In some respects, we’re again to the place we had been in 2021 when the availability constraints that arose from the COVID lockdowns and widespread sicknesses began to disclose themselves in escalating costs all over the world. This time it’s the US-Israel folly within the Center East that’s the perpetrator and the availability constraints are largely confined to power, particularly oil (and its by-product merchandise). And just like the COVID inflation, the present inflationary pressures will show to be transitory and can dissipate as quickly as Trump will get bored and decrees his folly is over. It’s irresponsible to regulate financial coverage, which may have long-term penalties, to cope with a short-term blip, particularly when the causes of that blip usually are not delicate to rate of interest adjustments. When the RBA hiked rates of interest once more they knew they might not justify it based mostly on the power value rises. Everybody is aware of these value rises are short-term. So the RBA resorted to “capability constraints” and ‘rising expectations’ to justify their motion but supplied no sturdy proof to help these assertions. It was ideology triumphing over motive. Simply what now we have come to count on from our central financial institution.

On Tuesday (Might 5, 2026), the Reserve Financial institution of Australia (RBA) elevated rates of interest once more – the third time this yr.

Within the media launch accompanying the choice – Assertion by the Financial Coverage Board: Financial Coverage Determination – the RBA sought to justify the rise with an extra demand narrative – “capability pressures” and claimed that the rising rates of interest will imply that:

… demand development slows and capability pressures ease …

The RBA additionally rehearsed the mainstream ‘inflationary expectations’ argument that claims that rising inflation turns into in-built to the choice making of companies and households, which then turns into a self-fulfilling dynamic impartial of the unique causes of the rising costs.

The story then goes {that a} sharp downturn in demand is required to expel these expectations from the system.

That is Milton Friedman model XXX.

It’s a pity that this nonsense nonetheless has foreign money in central banking and is used as a smokescreen for his or her irresponsible determination making.

In 2021, the Board of Governors on the Federal Reserve Board, Washington, D.C. printed a analysis paper – Why Do We Suppose That Inflation Expectations Matter for Inflation? (And Ought to We?) – (a part of the Finance and Economics Dialogue Sequence 2021-062), which was written by a senior advisor to the Financial institution, one Jeremy B. Rudd.

Jeremy Rudd is an economist on the Board of Governors of the Federal Reserve System within the US, and, beforehand held senior positions with the US Treasury Division and served on the Council of Financial Advisors for a number of years.

His paper presents a frontal assault of the mainstream concept that inflation turns into self-fulfilling by way of rising inflationary expectations.

The opening paragraphs inform us of the intent:

Mainstream economics is replete with concepts that “everybody is aware of” to be true, however which might be really arrant nonsense …

None of those propositions has any type of empirical basis; furthermore, every one seems to be significantly poor on theoretical grounds … However, economists proceed to depend on these and comparable concepts to prepare their occupied with real-world financial phenomena.

That may be a good begin.

He then launches into the present central financial institution orthodoxy that was as soon as once more rehearsed by the RBA governor on Tuesday when she was attempting to justify the unjustifiable – mountaineering rates of interest to move off a supply-side phenomenon, the place the important thing drivers are by no means delicate to Australian home rate of interest variations:

I look at one such thought, specifically, that anticipated inflation is a key determinant of precise inflation. Many economists view expectations as central to the inflation course of; equally, many central banks think about “anchoring” or “managing” the general public’s inflation expectations to be an essential coverage aim or instrument. Right here, I argue that utilizing inflation expectations to elucidate noticed inflation dynamics is pointless and unsound: pointless as a result of an alternate rationalization exists that’s equally if no more believable, and unsound as a result of invoking an expectations channel has no compelling theoretical or empirical foundation and will doubtlessly lead to severe coverage errors.

He invokes a basic quote from the 1946 basic by J.R. Hicks – Worth and Capital (printed by Oxford College Press):

Pure economics has a outstanding manner of pulling rabbits out of a hat — apparently a priori propositions which apparently confer with actuality. It’s fascinating to attempt to uncover how the rabbits bought in; for these of us who don’t consider in magic have to be satisfied that they bought in one way or the other.

