Debt balances continued to march upward within the second quarter of 2025, in accordance with the most recent Quarterly Report on Family Debt and Credit score from the New York Fed’s Middle for Microeconomic Information. Mortgage balances specifically noticed a rise of $131 billion. Following a steep rise in house costs since 2019, a number of housing markets have seen dips in costs and considerations have been sparked concerning the state of the mortgage market. Right here, we disaggregate mortgage balances and delinquency charges by sort and area to higher perceive the panorama of the present mortgage market, the place any ongoing dangers could lie, regionally and by product.

Notice: The Quarterly Report and this evaluation are based mostly on the New York Fed Shopper Credit score Panel, which is drawn from anonymized Equifax credit score reviews.

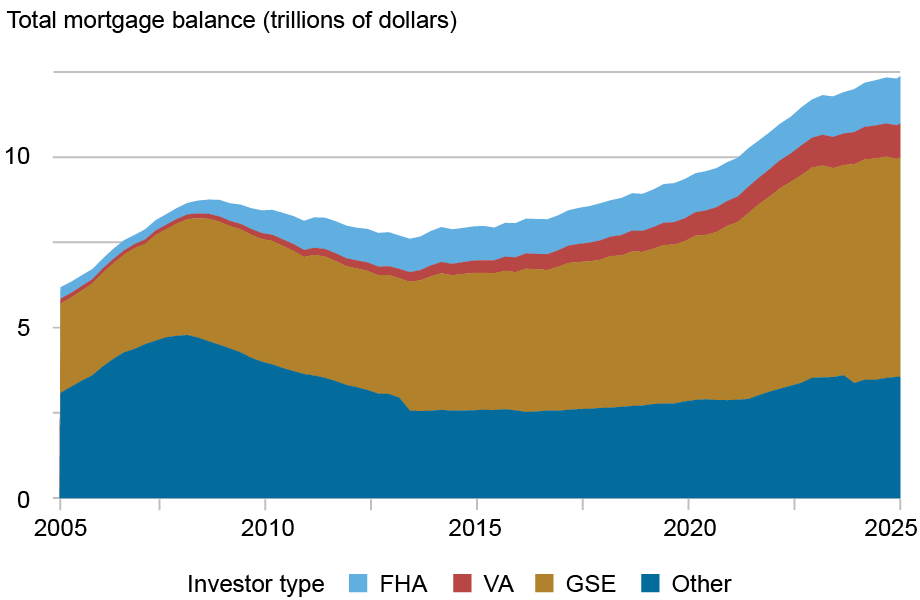

Mortgage Steadiness Composition

As of June 2025, complete excellent mortgage balances in america stood at $12.94 trillion. Loans securitized by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac proceed to dominate the market, comprising round 52 % of all balances at roughly $6.5 trillion. Authorities-backed loans, equivalent to these insured by the Federal Housing Administration (FHA) or Division of Veterans Affairs (VA), account for 19 % or $2.5 trillion. FHA loans are designed for first-time and lower-income patrons and make up 12 % of balances, whereas VA loans which are accessible to U.S. army veterans comprise 8 %.

Mortgage Balances Proceed to Climb

The composition of complete mortgage balances by sort has stayed largely steady since 2019. Different loans, proven in teal within the chart beneath, are comprised by a mix of loans, together with loans held on financial institution portfolios in addition to non-public label securitized loans. The more moderen cross-section of “different” loans could be overwhelmingly portfolio loans, significantly jumbo loans that can not be offered to the GSEs. The majority of the loans within the “different” class within the earlier cross sections of the chart would seemingly have been comprised of the big quantity of subprime loans that had been securitized on the non-public market.

Complete Mortgage Steadiness Excellent by Investor Kind

Notice: Different consists of mortgages held on portfolio, non-public label securities, and in any other case unnarrated loans.

