Inflation doesn’t all the time reply to value and demand pressures in the identical manner. When shocks are small, the mapping from prices to costs is roughly proportional—double the shock, double the inflation response. However when the economic system is hit by massive shocks, this proportionality breaks down. Because the current surge and subsequent decline of world inflation confirmed, worth progress can speed up—or decelerate—by greater than one-for-one relative to the scale of the disturbance. Economists confer with this sample as nonlinear inflation dynamics. On this publish, I focus on what these nonlinearities imply, how they relate to the slope of the Phillips curve mentioned in a companion publish, and the way firm-level knowledge may also help us perceive the mechanisms behind them.

Proof of Nonlinearities within the Information

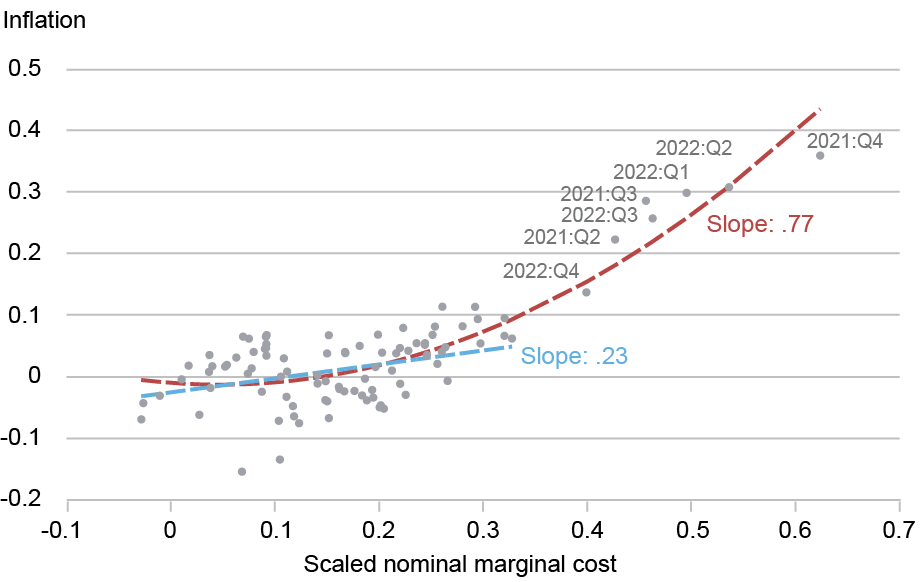

The chart beneath illustrates nonlinear inflation dynamics taken from a current working paper. It plots a measure of actual value modifications for the Belgian manufacturing sector towards producer worth inflation (PPI) over the interval 1999–2023.

The Nonlinear Relation Between Inflation Value Shocks and Inflation

Notes: Every dot represents the joint realization of year-over-year change in a production-cost index (x-axis) towards year-over-year PPI inflation (y-axis) for Belgian manufacturing in the identical quarter. The information cowl the interval 2000:Q1 via 2023:This autumn.

For small and medium-sized value shocks, inflation rises roughly one-for-one with prices: the dots align alongside a straight line. When the economic system is underneath stress, nevertheless, this proportionality breaks down. As soon as value shocks exceed a threshold—round a 20 p.c annual enhance in our knowledge—the slope steepens sharply. Double the scale of the shock and inflation rises by far more than twofold. That’s, inflation turns into extra delicate to shocks when disturbances are sufficiently massive. This sample is precisely what we observe lately, when the vitality shocks and supply-chain disruptions related to the COVID-19 pandemic and the struggle in Ukraine drove exceptionally massive will increase in producers’ prices.

The State-Dependent Nature of Pricing

Nonlinear inflation dynamics replicate the microeconomics of corporations’ pricing selections—and, specifically, the state-dependent manner corporations reply to shocks. Merely put, corporations don’t react uniformly: when shocks are small, many wait; when shocks are massive, extra corporations modify, and by bigger quantities.

