{kind=link}

For many of our historical past, the area of the monetary advisor has been serving to shoppers to take a position their financial savings in publicly traded shares and bonds that create alternatives for long-term progress, so as to obtain shoppers’ retirement and different financial savings targets. Whereas the actual automobiles have modified over time – from particular person securities, to mutual funds, to exchange-traded funds – the underlying continuity has been that each one of those issuers are registered with and are topic to the reporting requirements of the Securities and Change Fee (SEC), which mandates detailed and intensive disclosures in regards to the issuer, its enterprise, and the securities being provided. Extra not too long ago, as corporations are staying personal longer and issuing extra personal fairness and debt, personal investments and funds have proliferated, and increasingly advisory corporations are actually exploring whether or not so as to add allocations of personal funds into their consumer portfolios. Nonetheless, with out the rigorous disclosures required of issuers due to SEC registration and reporting, it’s considerably more durable for advisors to conduct due diligence on personal funds, which current funding and authorized dangers not typical for many public investments.

On this visitor submit, Wealthy Chen, founding father of Brightstar Legislation Group, explores the sensible due diligence concerns that advisors should navigate when contemplating a non-public fund funding, with a specific give attention to what to search for in governing paperwork and the operational programs of the personal fund.

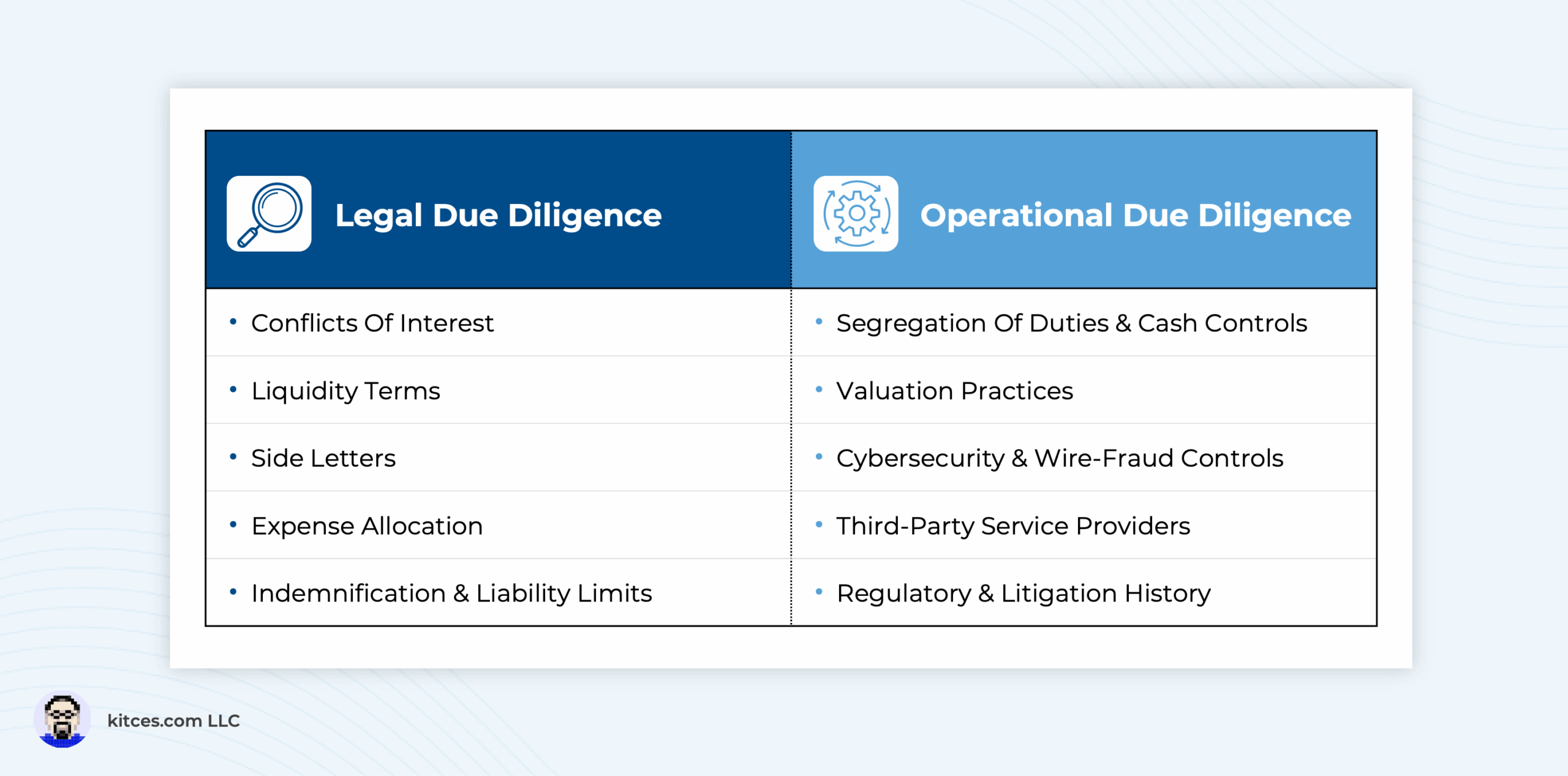

The start line in due diligence is to acknowledge that what’s acknowledged in authorized governing paperwork can differ fairly considerably from a non-public fund’s advertising supplies, because the latter is written to draw buyers to the fund by specializing in the alternatives, whereas the previous is written to attenuate the dangers for the fund sponsor (and thus extra clearly articulates the rights of buyers who put {dollars} into the fund). Accordingly, an in depth evaluation of governing paperwork can spotlight conflicts of curiosity (e.g., between the fund sponsor and affiliated events), reveal restrictions on an investor’s skill to exit the fund funding (which may typically be vital), establish red-flags relating to indemnification provisions, and element how bills will probably be allotted between buyers and fund administration. As well as, due diligence of governing paperwork gives a chance to ask about “facet letters” to find out if different buyers may need preferential or totally different rights or return alternatives.

Past due diligence of authorized paperwork, it is also necessary to guage a non-public fund’s operational programs, and the way successfully they’re constructed to guard buyers. For example, does the personal fund segregate key capabilities, guarantee twin authorizations for disbursements, use an outdoor custodian or separate accounting agency, and conduct annual audits? These measures can considerably mitigate dangers of fraud or misappropriation by the supervisor or its personnel. Equally, advisors can inquire in regards to the agency’s cybersecurity and consumer information protections, interact in background checks of the fund sponsor’s historical past (to make sure no prior authorized points or enforcement actions!), and decide how the agency values its property (particularly in circumstances the place it calculates carried curiosity or different administration charges primarily based on these valuations).

In the end, Chen gives a due diligence guidelines to assist help the method, although notably it is not sufficient to simply ‘mechanically’ full a guidelines; as a substitute, the SEC expects to see advisors exhibiting contemporaneous documentation that they have been considerate of their questions and analysis of the solutions offered, to show robustness of the method itself – for which advisors might even want to interact outdoors suppliers to help in due diligence (particularly if their inside sources are restricted). The expansion of corporations within the personal markets represents a big alternative for shoppers to take a position, however those that are accustomed to the pure protections the SEC has constructed into public markets have to be cognizant that there are distinctive dangers of personal fairness and debt funds that, at least, require a substantive proactive due diligence course of from monetary advisors (with the SEC more and more making use of enforcement actions in opposition to advisory corporations that “simply” relied on the advertising supplies and representations of the personal fund sponsor alone).