{kind=link}

Financial institution supervisors, business analysts, and educational researchers depend on a spread of metrics to trace the well being of each particular person banks and the banking system as a complete. Many of those metrics give attention to financial institution solvency—the probability {that a} financial institution will be capable to repay its obligations and thus retain its funding and proceed to provide companies to shoppers, companies, and different monetary establishments. We draw on our latest analysis to explain a brand new solvency metric that’s extra forward-looking, extra well timed, and extra complete in its evaluation of solvency than many present measures.

Financial Capital: Combining Credit score, Liquidity, and Funding Threat

Arguably probably the most broadly used solvency measures are regulatory capital and tangible frequent fairness (TCE), each of that are grounded in U.S. Usually Accepted Accounting Ideas (GAAP). Below U.S. GAAP, many belongings and liabilities on banks’ stability sheets are carried at historic or amortized price moderately than at honest market values. Whereas credit score losses are acknowledged by way of reserving, adjustments in worth as a result of actions in rates of interest and credit score spreads are solely partially acknowledged. A key underlying assumption of this strategy is that the financial institution will proceed to be a going concern even after dealing with losses in worth, receiving funds due and making funds owed based mostly on contractual obligations.

Nevertheless, many financial institution belongings and liabilities don’t have binding contractual fee dates, offering financial institution clients with the choice to prepay (within the case of loans) or withdraw funds on demand (within the case of deposits). When a financial institution’s solvency is in query, depositors have an incentive to run on the establishment in an try and keep away from losses. These incentives are documented in seminal educational work by Diamond and Dybvig (1983). Therefore, solvency measures based mostly on accounting requirements will not be capable of quantify the interactions between financial institution solvency and liquidity that may threaten banks.

To handle these shortcomings, we develop another measure of financial institution solvency based mostly on estimates of the current values of belongings, liabilities, and working bills. This measure, Financial Capital (EC), incorporates adjustments in financial institution worth as a result of actions in rates of interest and credit score spreads in addition to the adjustments in worth from credit score losses acknowledged in conventional solvency measures. Importantly, EC additionally incorporates assumptions in regards to the timing of funds and the steadiness of deposits. Particularly, we’re capable of think about circumstances the place uninsured deposits have to be changed with market-rate financing and underneath potential stress shocks to rates of interest and credit score spreads.

Conceptually, EC is carefully associated to the Financial Worth of Fairness (EVE), a measure that has lengthy been used to evaluate banks’ rate of interest threat exposures. Historically, EVE-based measures have been used to evaluate adjustments in financial worth (∆EVE) ensuing from potential rate of interest actions, typically scaled by an accounting-based measure of financial institution capital. This sensitivity is meant to seize capital in danger as a result of rate of interest actions. In distinction, our implementation of EC focuses on the degree of financial capital. On this sense, EC is similar to different solvency measures similar to regulatory capital and TCE. By evaluating the extent of EC to its sensitivity to rates of interest, market costs, and depositor conduct, we will quantify banks’ solvency in response to market circumstances and funding shocks.

Calculating Financial Capital

We calculate EC utilizing publicly accessible regulatory knowledge for U.S. business banks—the Name Studies. These stories include detailed quarterly stability sheet and earnings assertion info and, important for our functions, details about the remaining maturity of every financial institution’s mortgage portfolio, time deposits, and long-term debt. The Name Studies additionally include bank-reported estimates of the honest market worth of securities and buying and selling account belongings and liabilities, which we incorporate straight into our measure of EC. Utilizing the knowledge within the Name Studies, we will estimate the current worth of loans, demand and time deposits, and different liabilities. As detailed in our paper, our estimates incorporate bank-specific, time-varying components such because the relative riskiness of the mortgage portfolio and the value sensitivity of demand deposits to rates of interest (“deposit beta”). We additionally generate bank-specific, time-varying estimates of the minimal working bills needed for every financial institution to understand the worth of its belongings and to provide deposit-related companies. EC equals our estimates of the current worth of belongings minus the current worth of liabilities minus the current worth of those minimally needed working bills.

The Name Report knowledge allow us to calculate EC again to 1997, a interval that spans a number of enterprise and rate of interest cycles, in addition to two intervals of serious banking business stress: the 2007-09 International Monetary Disaster (GFC) and the 2023 episode of banking business turmoil. This lengthy historical past offers wealthy context for assessing the outcomes we produce and for analyzing how the banking business’s solvency has developed over time.

