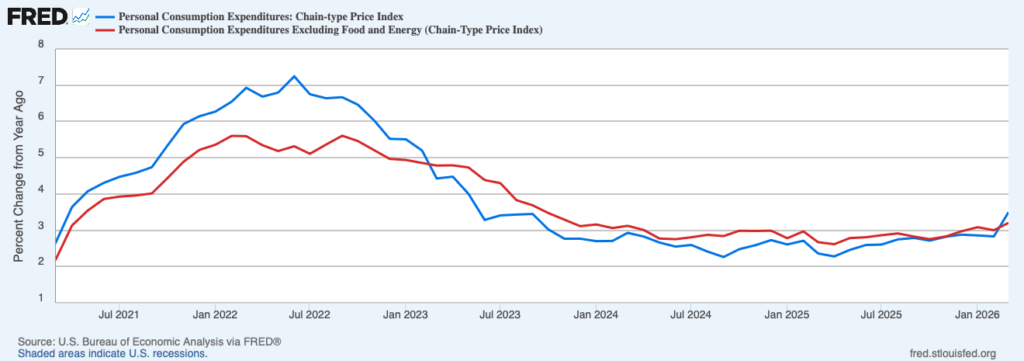

Nobody can be stunned to listen to that inflation has picked up. However new knowledge from the Bureau of Financial Evaluation confirms it. The Private Consumption Expenditures Worth Index (PCEPI), which is the Federal Reserve’s most well-liked measure of inflation, grew at an annualized price of 8.3 p.c in March 2026, up from 4.6 p.c within the prior month. The PCEPI grew at an annualized price of 5.6 p.c during the last six months and three.5 p.c during the last 12 months.

A lot of the noticed enhance during the last two months is said to the continuing battle within the Center East, which has pushed up vitality costs. The worth index for vitality items and providers grew 11.6 p.c in March — or 271.8 p.c annualized. The worth of vitality has grown 14.4 p.c during the last 12 months.

Excessive inflation shouldn’t be restricted to the vitality sector, nonetheless. Core inflation, which excludes meals and vitality costs and is regarded as a greater gauge of the underlying price of inflation, stays properly above the Fed’s longer-run goal. Core PCEPI grew at an annualized price of three.6 p.c in March 2026. It grew at an annualized price of three.7 p.c during the last six months and three.2 p.c during the last 12 months.

AIER’s Financial Neutrality Report, launched this morning, identifies the first driver of the broader inflation downside: extra nominal spending development.

Milton Friedman taught us that “Inflation is at all times and all over the place a financial phenomenon within the sense that it’s and might be produced solely by a extra speedy enhance within the amount of cash than in output.” When the amount of cash being spent in an financial system grows quicker than actual output, costs should rise. And when a rise in nominal spending development shouldn’t be matched by a rise in actual output development, costs should rise extra quickly. A surge in nominal spending development, subsequently, tends to supply greater inflation.

Nominal spending has surged during the last 12 months. It grew 5.4 p.c from 2024:This autumn to 2025:This autumn. It grew at an annualized price of 5.6 p.c in 2026:Q1. For comparability, nominal spending grew at a median annualized price of 4.1 p.c over the 5 years simply previous to the pandemic. If actual GDP development averages 2.5 p.c, nominal spending development would want to common round 4.5 p.c for the Fed to hit its two-percent inflation goal. Therefore, at 5.6 p.c, nominal spending is rising about 1.1 share factors quicker than the Fed would really like.

Taken collectively, the out there proof suggests inflation is excessive for 2 distinct causes: the continuing battle within the Center East, which disproportionately impacts vitality costs, and broader inflationary pressures associated to extra nominal spending. The vitality worth hikes are momentary, with vitality costs returning to regular when the battle ends and manufacturing resumes. However the broader inflationary pressures associated to extra nominal spending indicate that the Federal Reserve nonetheless has some work to do.

Sadly, many Fed officers have been sluggish to acknowledge the broader inflationary pressures. They blame the battle within the Center East and, earlier than that, tariffs for the uptick in inflation.

On the post-meeting press convention earlier this week, Fed Chair Jerome Powell acknowledged that “Inflation has moved up not too long ago and is elevated relative to our two-percent, longer-run purpose.” He mentioned the rise in headline inflation was on account of “the numerous rise in world oil costs that has resulted from the battle within the Center East,” whereas the excessive core inflation “largely displays the consequences of tariffs on costs within the items sector.”

The view that tariffs have had a significant impact on inflation is tough to sq. with the information. Tariffs have an effect on relative costs, to make sure. A ten p.c tariff on vehicles will have a tendency to boost the value of vehicles relative to every part else. However tariffs enhance inflation solely insofar as they scale back actual output development. However actual output development has been sturdy. Actual GDP grew 2.7 p.c during the last 12 months. For comparability, actual GDP development averaged 2.6 p.c per 12 months over the 5 years simply previous to the pandemic.

Wanting forward, Powell described the financial outlook as “extremely unsure” and mentioned that “the battle within the Center East has added to this uncertainty.” He expects “greater vitality costs will push up total inflation” within the close to time period, however mentioned “the scope and period of potential results on the financial system stay unclear, as does the longer term course of the battle itself.”

Notably absent from Powell’s remarks is any concern that nominal spending is rising too quickly. That is particularly worrisome given current Fed errors.

Within the again half of 2021, Fed officers believed rising inflation was primarily on account of pandemic-related provide disruptions, despite the fact that the incoming knowledge instructed in any other case. Actual GDP had largely recovered. However, somewhat than returning to development, costs accelerated. Nonetheless, Fed officers clung to the assumption that the excessive inflation was transitory. And, even after they dropped the phrase transitory and appeared to acknowledge the surplus nominal spending downside, they delayed tightening financial coverage. The consequence was the worst inflationary episode in forty years.

Now, the Fed dangers repeating that mistake. On this case, Powell is correct that provide disruptions are pushing up costs. However that’s solely a part of the story. The opposite half — and the half that financial coverage is best-suited to deal with — is the surplus nominal spending, which has largely gone unnoticed.

There’s one key distinction between then and now, nonetheless. This time round, no less than some Fed officers are genuinely involved about excessive inflation, a lot in order that they broke ranks with the remaining. Three regional Reserve Financial institution presidents — Beth Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorie Logan (Dallas) — dissented at this week’s assembly, preferring to take away the easing bias within the FOMC’s post-meeting assertion. They might want to persuade their colleagues that the excessive inflation is broader and extra persistent than what all of us can see clearly on the pump, and take steps to scale back nominal spending development.