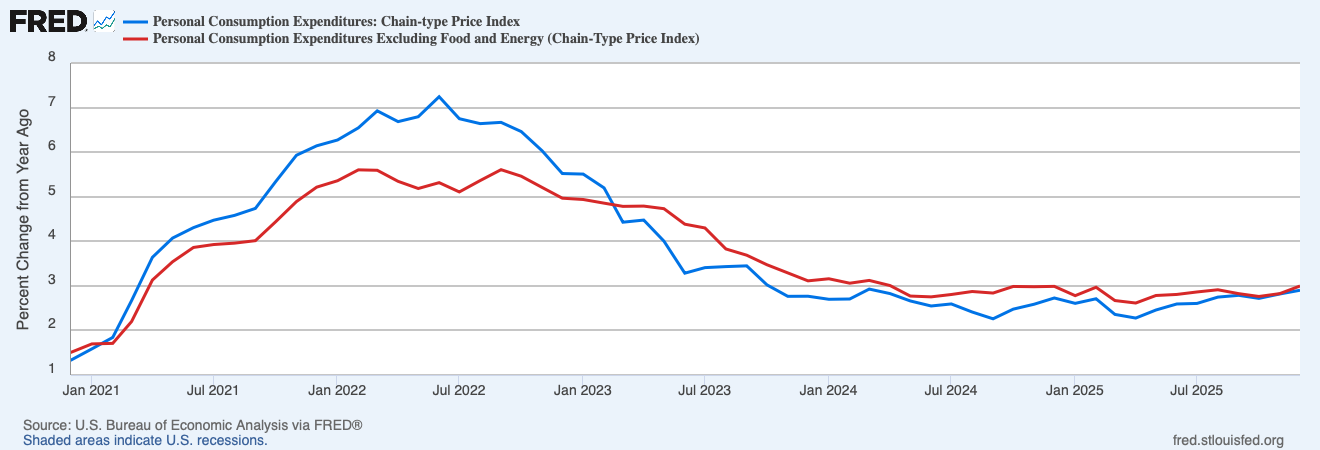

Delayed information confirms inflation remained properly above goal in December. The Private Consumption Expenditures Value Index (PCEPI), which is the Federal Reserve’s most popular measure of inflation, grew at an annualized price of 4.4 p.c within the final month of 2025. The PCEPI grew at an annualized price of three.1 p.c over the prior three months and a pair of.9 p.c over the prior 12 months.

Core inflation, which excludes risky meals and vitality costs, additionally remained elevated. Core PCEPI grew at a constantly compounding annual price of 4.3 p.c in December 2025. It grew at an annualized price of three.1 p.c over the prior three months and three.0 p.c over the prior 12 months.

The outsized value will increase have been widespread, if uneven. Items costs grew at an annualized price of 4.7 p.c in December, and have been up 1.7 p.c year-over-year. The costs of sturdy items grew at an annualized price of 6.8 p.c in December, whereas the costs of non-durable items grew 3.6 p.c. Companies costs grew 4.2 p.c in December. They grew 3.4 p.c over the prior 12 months.

Uncertainty Clouds the Coverage Outlook

Stubbornly excessive inflation readings over the again half of 2025 led the Federal Open Market Committee to pause its price cuts final month, with the federal funds price goal vary held at 3.5 to three.75 p.c. FOMC members look like divided on whether or not — and, in that case, when — to start chopping charges once more.

Again in December, the median FOMC member projected the federal funds price would finally settle round 3.0, albeit someday after 2028. However the distribution of projections supplied something however certainty. 4 FOMC members projected an extended run midpoint of the federal funds price goal vary at or above 3.5 p.c; 5 members projected a midpoint between 3.0 and three.5 p.c; 5 members projected a midpoint at 3.0 p.c; and 4 members projected a midpoint under 3.0 p.c.

The median FOMC member projected only one 25-basis-point reduce this 12 months. Right here, too, FOMC members supplied little certainty, nonetheless. Seven members projected the federal funds price would stay at or above its present vary this 12 months. 4 projected one 25-basis-point reduce; 4 projected two cuts; and three projected greater than two cuts.