Banking Business Solvency Over Time

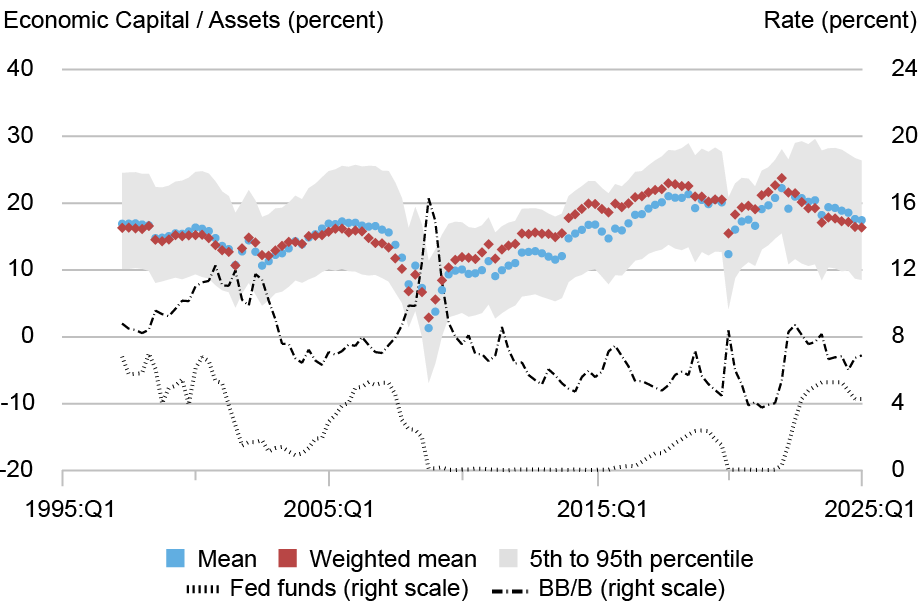

The chart beneath presents our baseline measure of EC assuming that banks retain their uninsured demand deposits. This can be a benign situation in that financial worth is calculated assuming that banks don’t incur funding stress. The chart depicts EC scaled by ebook belongings—an EC leverage ratio—for all U.S. business banks between 1997:Q2 and 2025:Q1. The blue diamonds are the unweighted common throughout all banks, the pink diamonds are the common weighted by financial institution asset dimension, and the grey shading represents the Fifth-Ninety fifth percentile estimates throughout all banks.

On common, EC has diverse between 10 and 25 p.c of belongings for many of the pattern interval. There was a pronounced dip through the GFC, when banks skilled giant credit score losses and credit score spreads (the black dashed line) widened considerably. Throughout this era, a major share of banks had unfavorable financial capital. That decline is in step with issues that motivated coverage interventions to stabilize the banking sector although typical solvency measures confirmed a lot much less deterioration.

EC has since risen above pre-GFC ranges, averaging 20 p.c or extra of belongings for the reason that mid-2010s. Bigger banks usually had greater ranges of EC than smaller banks throughout this era (the weighted common exceeds the unweighted common), implying that these banks elevated their capital within the wake of the monetary disaster.

Financial Capital (EC) Over Time

Notes: The chart exhibits the distribution of financial capital scaled by belongings from 1997:Q2 to 2025:Q1 for all business banks with belongings exceeding $50 million, excluding belief banks. The blue diamonds are common values, the pink diamonds are asset-weighted averages, and the gray shading depicts the Fifth to Ninety fifth percentile vary. The dashed line is the common yield on B- and BB-rated company bonds.

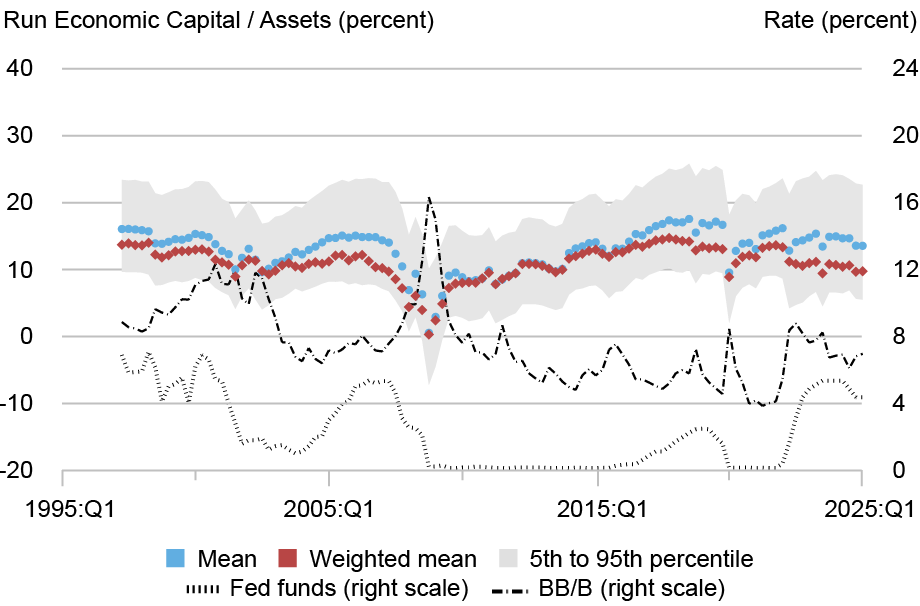

The outcomes for our baseline EC measure thus current a comparatively encouraging perspective on banking business solvency. Nevertheless, as a result of baseline EC is calculated assuming secure funding, it doesn’t incorporate funding liquidity stress. The subsequent chart presents estimates of financial capital underneath a “run situation” (R-EC), the place we assume that uninsured deposits have to be changed with market-rate funding which is dearer than deposits.