To see the instinct, contemplate a world the place corporations can modify costs solely at random and with a set chance—like in a lottery. On this world, the corporations that reprice are usually not essentially these dealing with the biggest shocks (these whose costs deviate most from their optimum degree). But once they do reprice, they replace their costs to replicate present financial situations. These concepts underlie the Calvo mannequin, the workhorse mannequin utilized in tutorial and coverage evaluation. On this framework, the typical frequency of worth modifications doesn’t range with financial situations, implying that inflation scales linearly with the scale of the shock (a linear Phillips curve). Strict as they might appear, the assumptions behind the Calvo mannequin—notably the mounted chance of worth adjustment—are remarkably in step with the information in regular occasions.

Issues look completely different when shocks are massive. If adjusting costs is expensive—as a result of, for instance, it includes updating menus or dangers alienating prospects—corporations reprice solely when the advantages outweigh these prices, a lot as a restaurant rewrites its menu solely when costs are far outdated. When pressures are modest, few corporations discover it worthwhile; when shocks surge, many do. These shifts present up clearly within the knowledge: massive jumps within the common frequency of worth modifications occurred, extra lately, throughout the current pandemic inflation surge.

Such spikes are inconsistent with the Calvo mannequin, however they’re precisely what state-dependent pricing fashions—similar to menu-cost fashions or fashions with info frictions—predict. These fashions seize the concept that when the economic system is hit by massive shocks, the whole price-setting course of accelerates.

Three Details About Pricing

Utilizing detailed administrative knowledge on 1000’s of Belgian manufacturing corporations, we assemble an empirical measure of every agency’s worth hole—the proportion distinction (in proportion phrases) between the value it at the moment costs and the value it could set if it may modify freely (its “desired worth”). The bigger the hole—whether or not constructive or destructive—the higher the modifications in prices or aggressive pressures the agency faces, and the additional its present worth drifts from the specified one. We thus present a pure option to research how usually and by how a lot corporations modify in response to shocks of various sizes.

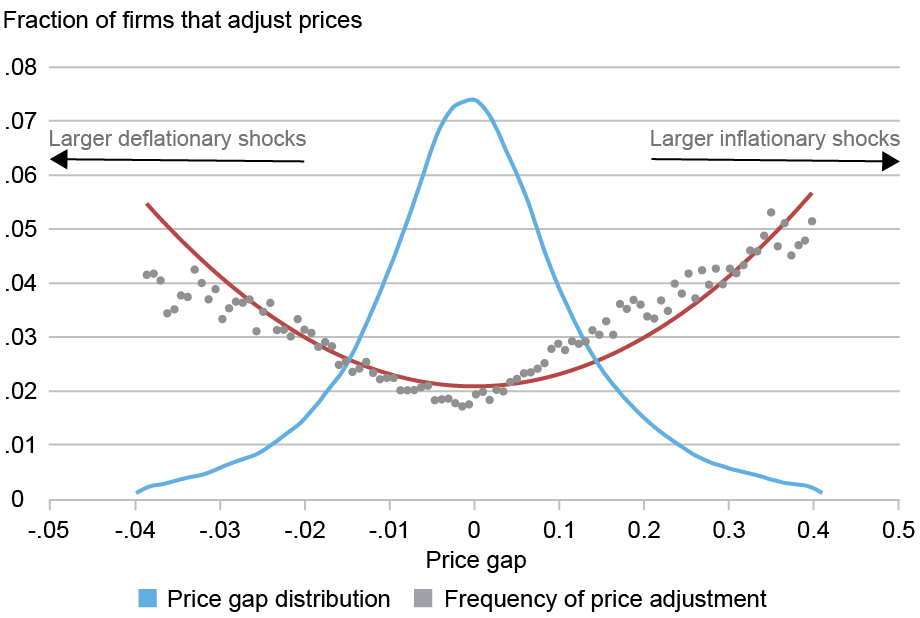

Reality 1: Companies modify extra ceaselessly when their costs drift removed from optimum

