In 2025, the Federal Reserve has reduce rates of interest, commerce coverage has shifted abruptly, and financial coverage uncertainty has elevated. How have these developments affected the functioning of the important thing U.S. Treasury securities market? On this put up, we return to some acquainted metrics to evaluate the latest conduct of Treasury market liquidity. We discover that liquidity briefly worsened across the April 2025 tariff bulletins however that its relation to Treasury volatility has been just like what it was prior to now.

Why Treasury Market Liquidity Issues

The U.S. Treasury market is the biggest securities market on the planet, with practically $30 trillion in marketable debt excellent as of September 30. The market is utilized by the Treasury Division to finance the U.S. authorities, by the Fed to implement financial coverage, and by quite a few monetary establishments as a protected asset, to handle rate of interest threat, and to worth different securities. Liquidity is essential to all of those makes use of and is therefore adopted carefully by each market contributors and policymakers.

How We Measure Treasury Market Liquidity

Market liquidity could be outlined as the price of rapidly changing an asset into money (or vice versa) and could also be measured in a number of methods. As in previous work, we have a look at three widespread measures, estimated utilizing high-frequency knowledge from the interdealer market: the bid-ask unfold, the order ebook depth, and the worth affect. The measures are calculated for probably the most lately auctioned (on-the-run) two-, five-, and ten-year notes (the three most actively traded Treasury securities, as proven in this put up) over New York buying and selling hours (outlined as 7:30 a.m. to five p.m., jap time).

Liquidity Deteriorated in April 2025

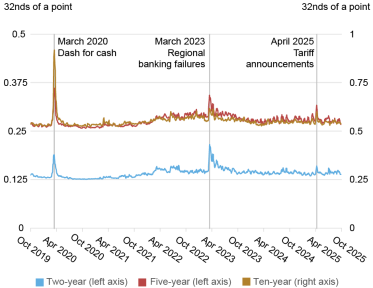

The bid-ask unfold is the distinction between the bottom ask worth and the best bid worth for a safety, with a wider unfold suggesting worse liquidity. Bid-ask spreads, proven within the chart under, widened notably after the April 2 tariff announcement, albeit to a a lot lesser extent than in March 2020 and even considerably lower than in the course of the March 2023 regional banking turmoil. Bid-ask spreads then narrowed after the April 9 announcement that the brand new tariffs had been principally being postponed and have since been commensurate with ranges usually noticed lately.

Bid-Ask Spreads Widened in April 2025

Notes: The chart plots five-day shifting averages of common every day bid-ask spreads for the on-the-run two-, five-, and ten-year notes within the interdealer market from October 1, 2019, to September 30, 2025. Spreads are measured in 32nds of a degree, the place a degree equals one % of par. Vertical strains flag the peaks within the five-day shifting common for the ten-year be aware, that are centered round March 16, 2020, March 15, 2023, and April 9, 2025.

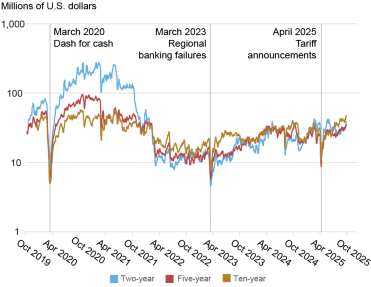

The following chart plots order ebook depth, measured as the common amount of securities out there on the market or buy at the very best bid and supply costs. This metric additionally factors to comparatively poor liquidity in April 2025, when out there depth declined to the bottom ranges since March 2023. Depth then rapidly recovered and by late summer season 2025 was at ranges just like, if not higher than, at any time because the begin of the Fed’s post-COVID tightening cycle in March 2022.

Order Ebook Depth Dropped in April 2025

Notes: The chart plots five-day shifting averages of common every day depth for the on‑the‑run two-, five-, and ten-year notes within the interdealer market from October 1, 2019, to September 30, 2025. Information are for order ebook depth on the inside tier, averaged throughout the bid and supply sides. Depth is measured in thousands and thousands of U.S. {dollars} par and plotted on a logarithmic scale. Vertical strains flag the low factors within the five-day shifting common for the ten-year be aware, that are centered round March 16, 2020, March 15, 2023, and April 9, 2025.

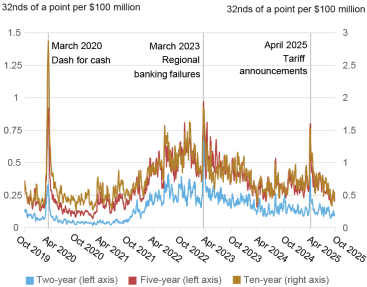

Measures of the worth affect of trades additionally recommend a pointy deterioration of liquidity in April 2025. The following chart plots the estimated worth affect per $100 million in web order circulate (outlined as buyer-initiated buying and selling quantity much less seller-initiated buying and selling quantity). The next worth affect suggests lowered liquidity. Value affect rose abruptly on April 2, however then rapidly reverted. By late summer season 2025, worth affect was about as little as at any time since early 2022.