Stressing funding prices raises the current worth of liabilities by bringing the timing of deposit funds ahead in time and assuming they’re changed with dearer funding sources. The result’s that R-EC is lower than EC. Whereas R-EC will increase after the sharp decline through the GFC, the post-GFC degree of R-EC isn’t materially greater than the extent prevailing earlier than the monetary disaster. As well as, smaller banks are likely to have greater ranges of R-EC than bigger banks (the unweighted common exceeds the weighted common) as a result of giant banks’ higher reliance on uninsured deposits, suggesting that the everyday giant financial institution has greater threat underneath a run than smaller establishments. Thus, based mostly on our measure of harassed financial capital, post-crisis adjustments in prudential regulation geared toward bigger banks don’t seem to have resulted in materially decrease solvency threat for these corporations, both over time or relative to smaller banks.

Run Financial Capital (R-EC) Over Time

Notes: The chart exhibits run financial capital scaled by belongings from 1997:Q2 to 2025:Q1 for all business banks with belongings exceeding $50 million, excluding belief banks. The blue diamonds are common values, the pink diamonds are asset-weighted averages, and the gray shading depicts the Fifth to Ninety fifth percentile vary. The dashed line is the common yield on B- and BB-rated company bonds.

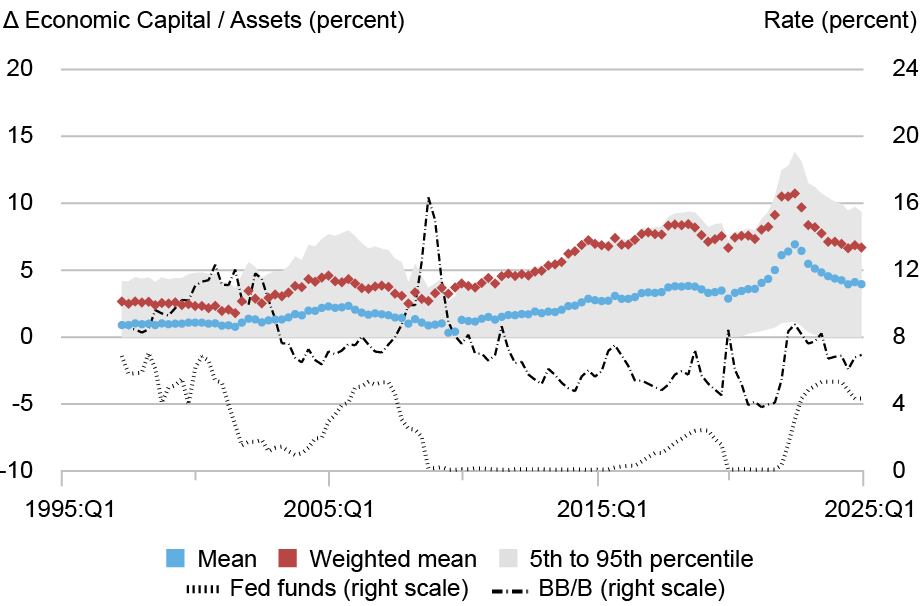

The subsequent chart, which plots the distinction between EC and R-EC, presents a further perspective on evolving dangers to banking business solvency. This distinction is a measure of the extent of deposit funding threat, because it captures the change in financial capital ensuing from a run on uninsured deposits. The banking business’s publicity to this threat has risen over time, particularly for bigger banks. The weighted common, unweighted common and cross-bank vary have all elevated steadily for the reason that GFC, reflecting elevated reliance on uninsured deposits in banks’ funding buildings.

Deposit Funding Threat

Notes: The chart exhibits the distinction between financial capital and run financial capital scaled by belongings from 1997:Q2 to 2025:Q1 for all business banks with belongings exceeding $50 million, excluding belief banks. The blue diamonds are common values, the pink diamonds are asset-weighted averages, and the gray shading depicts the Fifth to Ninety fifth percentile vary. The dashed line is the common yield on B- and BB-rated company bonds.

Summing Up

On this put up, we current new measures of financial institution solvency that incorporate adjustments in financial worth stemming from actions in rates of interest and credit score spreads underneath a spread of assumptions about depositor conduct. Whereas accounting and regulatory capital ratios counsel that the banking business is best capitalized relative to earlier than the GFC, financial capital suggests a extra nuanced story. After we assume that deposit funding is secure, it seems the banking business has improved its solvency for the reason that early 2000s. Nevertheless, after we assume deposit funding is harassed, we discover that financial capital has not materially modified relative to pre-GFC. This displays the banking business’s rising reliance on uninsured deposits as a supply of funding, significantly amongst bigger banks. In a future put up, we’ll look at whether or not our financial capital measures do a greater job of figuring out failing banks than different solvency measures.

Beverly Hirtle is a monetary analysis advisor in Monetary Intermediation Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Matthew Plosser is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Methods to cite this put up:

Beverly Hirtle and Matthew Plosser , “Financial Capital: A New Measure of Financial institution Solvency ,” Federal Reserve Financial institution of New York Liberty Road Economics, September 3, 2025, https://libertystreeteconomics.newyorkfed.org/2025/09/economic-capital-a-new-measure-of-bank-solvency/

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).