{kind=link}

On October 10, 2025, the announcement of a possible further 100 % tariff on Chinese language items drove risk-off strikes throughout equities, Treasuries, credit score spreads, and digital belongings. Digital asset costs fell sharply, buying and selling volumes surged, and liquidity vanished from key exchanges. On this put up, we present how the worth shock in digital belongings was transmitted and amplified by way of a category of devices known as artificial stablecoins—crypto belongings whose structural design turned an exterior shock right into a self-reinforcing deleveraging spiral inside the crypto ecosystem.

Artificial Stablecoins and Perpetual Futures

Artificial stablecoins differ basically from fiat-asset-backed stablecoins like USD Coin (USDC), that are backed by reserves of dollar-equivalents reminiscent of Treasury payments, Treasury-backed reverse repurchase agreements, and financial institution deposits. As an alternative, artificial stablecoins like Ethena (USDe) goal their greenback peg by way of monetary engineering: they mix a protracted place in cryptocurrency (usually ether staked in a staking pool like Lido) with an offsetting brief place in perpetual futures contracts. Lido swimming pools collectively ether deposits, earns yield for collaborating in Ethereum’s proof of stake protocol, and returns depositors a liquid token known as staked ether (stETH) that can then be used once more as collateral in different DeFi protocols reminiscent of Ethena. This construction creates a “artificial” greenback place with out requiring precise greenback reserves.

Perpetual futures are the spine of artificial stablecoins. They’re contracts with out an expiry date, designed to trace the spot value of an asset by way of a recurring funding price (that’s, a foundation fee between lengthy and brief positions that retains costs aligned). When the perpetual future trades above spot, traders with lengthy futures positions pay these with brief futures positions; when it trades under spot, shorts pay longs. These funding flows create a bridge between leveraged merchants and arbitrageurs, making certain that derivatives keep near their underlying belongings. The mechanics of this commerce are just like these of the cash-futures foundation commerce within the Treasury relative worth house.

Artificial stablecoins depend on this construction to take care of their peg. Every minted coin represents a matched place: lengthy staked ether (ETH) and brief perpetual futures. The Ethena DeFi protocol earns the sum of staking rewards and any funding price revenue from the brief place. When funding charges stay optimistic and steady, this design delivers engaging returns with minimal value publicity, drawing new capital into the system. The important thing fragility, nevertheless, is that the hedge will depend on steady liquidity in derivatives markets and a persistently optimistic funding price. If funding turns detrimental or margin prices rise, the artificial greenback turns into costly to take care of and redemptions start.

Ethena’s Minting and Unwinding Mechanism

The stablecoin USDe, which is issued by Ethena, illustrates this mechanism in observe. New cash are minted when traders deposit ether or staked ether as collateral. Ethena’s programmatic good contracts open a brief place in ether perpetual futures, neutralizing value threat and locking in a yield given by the sum of the ether staking yield and the futures place’s funding price. So long as that sum stays optimistic, issuance grows quickly. Between early 2024 and mid‑2025, Ethena’s complete provide expanded to just about $15 billion, reflecting sturdy inflows of collateral and speculative demand for the excessive yields. By August 2025, Ethena had develop into the third-largest stablecoin by market capitalization (albeit a distant third after Tether’s USDT and Circle’s USDC).

When market circumstances change, this course of reverses. Falling funding charges in ether perpetual futures markets cut back revenue from brief positions, whereas increased margin prices compress the yield benefit, making the positions unattractive. Even worse, funding charges may flip detrimental, with brief futures holders having to pay lengthy futures holders. Traders redeem USDe for the underlying ether, forcing Ethena’s good contract to shut its brief futures place and launch collateral. This closing sequence requires shopping for again futures and promoting ether, placing strain on each derivatives and spot markets. The result’s a self-reinforcing unwind: decrease costs cut back collateral values, which in flip set off extra redemptions.

A Easy Instance

Think about an investor who needs to buy $100,000 price of artificial stablecoins. They deposit $100,000 price of staked ether as collateral, which earns a 3.5 % annual staking yield. The protocol concurrently opens a $100,000 brief place in ether perpetual futures. If the funding price is optimistic—say, 10 % annualized—shorts obtain funds from longs, producing further yield. The investor’s complete return can be roughly 13.5 % (3.5 % staking + 10 % funding), whereas sustaining dollar-denominated publicity because the lengthy ether and brief futures positions offset one another.

