Final Tuesday (Might 12, 2026), the Australian Treasurer launched the 2026-27 Fiscal Assertion (aka Federal ‘Finances’). I’ve been reluctant to touch upon the ‘Assertion’ given the fixed repetition by the Treasurer a couple of ‘trillion {dollars} of debt’ and all the remainder of the flawed conceptual growth and nomenclature that has surrounded its launch and subsequent public commentary. However I do wish to make a couple of feedback on a few of the element and subsequent commentary. The Authorities is operating scared for the time being as the acute Proper-wing political occasion, One Nation threatens to take a swathe of seats on the subsequent election (much like what Reform UK is doing). Additionally it is being bullied by the RBA Governor who’s threatening extra harmful price hikes if the federal government doesn’t minimize its fiscal deficit. Such a coverage stance will see unemployment rise additional (and in my estimation, a lot increased than the Authorities forecasts). And if there may be any development related to the fiscal stance it’ll come from growing family debt which is unsustainable given the report ranges of indebtedness at the moment endured by the family sector. General, this isn’t an fiscal spectacular assertion.

Introduction

The ‘Assertion’ made a lot of its intergenerational virtues, provided that it minimize a few of the tax benefits which have been channelling funding funds into speculative monetary property and actual property away from productive capital formation.

The wealth divide between staff who earn incomes and those who obtain earnings because of possession of economic and different speculative property has elevated fairly considerably over the past 20 years.

Youthful Australians are actually successfully locked out of the housing market as the rich indulge themselves in investments in a number of properties because of the tax write-offs that the coverage allowed.

A few of that largesse might be stifled by the brand new coverage however the shifts are minimal and don’t go to the center of the inequality drawback – that taxes on earnings can’t be shifted or averted by low-income earners whereas they are often considerably decreased by these on excessive incomes.

Australia wants a wealth tax and a better consumption tax to redress the discrepancies arising from the earnings tax system, however for that to occur, pigs would possibly fly.

I don’t actually wish to deal with these elements of the ‘Assertion’ anyway.

My focus is on the macroeconomics of the fiscal technique.

Abstract knowledge

In ‘Finances Paper No.1’, Assertion 2: Financial Outlook and Assertion 3: Fiscal Technique and Outlook, we observe the next forecasts.

I’ll mirror on this knowledge all through.

| Combination | 2024-25 (Precise) | 2025-26 | 2026-27 | 2027-28 |

| GDP development | 1.3 | 2.25 | 1.75 | 2.25 |

| Present Account (% of GDP) | -2.5 | -1.75 | -2.75 | -4.00 |

| Fiscal stability (% of GDP) | -1.0 | -1.0 | -1.0 | -0.7 |

| Public Remaining Demand | >4.2 | 2.75 | 2.75 | 2.5 |

| Employment | 2.1 | 1.5 | 1.5 | 1.75 |

| Unemployment | 4.2 | 4.25 | 4.25 | 4.25 |

| Participation price | 67.0 | 66.75 | 67.0 | 67.25 |

| Inflation | 2.1 | 5.0 | 2.5 | 2.5 |

Authorities is shifting to an inappropriate austerity stance

The Australian Monetary Evaluation revealed this Op Ed at the moment (Might 18, 2026)- ‘Chalmernomics finances sliced up however didn’t develop the pie – which claimed that:

What the federal government does have is “Chalmernomics” – the deliberate technique of utilizing all out there coverage devices to affect staff’ wages and employment outcomes extra immediately. It favours retrograde interventionism, usually no matter productiveness hyperlinks or long-term development. Chalmers’ macroeconomic pondering attracts closely on trendy financial principle (MMT) influences – activist fiscal coverage paired with accommodative financial coverage to supply a nominal anchor for wages and full employment. This helps clarify earlier RBA assessment outcomes and chronic dovish tendencies relative to see economies.