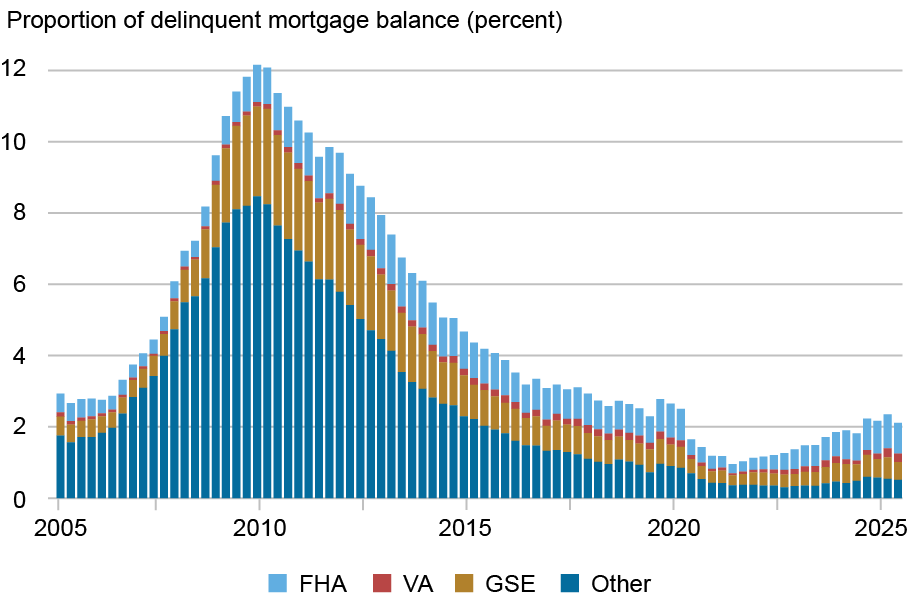

New Delinquencies

Mortgage delinquency charges have risen modestly general, though they continue to be low by historic requirements. Nonetheless, once we cut up mortgage balances by their underlying investor varieties, we notice substantial heterogeneity. FHA loans, proven in blue within the chart beneath, have traditionally had larger delinquency charges—as an end result of their mission to develop homeownership to new householders. These mortgages have not too long ago seen the steepest rise in delinquency charges, with transitions into 30 days overdue exceeding 4 % quarterly. In a means, the present larger circulation delinquency charges are offsetting the artificially low circulation delinquency charges in the course of the pandemic.

Quarterly New Delinquencies Have Risen Amongst FHA Mortgages however Stay Low and Secure for Different Sorts

Transition into delinquency (%)

Notice: 4-quarter shifting common.

FHA Mortgages Comprise a Disproportionately Massive Share of Delinquent Balances in 2025:Q2

We subsequent contemplate the precise greenback share of mortgages which are delinquent damaged out by mortgage sort. Presently, 2.1 % of mortgage balances are 30 or extra days overdue, which is barely beneath pre-pandemic ranges in 2019:Q1. In 2025:Q2, GSE loans make up greater than half of all mortgage debt, however lower than 1 / 4 of delinquent mortgages. Alternatively, FHA loans make up 38 % of 30+ day delinquent balances regardless of constituting solely 12 % of complete balances. It is a bigger proportion of delinquent balances in comparison with earlier than the pandemic, when FHA loans made up solely 30.5 % of delinquent balances in 2019:Q1. A have a look at the historic knowledge reveals that the markedly elevated ranges noticed within the teal bars previous to 2010 within the chart above align with the predominance of subprime and Alt-A mortgages in that class.

High quality of Newly Originated Mortgages Stays Stable, Even Amongst FHA Debtors

Imply origination credit score rating, annual

Mortgage underwriting requirements remained strict and common credit score scores remained close to historic highs even in the course of the surge in homebuying within the pandemic-era. Credit score scores at origination for GSE and different loans are the very best of all mortgage varieties and stay elevated at a median of 774. FHA loans, which usually have decrease credit score scores at origination, are exhibiting common credit score scores of recent debtors round 700. This rating is close to long-term highs, at the same time as house costs and demand have surged upward over the previous 5 years.