But when the funding price turns detrimental to –5 % annualized, the dynamics reverse. The investor should pay 5 % yearly to take care of the brief place whereas incomes simply 3.5 % from staking—a internet lack of 1.5 %. This leads traders to shut positions by shopping for again futures—and promoting spot ether. As traders redeem en masse, these pressured transactions amplify the unique decline in charges.

Deleveraging and the October 10 Occasion

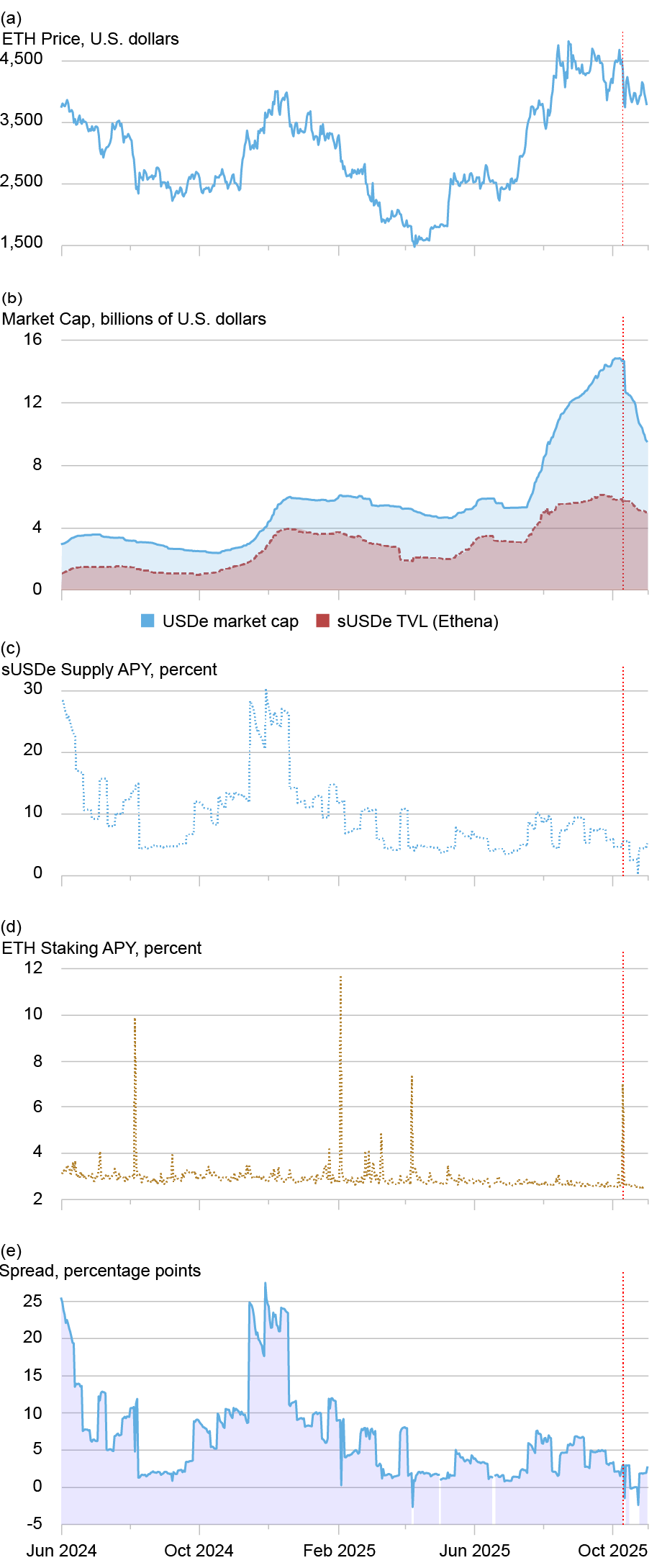

The dynamics of this deleveraging are seen within the chart under, which tracks the quantity, yields, and spreads of USDe and its yield-paying analogue, staked USDe (sUSDe), between June 2024 and October 2025. The higher panels present the sharp enlargement of USDe provide by way of the passage of the GENIUS Act in mid-2025, adopted by a sudden contraction starting in October. The decrease panels plot the USDe yield and the ether staking yield. On October 10, the unfold between them turned detrimental, which means the price of sustaining the brief futures exceeded the return from staking. As soon as the yield turned detrimental, the inducement to carry USDe vanished, and traders started to unwind their positions.