The dominant mainstream macroeconomic theoretical framework – New Keynesian economics – locations the concept the hyperlink between the actual financial system (exercise – output, employment and so on) and inflation is intrinsically linked by way of worth expectations shaped by decision-making ‘brokers’ (as people are known as within the fashions).

The theoretical help for this strategy is weak, to say the least and I gained’t rehearse them right here.

I’ve many weblog posts from the previous the place I focus on the restrictions, for instance – Mainstream macroeconomic fads – only a waste of time (September 18, 2009).

Apparently, one of many early architects of what has change into New Keynesian macroeconomics – Leonard Rapping – completely rejected his earlier work and accused governments of following the concepts in his earlier work of facilitating “transfers cash from the poor to the wealthy” (Supply).

He was a College of Chicago graduate (Milton Friedman’s affect) and his early work was with Robert Lucas Jnr, who was given the Nobel Prize in 1995 “for having developed and utilized the speculation of rational expectations, and thereby having remodeled macroeconomic evaluation and deepened our understanding of financial coverage.”

RATEX as it’s identified posits that everybody understands the true underlying financial mannequin and that on common now we have good foresight consequently (our forecasting errors have a zero imply).

The truth that such nonsense is definitely a core a part of the mainstream principle must be ample for any severe minded individual to reject such economics outright.

Leonard Rapping was interviewed for Arjo Klamer’s guide “The New Classical Macroeconomics” Wheatsheaf Books, 1984.

On methodology, Rapping says of his Chicago days:

… we had been within the Chicago custom, so we assumed good competitors and revenue and utility maximisation. Each single proposition needed to be in line with these assumptions. There have been sure guidelines of logic that needed to be adopted, and the discussions had been very tight and logical. We’d attempt to clarify every part when it comes to the aggressive equilibrium fashions. (We had realized that from Friedman) …

Someday later, Rapping turned extraordinarily disillusioned with the Vietnam Struggle and noticed that the logic of the warfare clashed with the coaching he had obtained at Chicago, and was, in flip, passing on to college students himself. He mentioned:

I found that the warfare was mistaken: I got here to the conclusion that it was an illegitimate warfare and America was an imperial energy. That disillusioned me. In all my coaching at Chicago there was no severe point out of the worldwide system. Chicago coaching, like coaching elsewhere, was closed financial system coaching. I knew that the Chicago world imaginative and prescient was inappropriate for the issues I used to be involved with … You can’t have democracy at dwelling and an empire overseas … Friedman by no means talked about something about overseas coverage or protection spending or an American system. So I did the one factor I may: I jettisoned Chicago economics …

This led Rapping to initially abandon his burgeoning profession as one on the forefront of mainstream neoclassical considering at Carnegie-Mellon College (Pittsburgh).

He later turned to radical economics and took a publish at Umass (Amherst).

It was a serious change in his thought processes and I at all times had quite a lot of respect for the braveness he demonstrated going head-to-head in opposition to the mainstream bully boys (largely males).

He was very essential of Ronald Reagan’s pursuit of supply-side economics.

I had an interchange some years in the past with Arjo Klamer about Rapping once I was within the Netherlands, which recommended he didn’t die all that completely satisfied.

Anyway, as soon as he had made the transition his views on the work of Lucas and the rational expectations custom modified considerably.

Klamer requested him: “What do you concentrate on the present work of Bob Lucas?” He replied:

It is vitally summary and formal mannequin constructing … For me it’s too normal, too faraway from actuality.

Additional on within the interview (p.234), Rapping mentioned that:

Frankly, I don’t assume that the rational expectations theorists are in the actual world … Folks skilled in his manner …[Lucas] … of considering can be utilized mathematicians. Of-course, these individuals won’t be satisfied that much less “exact” methods of considering are applicable. So what? Many of the economists who choose up these things are younger; the older economists haven’t embraced it. The youthful ones could drive the broad thinkers some place else, wish to political science or sociology or regulation. That bothers me about American economics.

