{kind=link}

Economics and enterprise correspondents usually function apologists for poor coverage. Their motivation is to file a narrative and infrequently they take the simple approach out by paraphrasing press releases put out by some conservative assume tank, or economist, or company with none important scrutiny being utilized after which masquerading their article as opinion. The opposite method is to rehearse some elementary mainstream macroeconomic textbook and declare the ‘concept’ might be utilized to justify selections taken by the fiscal and/or financial authorities. Final week (June 24, 2026), the Deputy Governor of the RBA gave a speech to the Financial Society of Australia in Melbourne – “The Straight Line Belongs to Man, the Curved Line Belongs to God” – which tried to justify the unjustifiable price hikes within the present inflationary episode. The reporting of that speech was lame to say the least. Over the weekend (June 26, 2026), there was one such article revealed within the Melbourne Age – Why the RBA has been so chill about placing jobs on the road – that simply repeats the RBA line and fails to see the precise subject.

As common readers know, the Reserve Financial institution of Australia has in my estimation an appalling file with regards to managing rates of interest.

They’re typically ‘forward of the curve’ – placing charges up properly earlier than there may be any signal of extra demand and in addition typically ‘behind the curve’ – protecting charges up at elevated ranges when there isn’t a justification for doing so.

Within the inflationary episode that got here with the pandemic, the RBA regularly tried to say it was an extra demand occasion and that the unemployment price was properly beneath the Non-Accelerating-Inflation-Fee-of-Unemployment (NAIRU), which meant that, in line with the mainstream logic, they needed to drive the unemployment price as much as suppress the inflationary pressures

On the time, I used to be one of many few economists who challenged the speed climbing logic by mentioning that the inflationary pressures have been as a result of provide constraints (closed factories, stalled transport programs, and many others) and would resolve pretty shortly as soon as the federal government restrictions have been eliminated.

For instance, on June 8, 2021, the UK Guardian revealed an Op Ed from me – Worth rises needs to be short-lived – so let’s not resurrect inflation as a bogeyman – the place I argued the value spikes have been transient, and will probably be absorbed with none entrenched inflation rising.

They actually didn’t justify a return to austerity or a tightening of financial coverage.

I feel the occasions that adopted proved that evaluation right and Japan, for instance, which didn’t observe the manic neoliberal climbing method of different central banks noticed inflation drop again extra shortly than the remainder of us.

One of many hanging misconceptions that the RBA pedalled to the general public throughout that interval was that the unemployment price was beneath their estimate of the unobservable NAIRU.

I wrote at size about that on the time, together with this weblog put up – Mainstream logic ought to conclude the Australian unemployment price is above the NAIRU not beneath it because the RBA claims (July 24, 2023).

The purpose was that the present RBA governor claimed that:

… the unemployment price should rise … the NAIRU … 4½ most likely appears, we expect, perhaps within the ballpark.

The mainstream concept summarises as:

1. When the unemployment price is above the NAIRU, inflation will decline.

2. When the unemployment price is beneath the NAIRU, inflation will speed up.

Whereas the NAIRU is unobservable and the estimates are all the time topic to very large commonplace errors (which make the purpose estimate ineffective for coverage anyway), we are able to observe the official unemployment price and the inflation price.

What did we observe?

1. From Might 2022, the Australia official unemployment price turned very steady round 3.5 per cent.

2. The inflation price rose throughout the worst of the pandemic because of the large provide impediments that Covid created exacerbated by the Ukraine scenario and OPEC+.

3. The inflation price peaked in September 2022, after which it declines steadily regardless that the unemployment price has remained very steady all through the rise and fall interval.

Making use of that mainstream logic would counsel the NAIRU, if it existed, should be beneath an unemployment price of three.5 per cent on condition that steady degree of unemployment had been related to a declining inflation price since round September 2022.

The RBA by no means addressed that flaw of their logic and even right now preserve batting on concerning the NAIRU and the necessity for price hikes.

Final week (June 24, 2026), the Deputy Governor of the RBA gave a speech to the Financial Society of Australia in Melbourne – “The Straight Line Belongs to Man, the Curved Line Belongs to God” – which tried to justify the unjustifiable price hikes within the present inflationary episode.

It’s clear that the present worth pressures have been additionally supply-driven because of Trump’s mad assaults on Iran and the harm that was finished to grease provide.

There isn’t any proof to assist an extra demand rationalization for the value rises and now with oil beginning to circulate once more, the value pressures are resolving pretty shortly.

However the RBA felt it needed to flex its mainstream muscle and hike charges, citing harmful demand pressures.

The Deputy Governor’s speech was concerning the Phillips curve – which is a significant macroeconomic framework modelling the connection between extra demand (inversely proxied by the unemployment price) and the inflation price.

I did a ten half sequence on the connection between unemployment and inflation (as a part of my documenting the writing of our Macroeconomic textbook).

That is half 10 – Unemployment and Inflation – Half 10 – which comprises hyperlinks to all the sooner elements.