The chart beneath exhibits the connection between corporations’ worth gaps and the frequency of worth adjustment. The blue line represents the chance density operate of worth gaps and the pink line the fraction of corporations that modify their costs (y-axis) at every level of the value hole distribution. Companies within the tails—these with costs far above or beneath their desired worth degree—change costs far more usually. The connection is U-shaped: the additional a agency’s worth is from its goal, the extra possible it’s to regulate. That is precisely what state-dependent pricing fashions predict. Against this, within the Calvo mannequin the chance of adjustment is unrelated to the value hole—its predicted curve could be flat.

The Likelihood of Value Adjustment Rises with the Measurement of the Value Hole

Notes: The blue line represents the chance density operate of the distribution of worth gaps; the pink line exhibits the measured frequency of worth adjustment alongside the value hole distribution.

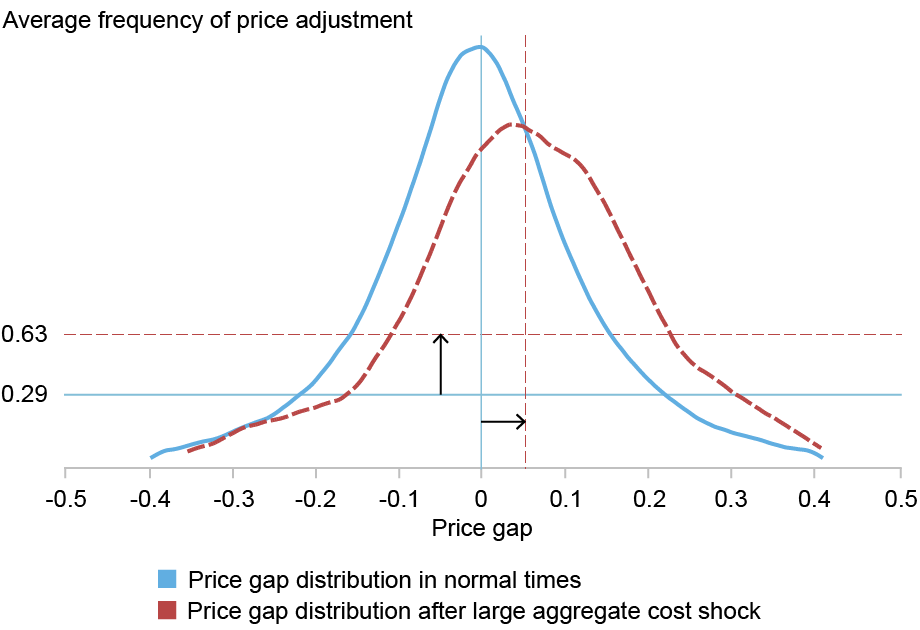

Reality 2: Massive mixture shocks shift the whole distribution of worth gaps, prompting extra frequent worth modifications

The chart beneath exhibits how mixture shocks reshape corporations’ incentives to reprice. Earlier than the pandemic, the distribution of worth gaps was centered round zero (blue line). In 2022:Q2—the quarter with the biggest soar in corporations’ manufacturing prices—the whole curve shifts rightward (pink dashed line) as producers grappled with surging vitality costs and widespread provide chain disruptions, and, as predicted by state-dependent pricing, the share of corporations altering costs almost doubled, resulting in a marked acceleration in inflation.

Massive Combination Shocks Shift the Total Distribution of Value Gaps, Prompting Extra Frequent Value Adjustments

Notes: The blue curve is the pre-pandemic (1999–2019) density of worth gaps; the pink dashed curve is the 2022:Q2 density. Vertical traces mark the typical gaps within the pre-pandemic interval and in 2022:Q2. Horizontal traces present common adjustment chances in every interval.

