Present discussions concerning a bifurcated U.S. economic system spotlight the growing financial divide between lower- and higher-income People in spending and earnings development and wealth accumulation. Whereas many households are doing wonderful and financial exercise total has been increasing at a strong tempo, massive segments of the inhabitants are going through excessive ranges of financial insecurity and monetary pressure, and shopper sentiment on the entire has dropped to low ranges. On this put up, we use newly collected knowledge from the Survey of Client Expectations (SCE) to replace our 2020 evaluation of disproportionate monetary hardship skilled in the course of the early pandemic and to research current adjustments in meals insecurity and broader financial strains. We then look at how meals insecurity pertains to the rise in shopper pessimism. We discover a exceptional enhance in meals insecurity, notably amongst lower-educated and lower-income households and households with younger youngsters. We doc a contemporaneous enhance in pessimism among the many similar teams, together with a pointy decline in job-finding expectations.

Declining Client Sentiment in a Ok-Formed Economic system

Regardless of strong financial fundamentals (low unemployment, traditionally excessive family web wealth, and resilient shopper spending), customers total have been pessimistic about their very own monetary circumstances and outlook. Present ranges of shopper sentiment, capturing how optimistic customers are about their private funds and the general economic system, have fallen close to or beneath the low ranges seen in the course of the Nice Recession and pandemic.

These macroeconomic indicators masks vital heterogeneity throughout households, supporting the notion of a “Ok-shaped” economic system, through which consumption development in recent times has been pushed largely by higher-income and college-educated households whereas lower-income households have seen fewer good points. The highest of the Ok-shape displays excessive and rising ranges of web wealth, fueled by rising inventory costs, near-peak dwelling fairness ranges, and reductions in mortgage funds following the 2020-21 refinance increase. The underside of the Ok-shape represents a big share of the middle- and lower-income inhabitants experiencing elevated ranges of financial uncertainty and monetary hardship. Such monetary stress is mirrored in considerations about affordability as a result of excessive value of residing, persistent inflation, and excessive rates of interest, and in excessive delinquency charges for bank cards and auto and pupil loans.

Decrease- and middle-income households typically have skilled larger efficient inflation charges, with a larger share of their spending allotted to items which have seen costs soar because the pandemic, akin to housing, groceries, and utilities, inflicting them to chop again on groceries. The larger monetary pressure as a result of excessive value of residing, mixed with the expiration of pandemic-era assist (akin to expanded SNAP advantages), have led to renewed considerations about meals insecurity amongst these on the backside of the Ok-shape.

New Proof from the Survey of Client Expectations

To offer additional current proof on monetary and meals insecurity, we draw on the SCE. The SCE is a month-to-month internet-based survey that has been performed by the Federal Reserve Financial institution of New York since June 2013. It’s based mostly on a twelve-month rotating panel of roughly 1,200 nationally consultant U.S. family heads. As a part of its Could and June 2020, October 2025, and February 2026 surveys, the SCE included a set of focused questions to review family monetary stress and meals insufficiency, in addition to households’ expectations about their monetary scenario a yr from now.