I believed I higher appropriate that mistaken (intentionally or in any other case) affiliation of the Authorities’s motivation and affect in drafting the ‘Assertion’ with my work (Trendy Financial Idea).

The creator is an ex-Treasury, IMF economist and will get a good quantity of media publicity in Australia.

Let me make it clear from the outset – the Treasurer (Chalmers) doesn’t assume by way of Trendy Financial Idea (MMT).

And MMT just isn’t an “activist fiscal coverage paired with accommodative financial coverage”.

Extra on that as we go

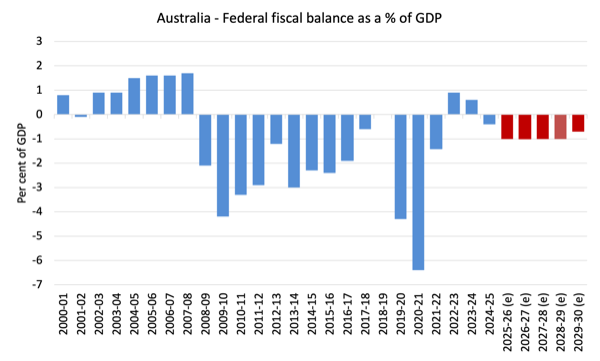

Right here is the fiscal place since 2000-01 with the purple bars indicating the forecast values.

Over the forecast interval there’s a slight contraction deliberate, which is why the unemployment price is forecast to rise.

Final evening’s assertion indicated that the federal authorities could be in fiscal deficit not less than out to 2029-30 – ‘deficits for so far as we are able to see’ is the favored criticism.

What number of commentators are you able to depend that use phrases akin to ‘eye watering deficits’ or comparable.

Nearly all of them, which ought to deem them unqualified to talk within the public enviornment as so-called ‘consultants’.

Since 1970-71, the fiscal deficit has averaged 0.9 per cent of GDP.

By 2028-29, it’s forecast to be 0.7 per cent of GDP.

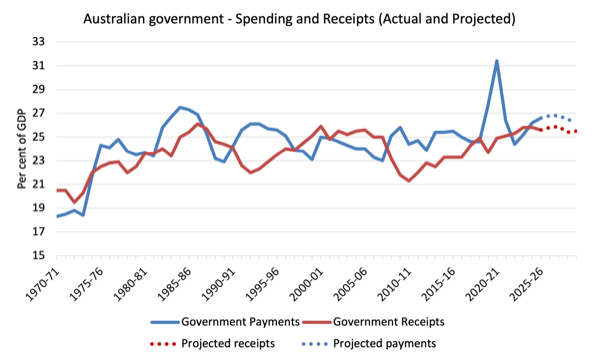

The next graph exhibits the motion in these aggregates as a p.c of GDP since 1970-71.

The dotted segments are the fiscal assertion projections.

You may see that whereas funds are projected to fall extra shortly than receipts, which is the rationale for the projected shrinkage fiscal deficit by 2029-30.

Each spending and receipts are barely above their historic common at current.

However there may be nothing wild occurring right here.

The fiscal assist through the pandemic was substantial however now the aggregates are returning to ‘base’.

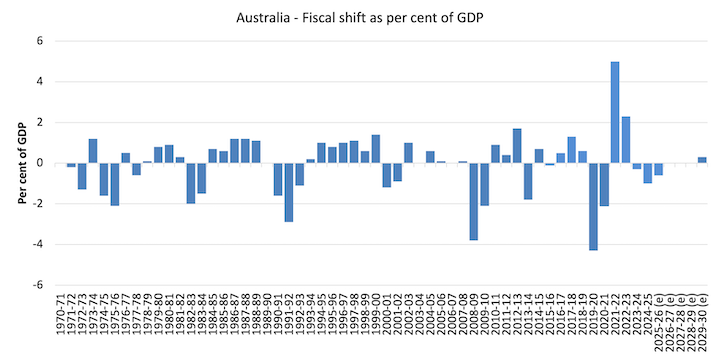

The fiscal shift from one yr to a different is the change within the fiscal stability as a share of GDP modifications.