Reality 3: Inflation grows disproportionately bigger when massive shocks hit

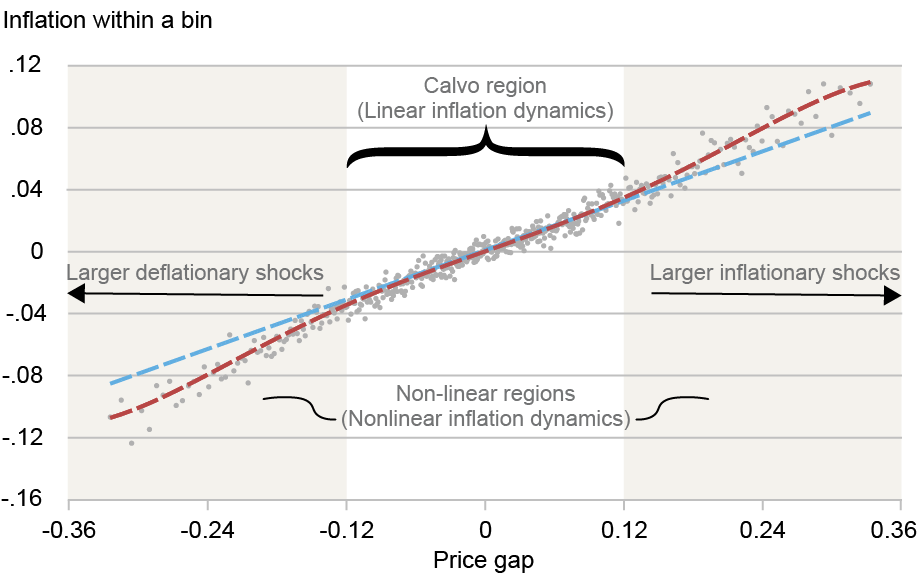

Within the chart beneath, we once more group corporations by the scale of their worth hole. Every dot represents the typical worth hole for a bunch of corporations (x-axis) plotted towards their common worth change (y-axis). The pink dashed line exhibits a nonlinear match via this cloud of factors.

Inflation Responds Nonlinearly with the Measurement of the Shocks to Companies’ Desired Costs

Notes: The blue dashed line represents a linear match of worth modifications (inflation) on worth gaps, estimated on the subsample of bins protecting corporations between the twenty fifth and seventy fifth percentiles of the value hole distribution, with the estimated slope reported in black. The pink dashed line represents the match of a third-order polynomial in worth gaps, estimated utilizing bins throughout the whole worth hole distribution.

At any level alongside this curve, its slope measures how strongly value shocks are handed via into costs—the steeper the slope, the stronger the pass-through, and the steeper the Phillips curve. This train reveals that the mapping between anticipated worth modifications and worth gaps isn’t fixed. In actual fact, we are able to establish two distinct areas.

The Calvo area. When worth gaps are small (roughly +/- 10 p.c), pricing conduct appears to be like linear: adjustment frequencies are steady, pass-through is proportional, and the elasticity of worth modifications with respect to gaps matches the typical adjustment frequency. This sample helps clarify why the Calvo mannequin works properly in low-inflation environments.

The nonlinear areas. On the tails of the value hole distribution, pricing turns into much more reactive. Companies hit by massive shocks exhibit almost double the same old pass-through as a result of vital rise within the frequency of worth adjustment. The conduct of those corporations mirrors what occurs to the broader economic system throughout main disturbances—similar to these triggered by the COVID-19 pandemic. Throughout these episodes, the economic system is pushed into areas the place the slope of the Phillips curve rises, and inflation reacts far more strongly and shortly to value pressures.

Recognizing when the economic system shifts between these regimes is essential for resolution makers who depend on well timed indicators about altering inflation situations. Accounting for these transitions is essential to understanding how inflation builds and finally unwinds.

Simone Lenzu is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The best way to cite this publish:

Simone Lenzu, “Does the Phillips Curve Steepen When Prices Surge?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, February 5, 2026, https://doi.org/10.59576/lse.20260205

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).