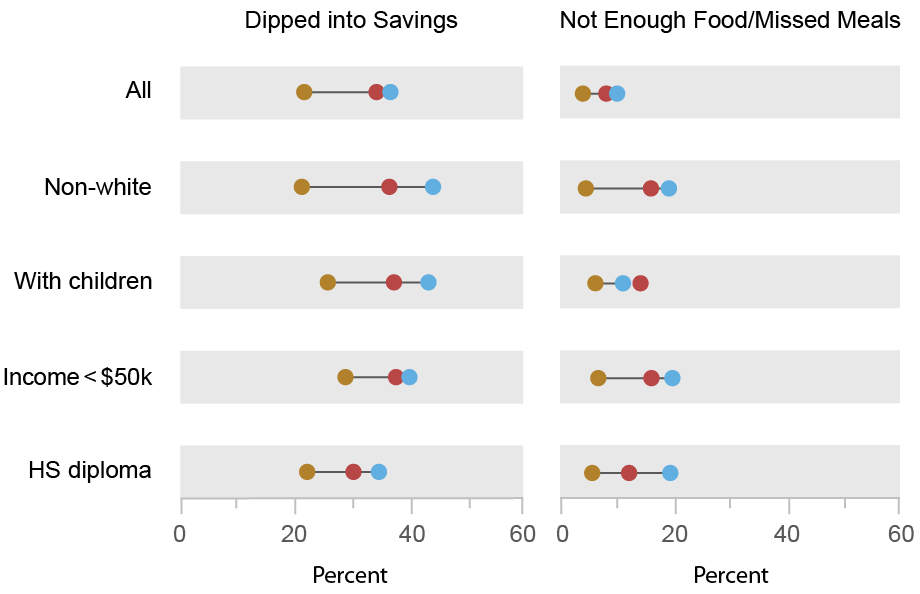

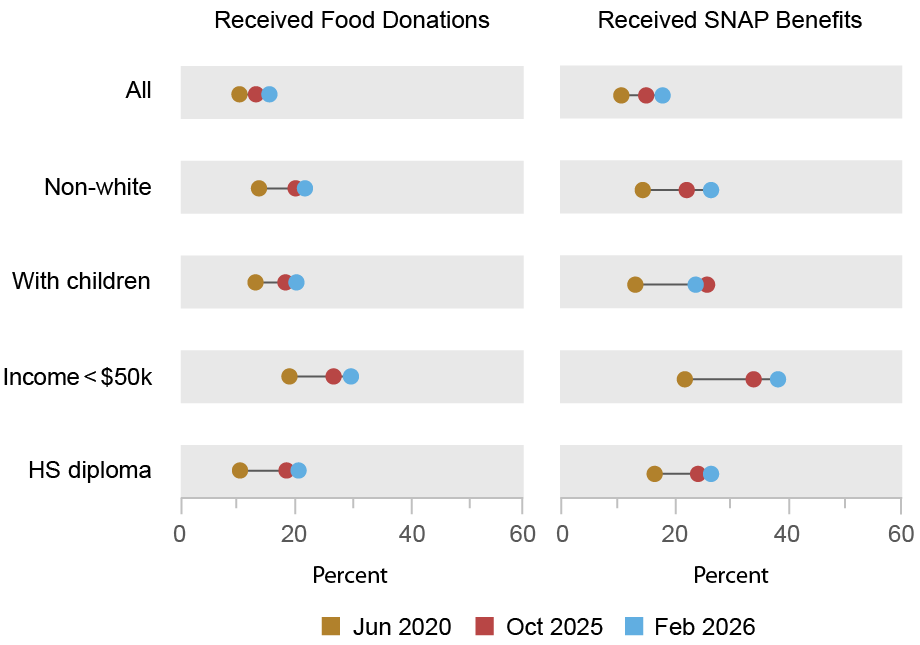

Particularly, we requested family heads whether or not they (or somebody of their family) skilled any of the next 4 occasions over the prior three months: dipped into financial savings or emergency accounts to cowl bills; had bother discovering sufficient meals to eat or had youngsters who missed meals; acquired meals donations from household, associates, or meals banks; or acquired assist via SNAP. Word that eligibility for SNAP advantages is predicated on family revenue and dimension, and is an imperfect proxy for meals insecurity. In our evaluation, we pool knowledge from the 2 2020 surveys and confer with it because the June 2020 survey.

As proven within the charts beneath, since Could/June 2020, and likewise between October 2025 and February 2026, there have been significant will increase within the shares of households reporting that they’d skilled the 4 conditions described above. The will increase have been principally broad-based throughout race, age, revenue, and training teams, however have been typically bigger for non-whites, lower-income and lower-educated households, and households with youngsters, as detailed within the chart.

Broad-Based mostly Will increase in Meals Insecurity and Broader Financial Strains Since 2020

Notes: The chart exhibits the shares of respondents within the 4 surveys (Could 2020 and June 2020 outcomes are grouped as June 2020) who reported that over the earlier three months they (or somebody of their family) had dipped into financial savings and emergency accounts to cowl bills; had bother discovering sufficient meals to eat or had youngsters who missed meals; acquired meals donations from household, associates, or meals banks; or acquired assist via SNAP.

