As in earlier years, we offer on this put up an replace on the vulnerability of the U.S. banking system based mostly on 4 analytical fashions that seize completely different elements of this vulnerability. We use information by way of 2025:Q2 for our evaluation, and in addition talk about how the vulnerability measures have modified since our final replace one 12 months in the past.

How Do We Measure Banking System Vulnerability?

We contemplate the next measures to seize key dimensions of banking system vulnerability, based mostly both on analytical frameworks developed by New York Fed employees or tailored from tutorial analysis. The 4 measures had been initially launched in a Liberty Road Economics put up in 2018 and have been up to date yearly since then, with a revision of the methodology carried out in 2023. The evaluation makes use of publicly accessible regulatory information on financial institution holding corporations.

The 4 measures purpose to seize capital, hearth sale, liquidity, and run vulnerabilities—and the way in which during which they work together to amplify unfavorable shocks. The chart under reveals the evolution of those measures.

Capital Vulnerability Indexes

Capital hole (billions of {dollars})

Hearth-Sale Vulnerability Index

Fraction of capital in danger

Liquidity Stress Ratio

Ratio of liquid liabilities to liquid property

Run Vulnerability Index

Essential fraction of unstable funding

Supply: Authors’ calculations, based mostly on FR Y-9C stories.

Capital Vulnerability Indexes

These two indexes measure how well-capitalized the banks are projected to be after a extreme macroeconomic shock. They’re constructed utilizing the CLASS mannequin, a top-down stress-testing mannequin developed by New York Fed employees. The indexes measure the capital hole, outlined as the mixture quantity of capital wanted underneath a macroeconomic state of affairs to deliver every financial institution’s Tier 1 widespread fairness capital to not less than 10 % of its risk-weighted property.

We calculate the Capital Vulnerability Indexes underneath two macroeconomic situations: one which replicates the circumstances skilled in the course of the 2007-09 monetary disaster (“2008 redux”) and one which replicates the circumstances skilled in the course of the 2022 rise in rates of interest (“2022 redux”). Within the second state of affairs, unrealized good points and losses on securities held within the AFS (“accessible on the market”) and HTM (“held to maturity”) portfolios are totally mirrored in banks’ capital ranges. Each indexes are steady and, if something, have improved over the past 4 quarters: based mostly on the “2008 redux,” the capital hole now stands at $1.92 billion (down from $5.1 billion in 2024:Q2), whereas based mostly on the “2022 redux,” the hole is now $161.32 billion (down from $260.47 billion in 2024:Q2). Banks’ capital ratios, excessive by historic requirements, are an necessary driver of this dynamic.

The chart under paperwork the decomposition of the Capital Vulnerability Indexes into two foremost elements at any given time limit, specifically the beginning degree of capital and the capital depletion in the course of the projection interval. Notice that the beginning degree of capital, particularly as soon as unrealized good points and losses on securities are taken into consideration, has been enhancing since 2023 as each (1) the extent of precise financial institution capital has improved (gentle blue line) and (2) the unrealized losses on securities have decreased (additional pushing the crimson line up).

Decomposition of the Capital Vulnerability Index

Ratio of capital to risk-weighted property (%)

Hearth-Sale Vulnerability Index

This index, based mostly on the Journal of Finance article “Hearth-Sale Spillovers and Systemic Danger,” captures the vulnerability of banks to a hypothetical system-wide asset hearth sale. The state of affairs assumes a uniform shock to all asset values, incentivizing banks to promote property with a view to cut back their leverage. The spillover losses, ensuing from the worth impression of the asset gross sales, are calculated as a fraction of banks’ Tier 1 capital. Given the expertise of March 2023, the methodology makes use of the “honest worth” for all securities and adjusts financial institution capital for unrealized losses (or good points). This adjustment will increase leverage and subsequently fire-sale vulnerability in durations of notable unrealized losses, due, for instance, to rising rates of interest.

The Hearth-Sale Vulnerability Index is roughly degree in comparison with the earlier annual replace. The index has been on an unsteady reducing development since growing sharply beginning in 2022:Q1 and peaking in 2022:Q3 at a degree final seen in 2009 (see the primary chart on this put up). Since then, the index has retraced greater than half of its enhance and has been at a average degree by historic requirements, but it surely stays elevated in comparison with the low ranges noticed between 2015 and 2022. The chart under decomposes the index into the dimensions of the banking system (relative to the remainder of the monetary sector), its leverage, and its “connectedness” (capturing the commonality of asset liquidity, leverage, and dimension throughout banks). Each the rise within the index in 2022 and the lower since then have been pushed primarily by adjustments in leverage, measured at honest worth.

