 proportion factors beneath the EMP.

Danger Sensitivities Stay Under Pre-Disaster Ranges

EMP (USD): OAE

EMP (USD): EME

Supply: Authors’ calculations.

Notes: The panel chart exhibits the evolution over time of sensitivities to the log (VIX) for foreign money Change Market Stress (EMP) from 2014:Q2-2024:This autumn. For every quarter t, the illustrations present the post-break coefficient (and its 90% confidence interval) obtained by estimating the mannequin with a pattern from 2000:Q1 as much as quarter t, with a break in 2009:Q1. The gold line in every panel represents the pre-break estimate of the sensitivity to VIX. The Different Superior Economies (OAEs) are Australia, Canada, Denmark, Euro Space, Nice Britain, Norway, New Zealand, and Sweden. The Rising Market Economies (EMEs) are Armenia, Bolivia, Brazil, Botswana, Chile, China, Colombia, Czech Republic, Hong Kong, Hungary, Israel, India, Jordan, South Korea, South Africa, Morocco, Mexico, Malaysia, Peru, Poland, Romania, Russia, Singapore, Thailand, Tunisia, Ukraine, and Uruguay. (Three “safe-havens” —Japan, Switzerland, and United States—are a part of the total knowledge pattern, however aren’t included right here).

What’s the position performed by supply nation monetary establishment situations? Specializing in OAEs, we discover that greater financial institution capitalization dampens the chance sensitivity of change market strain, as does decrease leverage of nonbank monetary establishments (NBFI). Specs that embrace measures of monetary establishment well being recommend that for OAEs a rise in financial institution capitalization decreases the EMP sensitivity to threat by 1.5 proportion factors, which is equal to a rise in financial institution capitalization ranges from 5.3 to six.2. This result’s in line with our speculation that higher capitalized banks expertise much less foreign money strain in response to threat. We additionally discover that a rise in NBFI leverage will increase the EMP sensitivity to threat by 1.9 proportion factors, suggesting that extra leveraged NBFI lenders elevate foreign money strain on the borrowing nation.

Are Adjustments in Danger Sensitivity Everlasting or Transitory?

Whereas greater banking sector capitalization within the supply international locations of lending flows lowered threat sensitivity of change market pressures, different drivers of change may be necessary. For instance, we’ve got not taken under consideration the traits of the home monetary establishments concerned in sourcing or receiving worldwide capital flows. Nor have we thought-about the position of micro and macroprudential devices which have been launched to answer cyclical and structural vulnerabilities inside international locations.

Linda S. Goldberg is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Samantha Hirschhorn is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The way to cite this publish:

Linda S. Goldberg and Samantha Hirschhorn, “Monetary Intermediaries and Pressures on Worldwide Capital Flows,” Federal Reserve Financial institution of New York Liberty Road Economics, September 22, 2025, https://doi.org/10.59576/lse.20250922

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).