Financial institution failures and misery may be expensive to the financial system, inflicting losses to collectors and lowering the circulation of credit score and different monetary intermediation companies. Thus, there may be important worth in having the ability to determine “in danger” banks in a well timed and correct means. In a earlier publish, we introduced a brand new solvency metric, Financial Capital, and confirmed how solvency dangers within the U.S. banking trade have advanced over time in accordance with this measure. On this publish, we proceed to attract on our latest Employees Report to current evaluation exhibiting that Financial Capital identifies failing banks earlier and extra precisely than extra standard solvency measures.

An Overview of Financial Capital

As an alternative choice to extra conventional measures of financial institution solvency similar to regulatory capital and tangible frequent fairness (TCE), we suggest and develop a measure of financial capital (EC). EC is calculated utilizing estimates of the current worth of financial institution belongings, liabilities, and vital working expense. EC embeds adjustments within the worth of financial institution belongings and liabilities as a consequence of adjustments in rates of interest and credit score spreads over time, in distinction to extra conventional solvency measures based mostly on accounting rules, which don’t constantly acknowledge adjustments in worth earlier than contractual maturity. We calculate EC utilizing publicly obtainable regulatory knowledge for practically all U.S. industrial banks over an extended historic interval from 1997 to the start of 2025.

As mentioned in our prior publish, EC has a number of conceptual and computational benefits relative to measures based mostly on accounting rules. Of explicit curiosity, we will calculate R-EC, or the worth of EC underneath the idea that uninsured depositors will run on the financial institution. This measure offers perception into whether or not banks would proceed to be solvent in such circumstances.

Higher Identification of Failing Banks?

Whereas EC has sure conceptual benefits, does it actually do a greater job of figuring out failing banks earlier or extra precisely than accounting-based solvency measures? To handle this query, we take into account failures throughout the March 2023 interval, when sharp will increase in rates of interest decreased the worth of financial institution belongings, resulting in runs and the failure of 4 massive banks. We study all failing banks between 1997 and 2025, a pattern that’s dominated by credit-related failures throughout the 2007-2009 International Monetary Disaster (GFC).