It gives an concept of how expansionary or contractionary the present fiscal place is relative to the earlier monetary yr.

It’s the results of two components – the fiscal stability itself (in $As) and the worth of nominal GDP (in $As).

The next graph exhibits the latest historical past (from 1970-71) of fiscal shifts as much as the tip of the projection interval (2029-30).

A constructive worth signifies a contractionary shift (even when the fiscal place remains to be in deficit) and vice versa.

The contraction in 2021-22 was giant (a 5 per cent of GDP shift) because the Authorities deserted the pandemic assist.

Within the subsequent yr, the Authorities contraction continued (equal to 2.3 per cent of GDP) because it pursued surpluses – it recorded two surplus positions in 2023-24 and 2024-25.

However the sustained withdrawal of internet authorities spending killed financial development and the Authorities was then pressured to take an expansionary place because it approached a nationwide election.

The present ‘Assertion’ forecasts a steady deficit final result (zero shift) till an extra fiscal withdrawal by 2029-30.

Is that this an applicable fiscal place to venture over the following a number of years?

As I clarify under, the implication is that GDP development is not going to be adequate to maintain reductions within the nationwide unemployment price, which has risen considerably since 2024.

In that sense, the present fiscal deficit is simply too small and an extra contraction is taking coverage within the mistaken path.

Is the Authorities’s fiscal stance a mirrored image of the physique of labor that we now consult with as MMT?

I suppose it relies on what you assume MMT is?

In case your understanding is restricted to MMT being “activist fiscal coverage paired with accommodative financial coverage” then even then you wouldn’t conclude the present fiscal settings to be influenced by that restricted conceptualisation.

First, financial coverage is something however accommodative.

As I’ve written beforehand, the RBA has hiked charges after which threatened the federal government with extra of the identical if it didn’t begin shifting in direction of an austerity stance.

The Treasurer has acted accordingly and ignored all of the challenges dealing with the nation that require greater authorities (housing, local weather, unemployment, degradation of schooling, well being and many others) and determined to maneuver (slowly) in direction of a contractionary place.

A fiscal deficit of 1 per cent of GDP is simply too low given the possible improve within the exterior deficit and the state of family funds (see under for extra information to assist that assertion).

In different phrases, fiscal coverage is being formed by the dictates of the RBA.

An MMT economist, no matter their particular coverage preferences, would by no means see it applicable for the central financial institution to be figuring out the path of fiscal coverage.

The productiveness and unemployment inferences

The most recent ABS estimates (March 19, 2026) launched within the assertion – Media Launch – tells us that:

Australia’s inhabitants grew by 1.6 per cent within the 12 months to September 2025 …

Our inhabitants grew to 27.7 million, with 423,600 extra folks than in September 2024 …

Pure improve added 112,600 folks, with births up by 1.9 per cent and deaths down by 1.4 per cent.

Internet abroad migration added 311,000 folks over the yr.

The Treasury forecasts that labour power participation will rise a tad over the ahead estimates.

In ‘Assertion 2: Financial Outlook’ (pp.79-80), the Authorities presents Field 2.4: Productiveness transition and assumes that:

… underlying productiveness development transitions to its long-run development price over time. Underlying productiveness development is assumed to be 1.2 per cent in 2031–32.

How does that affect the unemployment price forecasts?

The well-known US economist Arthur Okun developed a rule of thumb about the best way unemployment reacts to GDP development.

The rule of thumb has it that if the unemployment price is to stay fixed, the speed of actual output (GDP) development should equal the speed of development within the labour power plus the expansion price in labour productiveness.

Do not forget that labour productiveness development reduces the necessity for labour for a given actual GDP development price whereas labour power development provides staff that should be accommodated for by the true GDP development (for a given productiveness development price).

