{kind=link}

Retirement planning is usually a cornerstone of a consumer’s monetary plan, with advisors estimating how a lot the consumer can safely spend in retirement. In apply, advisors usually start with the consumer’s goal retirement date, after which modify levers equivalent to withdrawal charges, asset allocation, and spending flexibility to make the plan work. However when the retirement date is handled as mounted, an essential a part of the planning downside could also be left unexamined: whether or not the timing of retirement itself helps or hurting the plan from the outset.

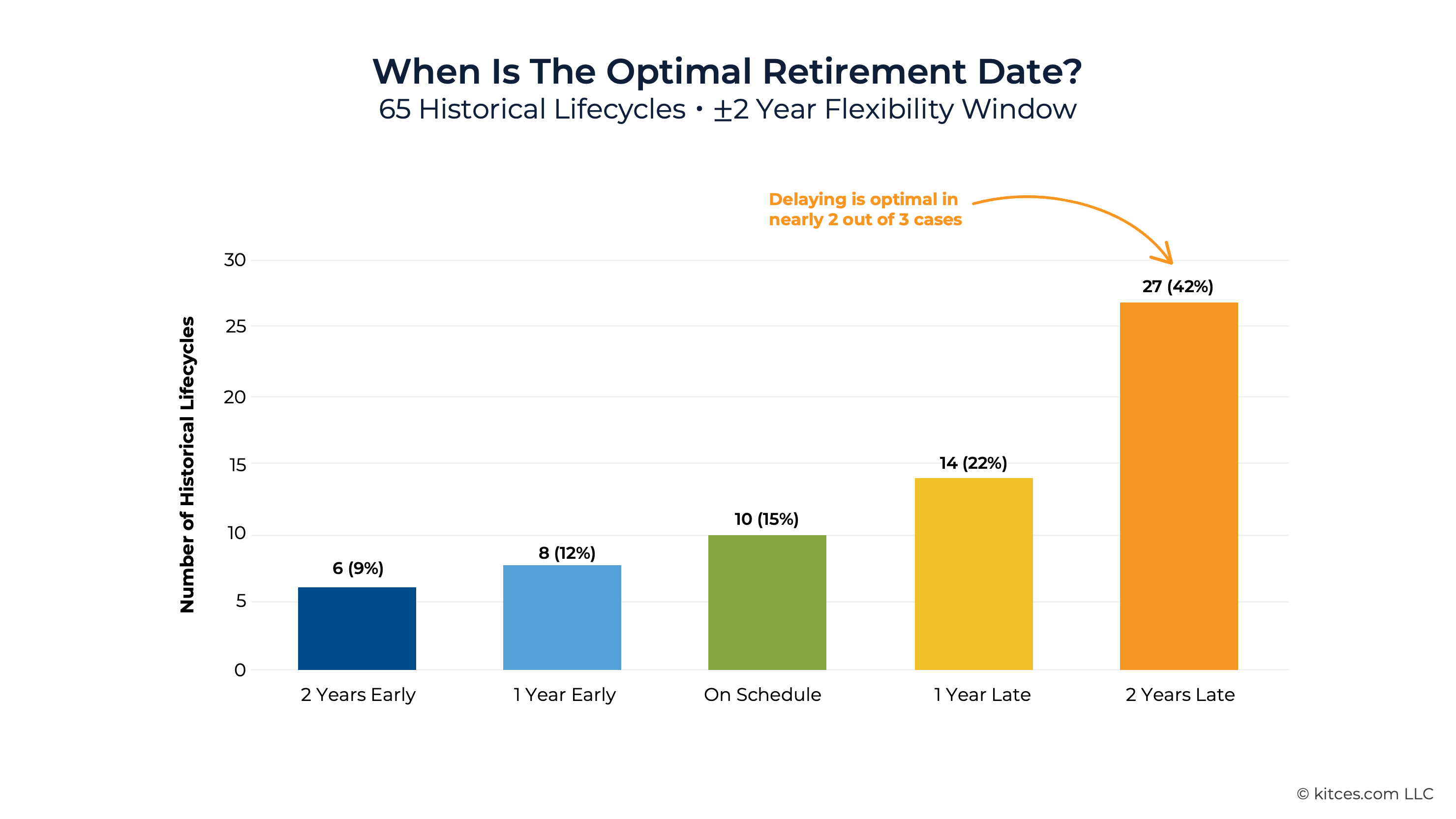

On this visitor put up, Georgios Argyris, Analysis Director at bellavia.app, explains how even a small shift in retirement timing can change the market atmosphere the retiree enters and, with it, the sustainability of the plan. The impact turns into clear when evaluating in any other case an identical retirees who start withdrawals in several environments. Throughout the historic lifecycle cohorts examined, permitting for a two-year flexibility window produced a median hole of roughly two-thirds in closing portfolio worth between the most effective and worst timing selection throughout the window. Retiring on the initially deliberate date was optimum solely about 15% of the time; typically the place a distinct selection helped, delaying retirement produced a greater end result.

This end result could be understood by separating retirement timing danger into two parts: cohort danger, which displays the general return atmosphere a retiree experiences, and pure sequence danger, which displays the order of returns inside that atmosphere. Historic evaluation means that roughly three-quarters of retirement end result variability is pushed by cohort danger, whereas solely about one-quarter is attributable to return ordering inside a cohort. This distinction issues as a result of most conventional planning instruments – together with dynamic withdrawal methods, guardrails, and allocation changes – function solely inside a given cohort, subsequently addressing solely the smaller portion of danger. Against this, adjusting the retirement date is among the few levers that may shift a consumer into a distinct cohort altogether.

This framework additionally results in a counterintuitive perception: purchasers who seem most ready for retirement – typically these with the biggest portfolios after sturdy accumulation durations – should still face elevated timing danger. Robust bull markets can inflate retirement balances whereas leaving purchasers uncovered to weaker ahead returns. Consequently, a big portfolio worth at retirement won’t, by itself, point out that the timing is favorable. Advisors can partially assess this danger utilizing valuation metrics such because the Shiller CAPE ratio, which has proven a relationship with subsequent decade-long returns and can assist determine whether or not present circumstances resemble traditionally unfavorable retirement environments.

In the end, the important thing level is that retirement timing could deserve a bigger position in retirement planning than it’s typically given. Advisors could enhance outcomes by first contemplating whether or not the retirement date itself needs to be adjusted, significantly when market circumstances seem unfavorable. When timing flexibility is restricted, lowering the preliminary withdrawal fee can present a margin of security, whereas dynamic spending methods can assist handle the remaining ordering danger. By recognizing retirement timing as a planning variable reasonably than merely a hard and fast assumption, advisors can higher place purchasers to navigate uncertainty and help the sustainability of retirement revenue over time.