The dialogue of the Phillips curve begins in – Unemployment and inflation – Half 2 (February 8, 2013) – and continues into the next elements.

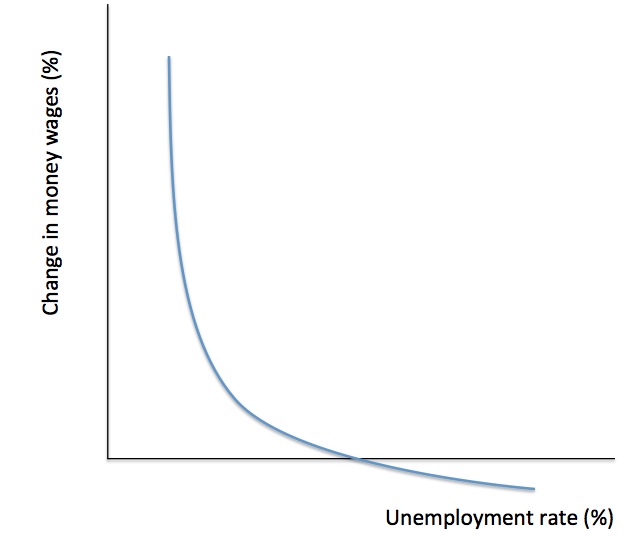

For those who refresh your reminiscence of the idea, you’ll encounter this diagram:

This diagram is the premise of the Deputy Governor’s speech final week.

The essence of his speech which was used to justify the present RBA’s financial coverage place even supposing the unemployment price is rising was that the Phillips curve is non-linear (that’s, not a straight line).

The RBA declare that the economic system is now working on the very steep (close to vertical) part of the Phillips curve:

Typically, the extra nonlinear the Phillips curve is, the stronger is the case for central banks who consider they’re on the steeper a part of the curve to take pro-active coverage motion to scale back extreme capability pressures …

The choice in February mirrored issues that we have been sliding up the steeper a part of the Phillips curve …

The purpose is that if the economic system is working on that part of the trade-off (we’re speaking right here as if the entire framework is legitimate), then attacking inflation with larger rates of interest could have very small unfavorable impacts on the unemployment price.

If the economic system was working on the horizontal part, then small drops in inflation would have very massive unfavorable impacts on the unemployment price.

The Deputy Governor stated:

The purpose of tighter coverage is to ship a interval of below-trend demand development, lowering capability pressures and returning inflation to focus on. However that is the place being on the steeper a part of the Phillips curve has a possible silver lining – as a result of whereas it implies that will increase in extra demand have a proportionally bigger influence on inflation on the way in which up … it additionally implies that well timed coverage steps to scale back inflationary pressures, of the sort we’ve got taken, must also have a proportionally smaller unemployment value (or ‘sacrifice ratio’) on the way in which down.

So the RBA, women and gents actually do care concerning the individuals they’ve put out of labor because of the speed hikes.

No less than that’s what they need us to consider.

The issue with all of that is that the evaluation assumes that the inflationary pressures are the results of extra demand.

The logic is that in instances of sturdy development, the labour market disequilibrium (extra demand for labour) will increase bargaining energy of unions and reduces unemployment and this results in a rise within the price of cash wages development.

And that interprets into individuals spending an excessive amount of relative to the provision capability of the economic system to fulfill the demand with additional output.

Outcome: inflation accelerates.

There may be scant proof to assist that evaluation.

The newest – Client Worth Index, Australia – information revealed June 24, 2026 by the Australian Bureau of Statistics, confirmed the inflation price falling shortly.

If fell 0.7 per cent in Might.

The primary drivers are housing (rents and electrical energy) and gas costs.

None of those drivers mirror extreme spending.

As soon as the oil begins to circulate once more, the CPI will drop quickly.

The Phillips curve framework differentiates between actions alongside a given curve and shifts within the curve.

Actions alongside are as a result of adjustments in demand (spending) which set off the trade-off between inflation and unemployment.

Shifts within the curve may result from altering inflationary expectations, which suggests at each unemployment price, individuals anticipate larger inflation which shifts the curve up.

Or it may well come from momentary provide shocks such because the Iran battle the place value pressures rise and inflation is larger at each unemployment price.

At current, there isn’t a proof that inflationary expectations are accelerating upwards.

There may be ample proof that there was a transient shift up within the relationship between inflation and unemployment as a result of larger power prices straight impacting on the transport part of the CPI and not directly impacting on manufacturing prices and different CPI parts (deliveries and many others).