If we assume the labour power grows in keeping with the assumed underlying inhabitants forecasts – so round 1.6 per cent (given participation is estimated solely barely increased – we are able to assume steady) and productiveness development is round 1.2 per cent on common over the ahead estimates, then GDP development needs to be 2.8 per cent on common in every of the forecast years if the unemployment price is to remain unchanged.

A cursory have a look at the Desk above, exhibits the next: if the forecasts become truth then the unemployment price will certainly rise from its present degree of 4.3 per cent, which means that the 4.25 per cent forecast is more likely to be too low.

1. 2025-26 – GDP is forecast to be 2.25 per cent or round 0.55 factors under the required price.

2. 2026-27 – GDP is forecast to be 1.75 per cent or round 1.05 factors under the required price.

3. 2027-28 – GDP is forecast to be 2.25 per cent or round 0.55 factors under the required price.

Whereas these figures are approximations, and productiveness development is assumed to transition to 1.2 per cent every year fairly than immediately attain that degree within the present yr, the outcomes recommend that there might be will increase within the unemployment price over the ahead estimates interval.

The Authorities forecasts that the unemployment price will rise from 4.2 per cent to 4.5 per cent over the interval to 2027-28.

What this implies is that the Authorities forecasts aren’t internally constant.

The one method that the unemployment price improve may very well be confined to 0.3 factors over the following three years is that if productiveness development stayed low or destructive.

The opposite method of contemplating that is to simulate the underlying labour power aggregates based mostly on the Treasury assumptions with respect to employment development.

That simulation (utilizing the ABS inhabitants development knowledge) and the Treasury employment development forecasts, delivers an unemployment price of 4.2 per cent by the tip of June 2028 with unemployment rising from 656.33 thousand in March 2026 (precise worth) to 676.55 thousand by the tip of June 2028.

But, the Authorities is forecasting the unemployment price to rise to 4.5 per cent.

Both method, the forecasts don’t communicate to one another.

My greatest guess is that the unemployment price will rise additional below the present coverage settings which are indicating a contraction in internet authorities spending.

Why the federal government technique is unsustainable

Trying again on the first Desk, we see that the expenditure drain from the exterior sector is predicted to extend fairly considerably over the forecast interval as the anticipated phrases of commerce decline considerably.

Ally that with the data that the fiscal deficit is forecast to say no from 1 per cent of GDP to 0.7 per cent.

Taken collectively it signifies that non-public home demand should do the lifting and that implies rising indebtedness.

We all know that the monetary stability between spending and earnings for the non-public home sector (S – I) equals the sum of the federal government monetary stability (G – T) plus the present account stability (CAB).

The sectoral balances equation is:

(1) (S – I) = (G – T) + CAB

which is interpreted as which means that authorities sector deficits (G – T > 0) and present account surpluses (CAD > 0) generate nationwide earnings and internet monetary property for the non-public home sector to internet save total (S – I > 0).

Conversely, authorities surpluses (G – T < 0) and present account deficits (CAD < 0) scale back nationwide earnings and undermine the capability of the non-public home sector to build up monetary property.

Expression (1) may also be written as:

(2) [(S – I) – CAB] = (G – T)

the place the time period on the left-hand facet [(S – I) – CAB] is the non-government sector monetary stability and is of equal and reverse signal to the federal government monetary stability.

That is the acquainted Trendy Financial Idea (MMT) assertion {that a} authorities sector deficit (surplus) is equal dollar-for-dollar to the non-government sector surplus (deficit).

The sectoral balances equation says that whole non-public financial savings (S) minus non-public funding (I) has to equal the general public deficit (spending, G minus taxes, T) plus internet exports (exports (X) minus imports (M)) plus internet earnings transfers.

All these relationships (equations) maintain as a matter of accounting.

The Authorities is estimating that the destructive international components will proceed to undermine Australia’s phrases of commerce.