Trigger for Battle

Why do the FOMC members’ assessments of the right path for rates of interest differ a lot? All of them have entry to the identical information, the identical fashions, and a military of economists. Three elements stand out: information issues, coverage shocks, and political strain.

Final 12 months’s authorities shutdown disrupted the standard circulation of knowledge, which has nonetheless not been completely restored. At present’s Private Consumption Expenditures launch is roughly one month delayed, and the Bureau of Financial Evaluation doesn’t anticipate to be again on monitor till the top of April. There are additionally issues about information high quality. When an underlying survey isn’t carried out, the results of that lacking information may linger on in methods which are tough to discern. That sows doubt, prompting FOMC members already eager to take a wait-and-see strategy to attend just a little longer.

The final 12 months has additionally been marked by vital coverage modifications. The Trump administration has ramped up immigration enforcement, decreased rules, slashed authorities employment, rolled again green-energy efforts, and overhauled the tax code. It captured and eliminated former Venezuelan President Nicolás Maduro and has despatched an armada to the Center East, with doubtlessly giant and long-lasting implications for American vitality prices. These coverage modifications have an effect on productiveness and, with it, estimates of potential output, most employment, and the longer run impartial price of curiosity. However how and to what extent? The varied contributors are so quite a few and of unsure magnitudes that it’s anybody’s guess.

Fed officers are significantly targeted on President Trump’s tariffs. On the post-meeting press convention in January, Fed Chair Jerome Powell mentioned “our financial system has pulled via fairly properly […] given the very vital modifications in commerce coverage.” That’s partly as a result of the tariffs finally imposed by the Trump administration have been a lot decrease than these initially introduced and the retaliatory tariffs imposed by different nations have been extra restricted than anticipated, he mentioned. However additionally it is as a result of “a very good a part of it hasn’t been handed via to customers but.” Powell defined how the Fed fashions the results of tariffs:

Originally, it was very a lot of a forecast; now, it’s — each, each cycle that goes by, it turns into extra knowledgeable by precise information. And we have been — we — our forecasts weren’t far off. What modified was, as I believe I mentioned earlier, what modified was what was applied was smaller than what was introduced. As well as, we didn’t see retaliation internationally, and I believe individuals did usually anticipate that as a result of we noticed that previously. And that actually mattered too. After which the opposite factor is the pass-through — didn’t know the way quick that was going to be to customers, didn’t know the way a lot exporters would take, how a lot firms within the center would take, and the way a lot the patron would take. And it seems it’s quite a lot of firms within the center — who, by the best way, are fairly strongly dedicated to passing the remainder of it via, which is without doubt one of the the reason why we have to maintain our eye on inflation and never declare victory prematurely.

As Powell’s assertion makes clear, there was rather a lot FOMC members didn’t know when tariffs have been introduced final 12 months, a few of which they nonetheless don’t know in the present day. At present’s Supreme Courtroom resolution on Trump’s use of the Worldwide Emergency Financial Powers Act additional complicates the evaluation. Resolving all that uncertainty takes time — and information.

Lastly, some FOMC members could also be involved with the perceived enhance in political strain on the Federal Reserve. President Trump has persistently referred to as for decrease rates of interest over the past 12 months. He’s believed to have pressured then-Vice Chair for Supervision Michael Barr to step down. He tried to fireside Governor Lisa Prepare dinner. He nominated then-CEA Chair Stephen Miran to fill a emptiness on the Fed, presumably to push for decrease rates of interest. And his Division of Justice opened an investigation into Chair Powell. With these occasions in thoughts, some FOMC members could also be reluctant to decrease the federal funds price goal even when they suppose a reduce is warranted by the info on the grounds that doing so would cut back the Fed’s credibility.

Implications for the March Assembly

FOMC members disagree in regards to the correct path for the federal funds price. These disagreements stem from competing views on the numerous coverage shocks realized over the past 12 months and the way finest to take care of political strain from the president. Knowledge disruptions make it harder than common to resolve these disagreements. The newest PCEPI launch illustrates the issue properly: it arrives roughly a month delayed and could also be distorted by the efforts taken to take care of lacking surveys.

Given the context, it appears probably that the FOMC will proceed to carry its federal funds price regular in March. Certainly, the CME Group places the percentages of a March price reduce at simply 4.0 p.c.