Take a look at Case: March 2023 Banking Stress Episode

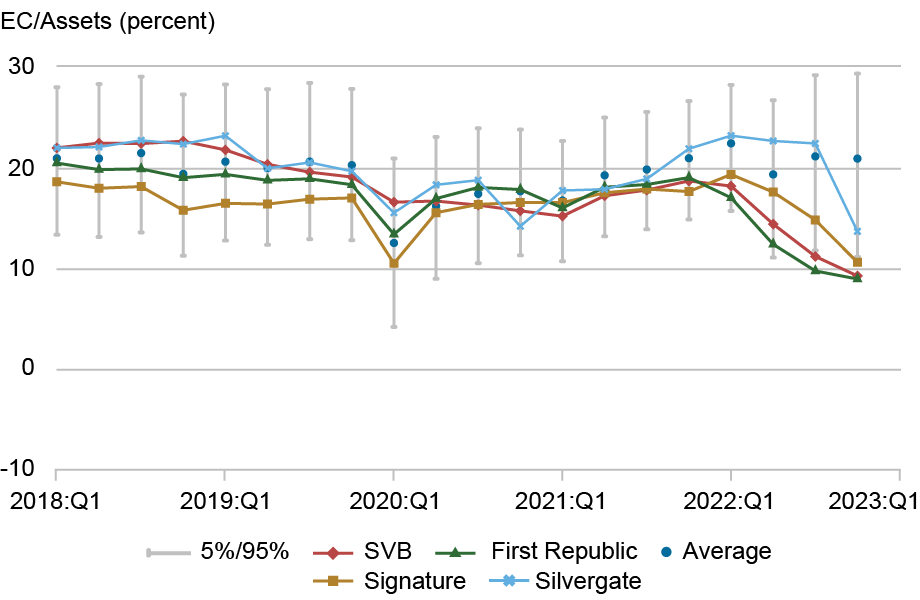

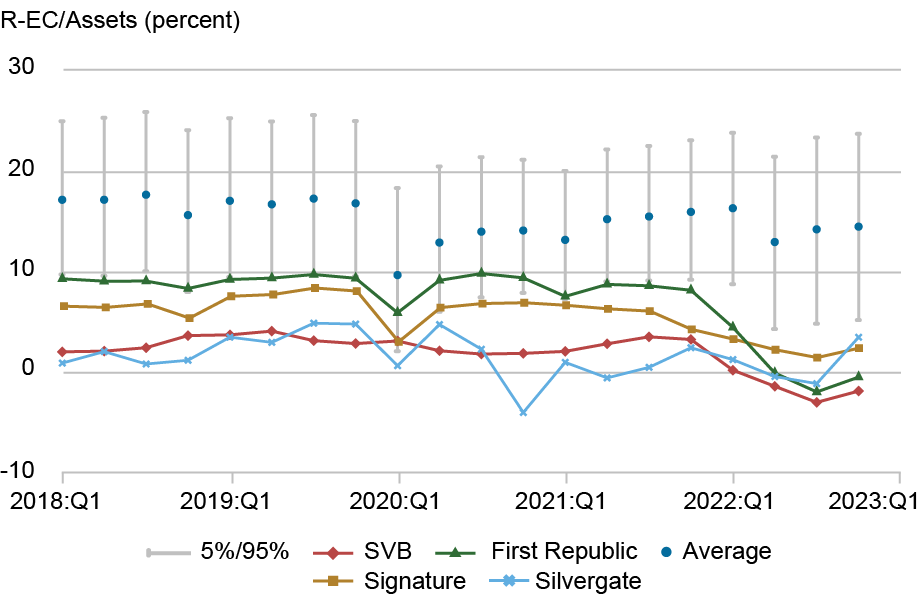

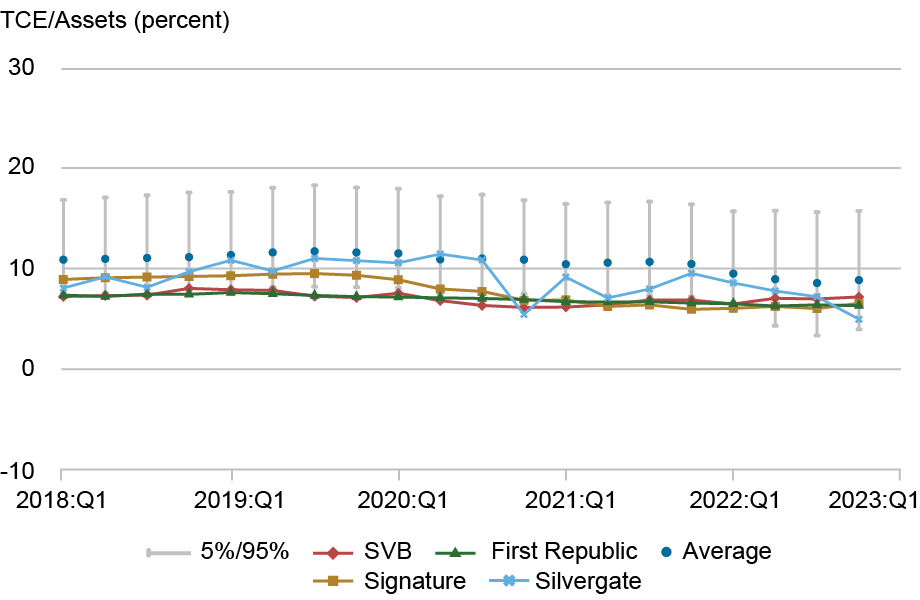

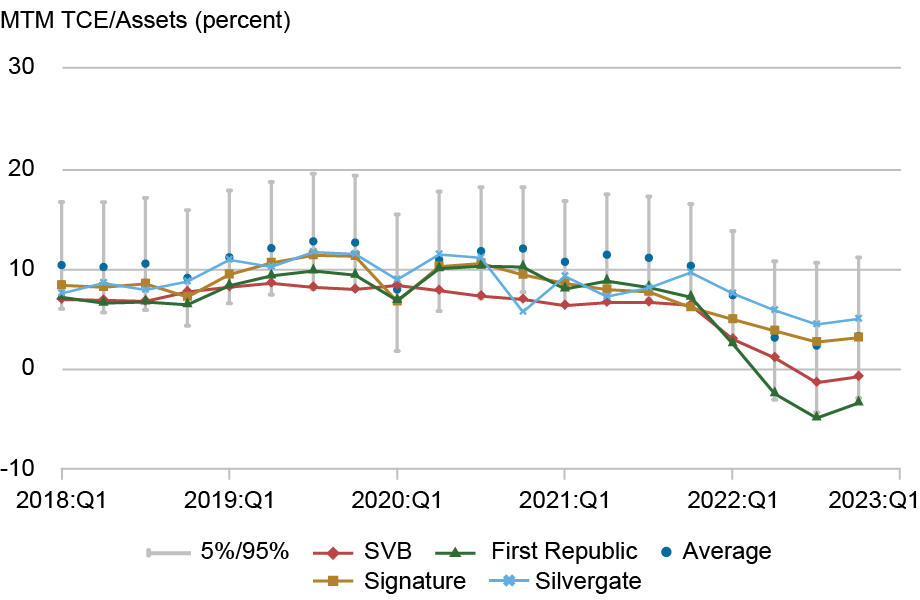

The chart under tracks 4 solvency measures within the 5 years earlier than March 2023. The 4 measures are our baseline EC measure, R-EC, TCE, and TCE adjusted for estimated losses on loans and securities (MTM TCE). Every measure is scaled by complete financial institution belongings to create a leverage ratio-type metric. The chart reveals the trail of every measure for the 4 banks that failed throughout this episode—Silicon Valley Financial institution (SVB), First Republic, Silvergate, and Signature Financial institution—together with the fifth to ninety fifth percentile vary of every measure for all banks in our pattern (“the trade”).