By 2027-28, they forecast a decline of seven.25 per cent in our phrases of commerce

Australia is forecast to return to its ordinary place of an exterior deficit of 4 per cent of GDP – a state that has been dominant because the Seventies.

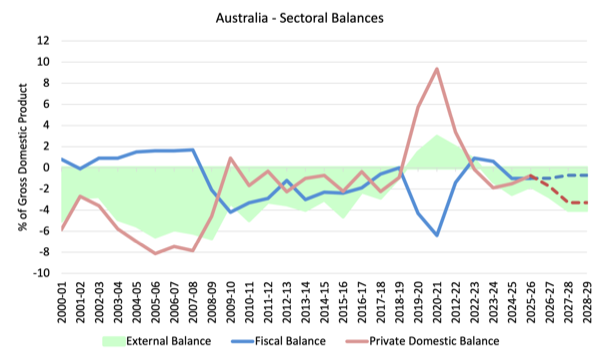

The next graph tells the story.

It exhibits the sectoral stability aggregates in Australia for the fiscal years 2000-01 to 2028-29, with the ahead years utilizing the Treasury projections revealed in ‘Finances Paper No.1’ in dotted kind.

The projections start in 2026-27 and I’ve assumed that 2028-29 final result might be equal to the 2027-28 Authorities estimate.

All of the aggregates are expressed by way of the stability as a p.c of GDP.

I’ve modelled the fiscal deficit as a destructive quantity although it quantities to a constructive injection to the economic system.

You additionally get to see the mirror picture relationship between it and the non-public stability extra clearly this fashion.

It turns into clear, that with the present account deficit (inexperienced space) projected to return growing deficits, which drain internet spending from the home economic system and with the fiscal stability shifting in direction of zero over the identical interval, the non-public home stability (purple line) will head shortly into increased deficits.

Increased non-public home deficits imply increased ranges of indebtedness.

The Family sector is already carrying report ranges of indebtedness which is why family consumption expenditure has been slowing down appreciably within the face of rising cost-of-living pressures.

So mirror on that in relation to the earlier part on sources of development.

You may see that the pandemic assist from Authorities clearly allowed the non-public home sector to rebuild its saving buffers and scale back the precarity of its stability sheet (given the large family debt).

Within the ancient times, previous to the GFC, the credit score binge within the non-public home sector was the one motive the federal government was in a position to report fiscal surpluses and nonetheless take pleasure in actual GDP development.

However the family sector, particularly, gathered report ranges of (unsustainable) debt (that family saving ratio went destructive on this interval although traditionally it has been someplace between 10 and 15 per cent of disposable earnings).

The fiscal stimulus in 2008-09 noticed the fiscal stability return to the place it must be – in deficit – given the nation’s exterior deficit place.

This not solely supported development but in addition allowed the non-public home sector to begin the method of rebalancing its precarious debt place.

You may see the purple line strikes into surplus or near it.

That course of was interrupted by the renewal of the fiscal surplus obsession in 2012-13.

The robust fiscal assist through the pandemic overwhelmed all of the nonsensical deficit scaremongering and allowed the non-public home sector to extend its total saving (and pay down debt) which was a great factor.

However because the earlier authorities withdrew its stimulus and the present authorities continued to pursue a contractionary fiscal place (see above), the non-public home sector has just one possibility given the traits within the exterior sector if it needs to keep up consumption expenditure – resume the method of accumulating extra debt.

With a world recession threatening and with increased rates of interest the norm, the technique outlined within the Authorities’s fiscal assertion is as soon as once more inserting the economic system on an unsustainable path counting on family debt accumulation, which is a finite course of.

Conclusion

There are various different elements to the present fiscal stance which I might talk about if I had extra time.

Basically, I’m unimpressed.

That’s sufficient for at the moment!

(c) Copyright 2026 William Mitchell. All Rights Reserved.