Decomposition of the Hearth-Sale Vulnerability Index

Normalized to 100 in 2006:Q1

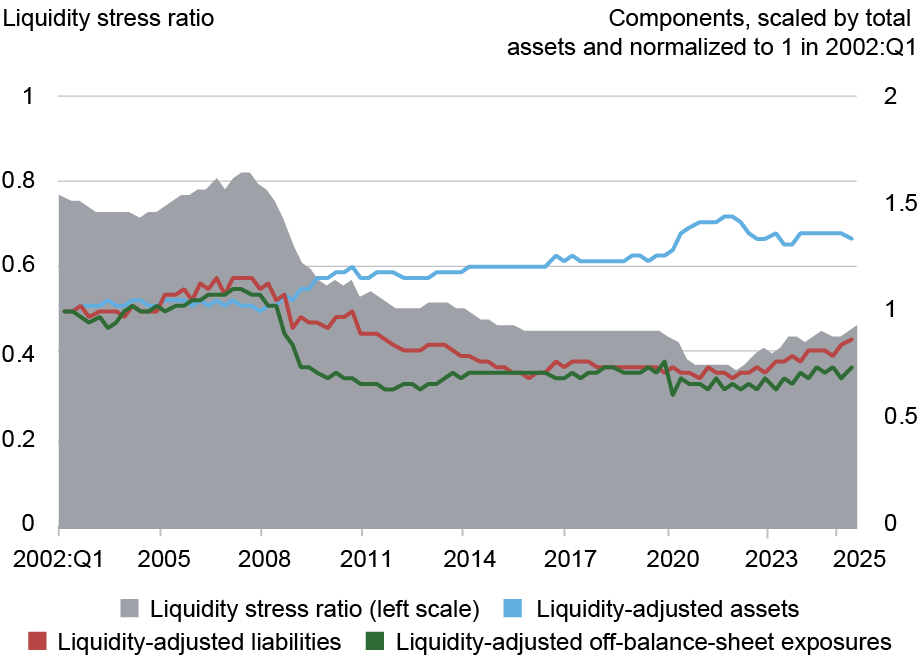

Liquidity Stress Ratio

This ratio measures the potential liquidity shortfall of banks underneath circumstances of liquidity stress as captured by the mismatch between liability-side (and off-balance-sheet) liquidity outflows and asset-side liquidity inflows. For every particular person financial institution, it’s outlined because the ratio of runnability-adjusted liabilities plus off-balance-sheet exposures to liquidity-adjusted property. The liabilities are adjusted for runnability by weighting every publicity class by its anticipated outflow fee, whereas the property are adjusted for liquidity by weighting every asset class by its anticipated market liquidity. The liquidity stress ratio grows when anticipated funding outflows enhance or property grow to be much less liquid. Following the occasions of March 2023, the methodology accounts for unrealized losses or good points on all securities through the use of the honest worth methodology, which suggests a rise within the ratio when property depreciate—due, for instance, to rising rates of interest. The mixture ratio is computed as a size-weighted common of the person banks’ liquidity stress ratio.

The primary chart on this put up reveals that the liquidity stress ratio is considerably above the extent of the earlier annual replace. The ratio has been on an growing development since 2022:Q1 and presently stands at its pre-pandemic worth. Nonetheless, it’s average by historic requirements, being roughly half of the 2007:Q3 peak however above the low ranges of 2020–21. The chart under plots the underlying elements of the liquidity stress ratio. The numerous rise within the ratio since early 2022 has been pushed by a decline in liquid property, coupled with a rise in unstable funding and off-balance-sheet exposures.

Decomposition of the Liquidity Stress Ratio

Run Vulnerability Index

This measure gauges a financial institution’s vulnerability to runs, making an allowance for each the financial institution’s liquidity and its solvency. We assume {that a} shock to property and a concurrent lack of funding forces pricey asset liquidations. Consequently, a financial institution can grow to be bancrupt as a consequence of a sufficiently dangerous asset shock, a sufficiently giant lack of funding, or each. A person financial institution’s run vulnerability is measured because the minimal fraction of unstable funding that the financial institution must retain within the stress state of affairs to stop insolvency. The mixture index is computed as a size-weighted common of the person banks’ run vulnerabilities. This system additionally makes use of the honest worth for all securities, which leads to larger values of financial institution leverage within the interval since early 2022.

The Run Vulnerability Index is at related ranges as in the course of the earlier annual replace. Since growing sharply beginning in 2022:Q1 and peaking in 2022:Q3 at a degree final seen in 2012, the index has not proven a transparent development. Run vulnerability is presently average by historic requirements however stays elevated in comparison with the low ranges between 2015 and 2022. Contemplating the underlying elements of run vulnerability (see the chart under), we see that the rise within the index since early 2022 is principally as a consequence of a rise in leverage, however the different elements (unstable funding and illiquid property) have additionally elevated over this era.

Decomposition of the Run Vulnerability Index

Normalized to 0 in 2002:Q1

Last Phrases

Our measures current a blended image of traits in banking system vulnerabilities in recent times. Whereas uniformly decrease than the excessive ranges seen within the run-up to the 2008–09 monetary disaster, among the measures have been larger in recent times than the low ranges attained between 2015 and 2020.

Matteo Crosignani is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Thomas M. Eisenbach is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Fulvia Fringuellotti is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Find out how to cite this put up:

Matteo Crosignani, Thomas Eisenbach, and Fulvia Fringuellotti, “Banking System Vulnerability: 2025 Replace,” Federal Reserve Financial institution of New York Liberty Road Economics, November 4, 2025, https://doi.org/10.59576/lse.20251104

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).