As the highest left panel reveals, whereas the failing banks have low EC ratios, they weren’t stark outliers with respect to the general distribution of banks till rates of interest started to rise in 2022. In distinction, R-EC ratios for these banks are notably low—generally under fifth percentile values—way back to 5 years earlier than the trade turned harassed in 2023. The truth is, the R-EC ratios for SVB and First Republic had been damaging by mid-2022.

Total, R-EC signaled a excessive threat of insolvency at these banks underneath a run state of affairs nicely forward of precise occasions. In distinction, neither of the accounting-based TCE measures offered as clear a sign. Whereas TCE ratios for the failing banks had been under trade averages, they had been throughout the fifth–ninety fifth percentile vary for your complete interval. The truth is, MTM TCE ratios for these companies really rose within the distribution—for Silvergate and Signature Financial institution, to ranges above the trade common—over the course of 2022. Whereas the extent of MTM TCE ratios for these companies fell in absolute phrases, they fell by lower than the trade common, illustrating the shortcomings of marking just one aspect of the steadiness sheet to market.

Failed-Financial institution Solvency Measures

EC

R-EC

TCE

MTM TCE

Sources: Name Experiences; authors’ calculations.

Notes: The chart reveals 4 solvency measures from 2018:Q1 to 2022:This fall for the 4 banks that failed or had been liquidated within the March 2023 interval of banking trade stress. The solvency measures are financial capital (EC), run financial capital (R-EC), tangible frequent fairness (TCE), and mark-to-market TCE (MTM TCE). The 4 banks are Silicon Valley Financial institution (SVB, in purple), First Republic (in inexperienced), Signature (in orange), and Silvergate (in blue). The gray bars are the fifth to ninety fifth percentile vary for all industrial banks with belongings higher than $50 million, excluding belief banks.

Is It Simply Curiosity Charge Danger?

Whereas the evaluation to this point means that R-EC did a greater job of anticipating which banks would fail in 2023, this discovering might mirror the traits of that specific episode slightly than a broader functionality to precisely determine failing banks. To handle this concern, we take into account all banks that failed at any time throughout our pattern interval, based mostly on data from the FDIC. The ensuing pattern of 465 failed banks is dominated by failures throughout the GFC, as roughly two-thirds of the failures occurred from 2008 to 2010, largely reflecting credit score losses—distinct from the interest-rate-driven market worth losses that spurred the 2023 episode.