Value Influence Rose in April 2025

Notes: The chart plots five-day shifting averages of slope coefficients from every day regressions of one-minute worth modifications on one-minute web order circulate (buyer-initiated buying and selling quantity much less seller-initiated buying and selling quantity) for the on-the-run two-, five-, and ten-year notes within the interdealer market from October 1, 2019, to September 30, 2025. Value affect is measured in 32nds of a degree per $100 million, the place a degree equals one % of par. Vertical strains flag the peaks within the five-day shifting common for the ten-year be aware, that are centered round March 17, 2020, March 16, 2023, and April 9, 2025.

Liquidity Intently Tracks Volatility

An in depth damaging relationship between Treasury liquidity and worth volatility is properly documented (see this examine, for instance). Volatility causes market makers to widen their bid-ask spreads and put up much less depth to handle the elevated threat of taking positions. Volatility, in flip, is pushed by uncertainty in regards to the anticipated path of rates of interest, reflecting uncertainty about financial progress, inflation, and coverage, each fiscal and financial.

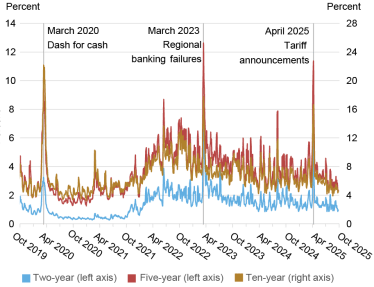

As proven within the subsequent chart, Treasury worth volatility rose sharply following the April 2 tariff announcement, peaking between April 7 and April 9. Volatility then rapidly declined after the April 9 announcement that the tariffs had been being postponed. Volatility continued trending down in subsequent months, and—like the worth affect—by late summer season was roughly as little as at any time since early 2022.

Value Volatility Spiked in April 2025

Notes: The chart plots five-day shifting averages of worth volatility for the on-the-run two-, five-, and ten-year notes within the interdealer market from October 1, 2019, to September 30, 2025. Value volatility is calculated for every day by summing squared one-minute returns (log modifications in midpoint costs) from 7:30 a.m. to five p.m., annualizing by multiplying by 252, after which taking the sq. root. It’s reported in %. Vertical strains flag the peaks within the five-day shifting common for the ten-year be aware, that are centered round March 11, 2020, March 14, 2023, and April 8, 2025.

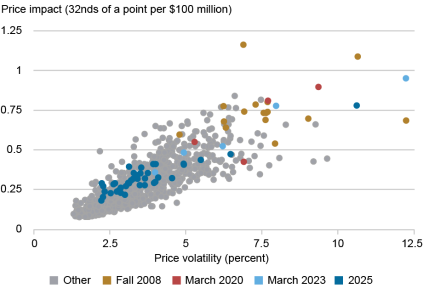

As with Liberty Road Economics posts in 2022 and 2023, we assess whether or not liquidity has been uncommon given the extent of volatility by inspecting scatter plots of worth affect in opposition to volatility. The chart under offers such a plot for the five-year be aware, displaying that the 2025 observations (in darkish blue) fall in step with the historic relationship. That’s, the affiliation between liquidity and volatility in 2025 has been according to the previous affiliation between these two variables; comparable outcomes are proven within the presentation accompanying this speech by Roberto Perli, supervisor of the System Open Market Account, utilizing a considerably completely different method.

Liquidity and Volatility in Line with Historic Relationship

Notes: The chart plots worth affect in opposition to worth volatility by week for the on-the-run five-year be aware from January 2, 2005, to September 30, 2025. The weekly measures for each collection are averages of the every day measures plotted within the previous two charts. Fall 2008 factors are for September 14, 2008–January 3, 2009, March 2020 factors are for March 1, 2020–March 28, 2020, March 2023 factors are for February 26, 2023–April 1, 2023, and 2025 factors are for December 29, 2024–September 30, 2025.

Liquidity Bears Shut Watching

Though U.S. Treasury market liquidity has not been uncommon given the extent of volatility, it nonetheless bears shut watching. Liquidity is essential to many important makes use of of this necessary market, as famous earlier. Market liquidity has additionally skilled periodic disruptions, as proven above, and faces the continuing problem of progress in Treasury debt excellent amidst restricted supplier capability. On the identical time, policymakers have taken many steps to advertise Treasury market resilience. It stays to be seen how these varied developments will have an effect on market functioning and liquidity.

Michael J. Fleming is head of Capital Markets within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The best way to cite this put up:

Michael J. Fleming, “How Has Treasury Market Liquidity Fared in 2025?,” Federal Reserve Financial institution of New York Liberty Road Economics, November 12, 2025, https://doi.org/10.59576/lse.20251112

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).