USDe and Staked USDe Dynamics: Scale, Yields, and Spreads (June 2024 – October 2025)

Notes: Panel (a) exhibits the ether value; panel (b) the full market capitalization of Ethena (USDe) and the full staked worth of Staked Ethena (sUSDe); panel (c) the sUSDe annual share yield (APY); panel (d) the ether staking yield; and panel (e) the yield unfold between sUSDe and ETH staking. The vertical purple line marks October 10, 2025, the date of the U.S. announcement of potential further tariffs on Chinese language items.

The decline in market capitalization in panel b displays this unwinding: collateral was launched, futures brief positions have been closed, and liquidity drained from each markets. The system that had grown on the promise of a excessive carry grew to become a pressured vendor, deepening the downturn. The episode underscores how delta-hedged stablecoins transmit funding shocks into the spot marketplace for native cryptocurrencies reminiscent of ether. When the yield unfold flips signal, redemptions speed up, and leverage throughout the crypto ecosystem contracts as merchants shut leveraged ether positions and cut back publicity to derivatives. This closing of positions results in decrease ether costs and extra closing of leveraged positions, an on-chain model of a margin spiral.

Because of this unwinding, USDe’s market capitalization contracted by greater than 13 % following a pointy funding-rate reversal, because the unfold between its yield and ether staking turned detrimental and traders raced for the exits. As redemptions flowed, the protocol closed its perpetual-futures shorts and launched ether collateral, producing purchase strain in futures markets and promote strain in spot markets virtually concurrently. The mechanics mirror conventional deleveraging spirals: leveraged positions unwind, pressured gross sales hit the spot market, liquidity evaporates, and the unique collateral asset worth spirals downward.

The timing of those flows mattered. As liquidity thinned and funding charges worsened, the flexibility for arbitrageurs to transform USDe again into ETH or greenback equivalents slowed markedly. On the centralized alternate Binance, the place USDe buying and selling was thinner, costs briefly fell to US $0.65 regardless of on-chain peg integrity elsewhere. In keeping with CoinDesk, this was as a result of Binance’s value oracle referenced its personal value feed, making a procyclical impact that stored the worth de-pegged for a couple of hours.

The mixture of funding losses, collateral outflows, and liquidity pressure pushed ether right into a deeper decline. The end result was a reinforcing loop: decrease ether costs diminished the worth of the posted collateral, triggering further redemptions or liquidations, which in flip additional depressed costs and funding charges. Briefly, the synthetic-dollar unwind grew to become a transmission channel from the stablecoin system into crypto-asset costs.

Closing Phrases

The deleveraging of USDe didn’t happen in isolation: it happened amid a broader funding squeeze and falling asset costs in native cryptocurrencies and different dangerous asset markets. However the magnitude of USDe’s declines and its design counsel it performed a cloth position in amplifying the decline in ether costs.

Of be aware, the market-leading, asset-backed stablecoins of Tether’s USDT and Circle’s USDC didn’t de-anchor from their fiat greenback targets in the course of the October 10 Ethena deleveraging episode. Circle’s USDC misplaced $280 million in market cap that day and Tether’s USDT gained a virtually equal $282 million, whereas each maintained their greenback targets.

These kinds of crises are more and more related to policymakers, since stablecoins, tokenized money-market funds, shares, and exchange-traded funds are creating rising hyperlinks between conventional and blockchain-based monetary markets. The entire market capitalization of U.S. Bitcoin, Ether, and Solana ETFs is now round $95 billion. Tokenized Treasury funds convey short-term authorities debt immediately onto public blockchains, permitting traders to maneuver simply between DeFi and greenback belongings. Main intermediaries proceed to increase into this house. Because the connections between crypto and the standard monetary system deepen, crises such because the one involving artificial stablecoins have the potential to transmit volatility to conventional monetary markets.

Pablo Azar is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jeff Garofano is a capital markets buying and selling affiliate within the Federal Reserve Financial institution of New York’s Markets Group.

The right way to cite this put up:

Pablo D. Azar and Jeff Garofano, “Artificial Stablecoins and Monetary Stability,” Federal Reserve Financial institution of New York Liberty Road Economics, June 23, 2026, https://doi.org/10.59576/lse.20260623

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).