Whereas associated, our measures differ from the U.S. Division of Agriculture’s (USDA) official survey measure of meals insecurity, which goals to seize “the restricted or unsure availability of nutritionally ample and protected meals, or restricted or unsure skill to amass acceptable meals in socially acceptable methods.” The USDA’s measure of meals insecurity for 2024, its most up-to-date survey, stood at 13.7 p.c of households (18.4 p.c amongst households with youngsters). The speed is the very best since reaching a post-2001 low of 10.2 p.c in 2021 however stays beneath its post-2001 excessive of 14.9 p.c attained in 2011. Meals insecurity is related to poor well being outcomes in addition to decrease instructional attainment, employee productiveness, and lifelong earnings.

Elevated Meals Insecurity Is Additionally Related to Declining Client Sentiment

Along with the growing development in these shares, we discover that amongst these reporting incidents of meals insufficiency (not sufficient meals, acquired meals donations) and SNAP receipt, there’s a decrease, and extra quickly declining, web share of respondents anticipating to be higher versus worse off financially a yr from now (as proven within the desk beneath). Which means a rise within the incidence of meals insecurity is related to a deterioration in shopper sentiment. Nonetheless, the rise in meals insecurity clearly will not be the one issue that issues—even amongst these not reporting these incidents of meals insecurity we discover a sizable decline between 2020 and October 2025 within the web share of respondents anticipating to be higher versus worse off a yr from now, although this decline was adopted by partial reversal from October 2025 to February 2026.

Meals Insecure Households Report Higher Pessimism on the Economic system, Labor Market, and Debt

| Family expectations | Could/June 2020 | October 2025 | February 2026 |

| Internet share higher/worse off | 8.0 | -4.2 | –0.6 |

| – Not sufficient meals/skipped meals | -10.2 | -22.1 | -32.5 |

| – Acquired meals donations | 0.8 | -14.8 | -22.7 |

| – Acquired SNAP advantages | 0.4 | -0.2 | -11.7 |

| Common job-finding chance, if have been to lose job | 48.0 | 46.8 | 44.0 |

| – Not sufficient meals/skipped meals | 48.8 | 37.2 | 41.4 |

| – Acquired meals donations | 48.6 | 37.0 | 39.4 |

| – Acquired SNAP advantages | 50.1 | 36.7 | 33.7 |

| Common debt delinquency chance | 11.2 | 13.1 | 11.6 |

| – Not sufficient meals/skipped meals | 41.4 | 41.8 | 32.3 |

| – Acquired meals donations | 23.4 | 30.1 | 23.4 |

| – Acquired SNAP advantages | 19.6 | 31.1 | 20.3 |

Notes: The highest panel of the desk exhibits the online share of respondents anticipating their family to be financially higher versus worse off twelve months from now, total and for these reporting meals want and help, within the Could/June 2020, October 2025, and February 2026 surveys. The center panel exhibits, for every subgroup and survey wave, the common reported proportion probability of discovering a job throughout the following three months, if one’s job have been to be misplaced at present. The underside panel exhibits the common reported chance of, over the subsequent three months, not with the ability to make a minimal debt fee. See the SCE questionnaire for the precise query wordings.

Apparently, we additionally discover significantly bigger reductions within the anticipated job-finding charge (measured because the chance of discovering a job within the subsequent three months if one’s present job is misplaced) for these reporting meals wants or SNAP receipt. In distinction, we see little motion over the interval in debt delinquency expectations, which measures the chance of lacking a minimal debt fee throughout the subsequent three months—though it’s value noting that respondents who expertise meals insecurity have considerably larger debt delinquency expectations. Total, these tendencies level to a deterioration in sentiment or an elevated pessimism amongst those that report meals insecurity and SNAP receipt.

Whereas not essentially causal, the noticed constructive affiliation between meals insecurity and total shopper pessimism, along with the rise within the incidence of meals insecurity, particularly amongst households on the backside of the Ok-shape, level to a possible rationalization for the unusually low current ranges of shopper sentiment at a time when the onerous financial knowledge paint a extra constructive image.

Gizem Kosar is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ishva Mehta is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How one can cite this put up:

Gizem Kosar, Ishva Mehta, and Wilbert van der Klaauw, “Meals Insecurity and Client Pessimism,” Federal Reserve Financial institution of New York Liberty Avenue Economics, Could 27, 2026, https://doi.org/10.59576/lse.20260527

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).