Jeremy Rudd wrote that whereas the idea supporting the ‘expectations’ declare is weak:

… the direct proof for an anticipated inflation channel was by no means very sturdy … the varied theoretical fashions that assumed a task for anticipated inflation tended to hold different empirical implications that had been clearly at variance with the information … the documented empirical deficiencies of the new-Keynesian Phillips curve are legion.

A lot of my earlier econometric work was on this subject and the empirical help for the mainstream inflation mannequin was very arduous to generate – all kinds of fudges had been wanted within the specification of the equations to get something like an affordable ‘match’ to the information.

Largely, the outcomes of the statistical work had been at odds with the idea.

Jeremy Rudd additionally utilized some frequent sense and mentioned that impartial of the econometric failures, it simply doesn’t make sense that enterprise companies, that are setting costs within the present interval to fulfill anticipated demand circumstances and likewise are ready to face by these costs to exhibit loyalty to prospects, would out of the blue push up costs as a result of they thought costs could be larger sooner or later.

He wrote:

What little we learn about companies’ price-setting conduct means that many have a tendency to reply to value will increase solely once they really present up and are seen to their prospects, slightly than in a preemptive style …

Whereas the idea and makes an attempt to offer evidential help for the idea that inflationary expectations drive the inflation course of have largely failed, central banks nonetheless parrot the idea as whether it is sacrosanct and past accountability.

Within the Financial Coverage assertion on Tuesday (hyperlink above), the RBA claimed:

Quick-term measures of inflation expectations have additionally risen.

Have they certainly?

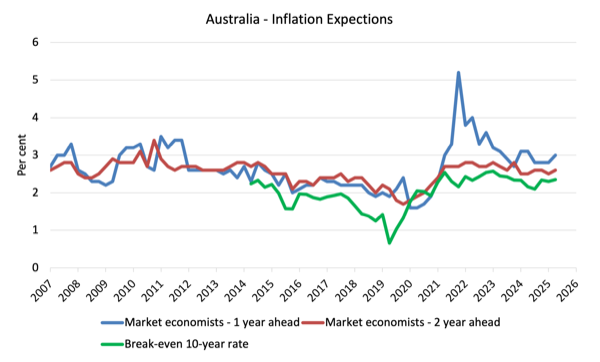

The next graph exhibits three measures of anticipated inflation produced by the RBA from the December-quarter 2005 to the March-quarter 2026.

The 4 measures are:

1. Market economists’ inflation expectations – 1-year forward.

2. Market economists’ inflation expectations – 2-year forward – so what they assume inflation can be in 2 years time.

3. Break-even 10-year inflation price – The typical annual inflation price implied by the distinction between 10-year nominal bond yield and 10-year inflation listed bond yield. It is a measure of the market sentiment to inflation threat. That is thought-about essentially the most dependable indicator.

They beforehand printed a fourth measure – Union officers’ inflation expectations – 2-year forward – however this collection hasn’t been up to date for the reason that September-quarter 2023.

However the systematic errors within the forecasts, the worth expectations (as measured by these collection) are all nicely inside the RBA’s targetting vary of 2-3 per cent.

Not one of the time collection are accelerating upwards at any important price.

The proof demonstrates that there isn’t any foundation for the RBA’s declare that worth expectations are rising.

The shifts are all inside survey sampling errors.