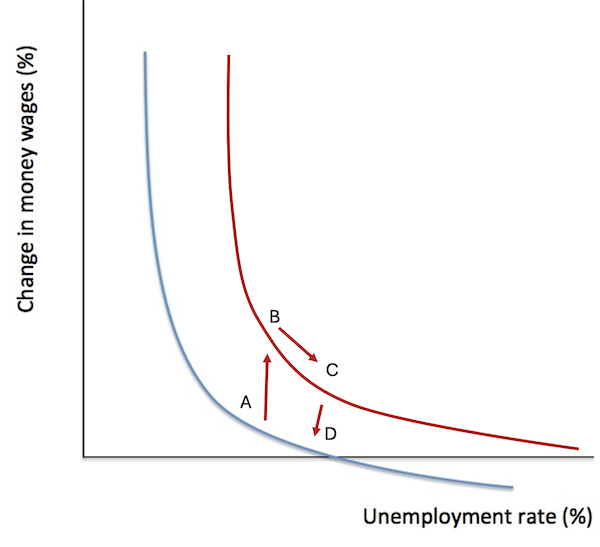

For those who have a look at the next additions to the Phillips curve above we are able to see the difficulty.

Suppose the economic system is at level A.

The Iran Battle happens and inflation at each unemployment price abruptly accelerates.

In Phillips curve discuss, we seize that by the purple curve and the economic system shifts from A to B, with none apparent extra demand pressures being current.

The RBA hikes charges to drive unemployment as much as stifle the imaginary extra demand pressures, pondering it’s nonetheless on the unique Phillips curve.

But it surely pushes the economic system from B to C.

In the meantime, the Battle ends (kind of) and the transient supply-driven inflation abates and the curve shifts again in to the unique relationship.

The issue is that the economic system then shifts from C to D so we’re caught with low inflation however larger unemployment.

If the RBA had not hiked charges, the economic system would have moved fairly merely from B again to A as the provision pressures abated.

The journalist within the article I cited on the outset utterly failed to grasp that time.

She additionally rehearsed the usual mainstream line that “unemployment has remained close to traditionally low ranges”.

I’m wondering when historical past started for her?

Historic lows are beneath 2 per cent for a number of many years not 4.3 per cent for a couple of (neoliberal) many years.

Information Merchandise 1 – Macroeconomics Textbook

Tomorrow I’ll ship the ultimate manuscript of the second version of our – Macroeconomics – textbook, which first got here out in 2019.

The second version has many additions and will probably be out a while in 2027.

It has been a giant job to get it to this stage.

Information Merchandise 2 – Unions and Neighborhood drive Australian authorities to retreat from ridiculous outsourcing plan

Earlier within the yr, I wrote this weblog put up – A traditional case of the Australian authorities denying that it’s the Australian authorities (April 20, 2026) – which summarised how the Federal authorities company that runs out airport security programs – Airservices Australia – had cooked up a plan to outsource the availability of all of the infrastructure (fireplace vans, stations, emergency gear and many others) to a monetary market entity.

They employed one of many huge Administration Advisor companies (and doubtless paid them heaps) to provide you with the spin – a so-called ‘Worth for Cash’ Proposal – the place they claimed that the plan would save the federal authorities cash.

It by no means stood as much as scrutiny.

I used to be commissioned by the United Firefighters Union (Aviation Department) to mannequin the proposal and decide its validity.

My report – A critique of the proposal to outsource ARFFS infrastructure procurement and administration by Airservices Australia (ultimate model revealed Might 4, 2026) – discovered that:

1. Airservices Australia is a completely government-owned statutory authority whose major position is to make sure the secure administration of Australian airspace and airport rescue and firefighting providers.

2. The Commonwealth in the end stays financially accountable for Airservices and may present low-cost funding when wanted.

3. Direct public funding could be cheaper, extra environment friendly, and extra per the statutory goal of Airservices Australia as a public service supplier quite than a profit-seeking company.

4. Since each events should fund the identical funding outlay profile, the one distinction is the price of capital utilized to these outlays over time. A decrease financing price signifies that much less curiosity accumulates on borrowed funds throughout the funding interval and over the compensation interval.

The federal government subsequently incurs a smaller complete compensation obligation as a result of annually’s borrowing compounds at 5 per cent quite than 8 per cent.

In sensible phrases, the non-public supplier should recuperate not solely the infrastructure funding prices but in addition a better required return to lenders and shareholders, making the privately financed choice costlier to the general public purse or customers over the lifetime of the asset.

Our conclusion is that the non-public supplier creates a further financing burden of round 7.4 per cent greater than direct government-financed provision solely due to the upper value of capital.

That’s, the direct authorities provision is $135 million cheaper.

The publication of my report by the Union and enter at Senate hearings and many others, introduced the difficulty out into the general public area.

Final Thursday, after a concerted marketing campaign by the unions concerned and neighborhood teams, the nationwide media introduced that the federal government by way of Airservices Australia had:

… formally deserted its controversial $1.8 billion aviation firefighting and infrastructure privatisation technique in June 2026. The board rejected the sale-and-leaseback proposal after intense pushback from unions and unbiased modelling revealing it might value taxpayers an additional $135 million.

A small victory for the neighborhood and staff.

That’s sufficient for right now!

(c) Copyright 2026 William Mitchell. All Rights Reserved.