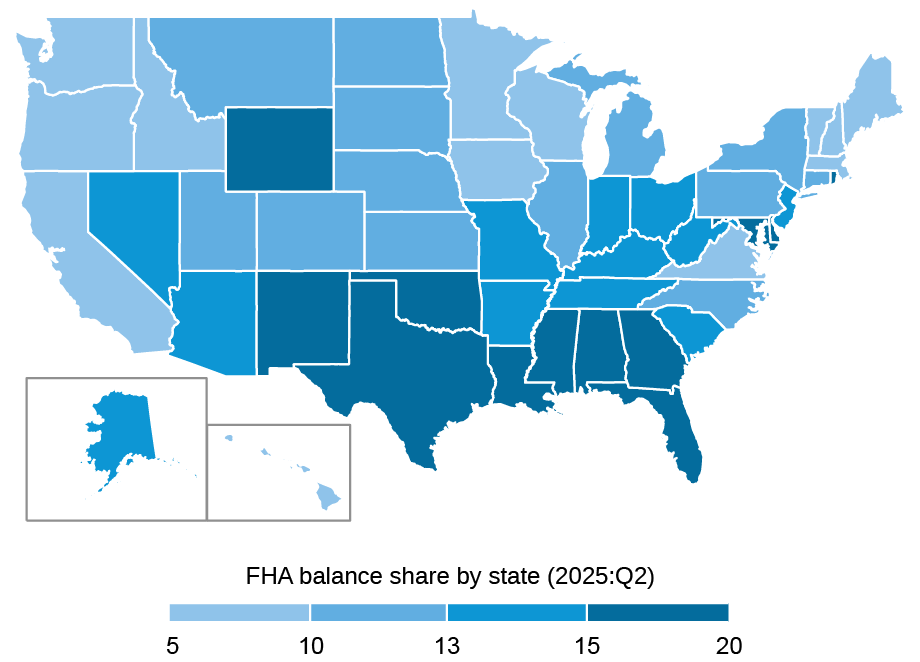

The place Are the FHA Debtors?

geographic concentrations of loans, current knowledge point out {that a} larger proportion of mortgage balances are delinquent in lots of the southern states and Puerto Rico. We additionally notice {that a} larger proportion of mortgage balances are FHA loans within the southern states. Notably, about 20 % of mortgage balances in Oklahoma, Mississippi, and Puerto Rico are FHA loans, nearly double the nationwide common of 11 %. Traditionally, we see that larger delinquency charges coincide with a better share of FHA loans throughout states.

FHA Mortgages Are Extra Concentrated within the Southeast

Conclusion

The image of the U.S. mortgage market could be very completely different as we speak than it was in 2008, when a considerable portion of excellent mortgage balances consisted of non-GSE mortgages. These mortgages have been significantly susceptible to default, and delinquency charges surged after house costs started to say no. This was largely resulting from their decrease credit score high quality and better loan-to-value ratios, amongst different elements. Against this, as we speak’s mortgage panorama is marked by extra prudent lending practices, and credit score high quality has improved. The common credit score rating for mortgages at origination in 2025 was 22 factors larger amongst GSE loans in comparison with 2008, and FHA loans have been 38 factors larger. Additional, exterior of FHA, mortgages typically require decrease loan-to-value ratios.

This longer-term enchancment in high quality has resulted in decrease delinquency charges. Whereas house costs have solely declined barely, there’s some threat {that a} continued decline in house costs could add stress ought to extra debtors discover themselves underwater. A few of this stress could also be extra related amongst FHA debtors. FHA mortgage merchandise enable for a smaller down fee at origination. The weakening efficiency amongst these debtors could replicate rising monetary stress amid softening house costs, particularly contemplating the previous pandemic interval of artificially low delinquency charges.

Mortgages are a monetary instrument that has traditionally helped American households bridge into homeownership and to construct wealth, and the mortgage market stays the most important and most essential credit score marketplace for American households. The current uptick in mortgage delinquency appears to be concentrated amongst FHA debtors, nonetheless, mortgage efficiency stays very stable when seen in gentle of the twenty-year historical past of our knowledge. Nonetheless, with the weird dynamics of house costs within the final 5 years, many eyes are on mortgage efficiency, and we are going to proceed to observe this essential market.

Andrew F. Haughwout is deputy analysis director within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Donghoon Lee is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jonathan Lee is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Joelle Scally is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Wilbert van der Klaauw is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

cite this publish:

Andrew F. Haughwout, Donghoon Lee, Jonathan Lee, Joelle Scally, and Wilbert van der Klaauw, “A Test‑In on the Mortgage Market,” Federal Reserve Financial institution of New York Liberty Avenue Economics, August 5, 2025, https://libertystreeteconomics.newyorkfed.org/2025/08/a-check-in-on-the-mortgage-market/

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).