The newest information is proven within the following graph:

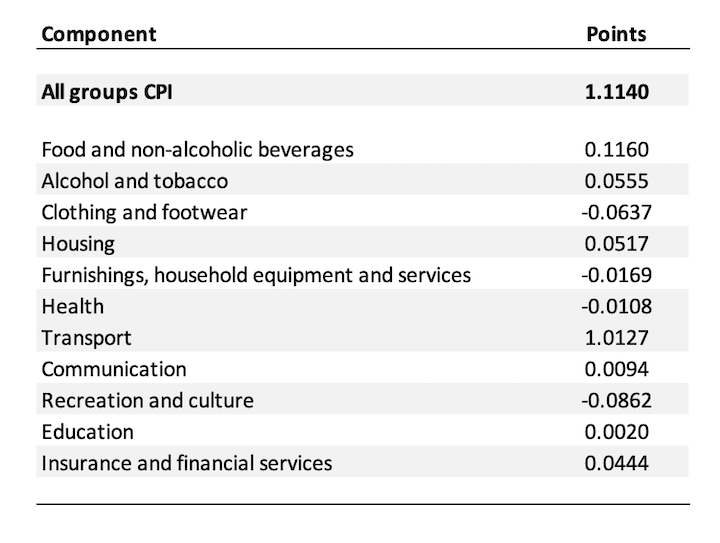

The next desk exhibits the contributing components (in factors) to the March All teams CPI inflation consequence.

I’ve aggregated the sub-components into the highest stage gadgets:

The outcomes are clear:

The outcomes are clear:

1. The All teams CPI rose by 1.1 per cent in March – which is sort of important.

2. Transport contributed 1.01 factors – all personal motoring.

That’s, imported gasoline prices have risen quickly on account of the chaos Trump and Netanyahu are inflicting within the Center East.

3. Meals and Alcoholic drinks contributed 0.11 factors.

4. Most practically each different element within the CPI routine demonstrated no important contribution or had been detrimental.

Then ask the query:

How will growing home rates of interest do something to cut back the worth of petrol in Australia when the oil and refined merchandise are imported and the prices are being pushed by an exterior warfare?

The reply is clear and the RBA is aware of that it’s apparent.

That’s the reason they’re dodging the difficulty and making spurious claims about “capability points” and “rising expectations” to divert our consideration from the plain.

On the capability subject – in March 2026, the official unemployment price was 4.3 per cent and the underemployment price was 5.9 per cent, given a complete wastage of prepared and obtainable labour of 10.2 per cent.

Along with the detailed CPI information (which may have revealed particular bottlenecks), the truth that there’s that a lot idle labour tells us that the capability subject (an excessive amount of spending) can also be spurious.

The ultimate subject pertains to fiscal coverage.

On the RBA’s press convention on Tuesday saying the – Financial Coverage Determination – the Governor mentioned that:

… when governments are spending some huge cash and we’re working up in opposition to capability constraints, then they do want to consider whether or not or not there’s methods they can assist the inflation drawback by in search of methods to constrain demand.

Subsequent week, the Treasurer will ship his annual fiscal assertion outlining spending and tax initiatives for 2026-27.

A lot must be completed to enhance public infrastructure, restore some credibility to the training system (significantly larger within the wake of latest scandals), cope with the housing disaster, cope with local weather change and all the opposite issues which might be degraded or deteriorating due to years of austerity-minded coverage making.

However the Treasurer is aware of that the RBA Board is stacked filled with New Keynesians who leap at shadows and name them ‘capability constraints’ or ‘unanchored inflationary expectations’ and drive up rates of interest.

So he’s caught on this continual dysfunction as nicely – which is partly of his personal making given he’s the one who makes appointments to the RBA administration and coverage board.

He is aware of that if he tries to cope with the short-term cost-of-living pressure led to by the Center East chaos, the RBA will simply worsen the issue by pushing charges up once more.

Consequently, whereas financial coverage is inflicting harm and redistributing earnings from the low-income debt holders to the high-income holder of monetary property and the financial institution shareholders, fiscal coverage is being prevented from aiding the low-income households who’re most uncovered to rising transport prices.

So each arms of coverage are perverted by this most cancers – New Keynesian ideology.

Conclusion

One thing has to provide.

That’s sufficient for at the moment!

(c) Copyright 2026 William Mitchell. All Rights Reserved.