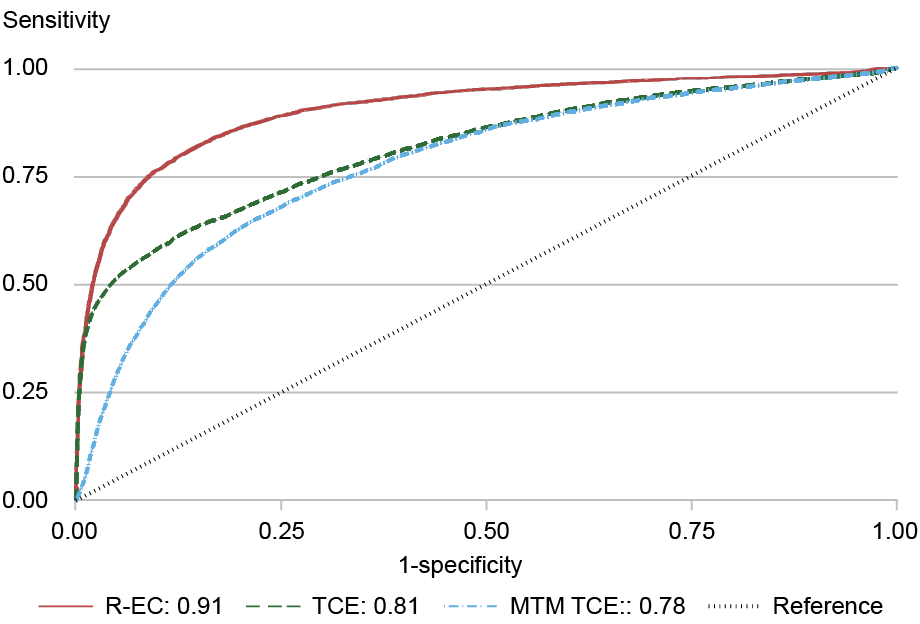

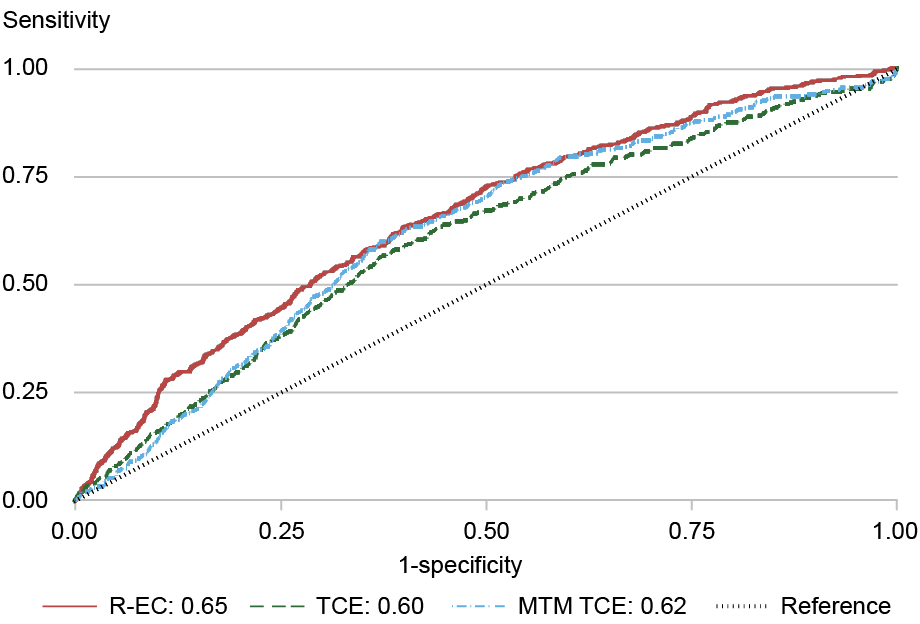

To discover how nicely the varied solvency measures predict the broader set of financial institution failures, we estimate easy logit fashions, utilizing a zero-one indicator of financial institution failure and values of R-EC, TCE, and MTM TCE, in flip, because the explanatory variable. (We don’t report outcomes for EC as they’re very near these for R-EC.) We estimate these fashions utilizing solvency measures eight and twelve quarters previous to failure and use the ensuing coefficients to assemble “Receiver Working Curves” (ROCs) exhibiting the tradeoff between appropriately figuring out a failing financial institution (on the y-axis) and incorrectly figuring out a non-failing financial institution as failing (on the x-axis). A perfect measure would appropriately determine a excessive portion of failing banks however incorrectly determine solely a small portion of non-failing banks, so curves which might be sharply sloped and nearer to the y-axis (with extra space underneath the curve) point out higher efficiency of the metric in optimizing this tradeoff.

The chart under reveals the ROCs for the three solvency metrics eight and twelve quarters earlier than failure. At each horizons, R-EC is extra correct than the choice solvency metrics, with variations on the eight-quarter horizon being notably notable. In all instances, outcomes for R-EC (the purple strains) are steeper and nearer to the y-axis than outcomes for TCE and MTM TCE, which carry out equally to 1 one other.

Receiver Working Curves for Solvency Measures

8-quarter

12-quarter

Supply: Authors’ calculations.

Notes: The chart reveals the receiver working curves (ROCs) distinguishing banks that fail (on the y-axis) from banks that don’t fail (x-axis) based mostly on logit regressions utilizing three solvency measures: run financial capital (R-EC), tangible frequent fairness (TCE), and mark-to-market TCE (MTM TCE). The panels present the ROCs 8 quarters and 12 quarters earlier than failure.

Summing Up

On this publish, we current a variety of outcomes exhibiting that our measure of Financial Capital is a extra well timed and correct indicator of financial institution failure than extra standard accounting-based measures of financial institution solvency. Accounting-based measures are based on the idea that the financial institution will proceed as a going concern and thus that the contractual timing of funds on belongings and liabilities will prevail. Conceptually, this assumption doesn’t seize circumstances by which depositors select to withdraw their funds and thus is unlikely to offer robust indicators about solvency underneath such circumstances. Financial Capital, in distinction, may be calculated underneath a financial institution run state of affairs for instance exactly this type of solvency threat. Our evaluation helps the concept this issues in apply by precisely figuring out failing banks, indicating that Financial Capital might be a helpful complement to present solvency metrics in monitoring each the well being of particular person banks and the dangers going through the banking system.

Beverly Hirtle is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

On the time this publish was written, Matthew C. Plosser was a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Methods to cite this publish:

Beverly Hirtle and Matthew C. Plosser, “Financial Capital: A Higher Measure of Financial institution Failure?,” Federal Reserve Financial institution of New York Liberty Road Economics, November 6, 2025, https://doi.org/10.59576/lse.20251106

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).