Latest pure disasters have renewed considerations about insurance coverage markets for pure catastrophe aid. In January 2025, wildfires wreaked havoc in residential areas exterior of Los Angeles. Direct injury estimates for the Los Angeles wildfires vary from $76 billion to $131 billion, with solely as much as $45 billion of insured losses (Li and Yu, 2025). On this submit, we look at the state of one other catastrophe insurance coverage market: the flood insurance coverage market. We evaluate options of flood insurance coverage mandates, flood insurance coverage take-up, and join this to work in a associated Employees Report that explores how mortgage lenders handle their publicity to flood threat. Mortgages are a transmission channel for financial coverage and likewise an vital monetary product for each banks and nonbank lenders that actively take part within the mortgage market.

Flood Damages and Insurance coverage Protection

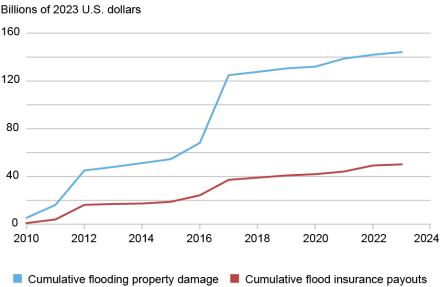

The U.S. has sustained substantial and largely uninsured damages from flooding over the previous fifteen years. The chart beneath shows the cumulative damages from flooding within the U.S. and the cumulative insurance coverage payouts on these damages, beginning in 2010. Between 2010 and 2023, the direct property injury from flooding totaled almost $144 billion (in 2023 USD). In the identical interval, insurance coverage funds on property injury from the Nationwide Flood Insurance coverage Program totaled roughly $50 billion (in 2023 USD)—simply 35 % of the direct damages. These injury estimates understate the total financial price of flooding by excluding oblique damages (for instance, misplaced revenue and manufacturing related to floods).

Cumulative Flood Damages and Insurance coverage Funds, 2010‑23

Notes: Each damages and insurance coverage funds thought-about are restricted to these within the fifty states and District of Columbia, excluding damages and claims in U.S. territories.

Insurance coverage Mandates

What does the flood insurance coverage market appear like and who has to buy flood insurance coverage? Flood insurance coverage within the U.S. is nearly solely offered by the Nationwide Flood Insurance coverage Program (NFIP), which is managed by the Federal Emergency Administration Company (FEMA). In its position administering the NFIP, FEMA designates particular areas with elevated flood threat, generally known as 100-year flood zones. A 100-year flood zone is a FEMA-designated space with an annual chance of experiencing a serious flood of a minimum of 1 % (that’s, a minimum of one main flood is predicted each 100 years). With little exception, flood insurance coverage is required to acquire a mortgage for a property in 100-year flood zones—areas that cowl roughly 5 % of residential properties.

Though these flood-prone areas are principally concentrated in coastal and riverine areas, smaller pockets exist throughout the nation. The chart beneath reveals the county-level proportion of properties lined by a 100-year flood zone for the contiguous states. Almost 20 % of all properties positioned in considered one of FEMA’s 100-year flood zones are positioned inside one mile of the coast, however the majority are positioned additional inland—roughly 60 % of properties inside a 100-year flood zone are positioned greater than ten miles from the coast.

County-Degree P.c of Properties in a 100-year Flood Zone

Corresponding with updates within the NFIP’s pricing construction, flood insurance coverage costs are on the rise. From 2009 to 2023, the imply annual price of a flood insurance coverage coverage for a single-family residence elevated by 82 %—a mean annual progress charge of roughly 4.4 %. On the similar time, flood insurance coverage protection has fallen. There have been almost 900,000 fewer lively flood insurance coverage insurance policies in 2023 than in 2009, an roughly 16 % drop over the interval.

Danger and Insurance coverage Take-Up

Regardless of the nearly necessary nature of flood insurance coverage inside a 100-year flood zone, most flood damages are usually not insured, partly due to the prevalence of flood threat exterior of official flood zones.

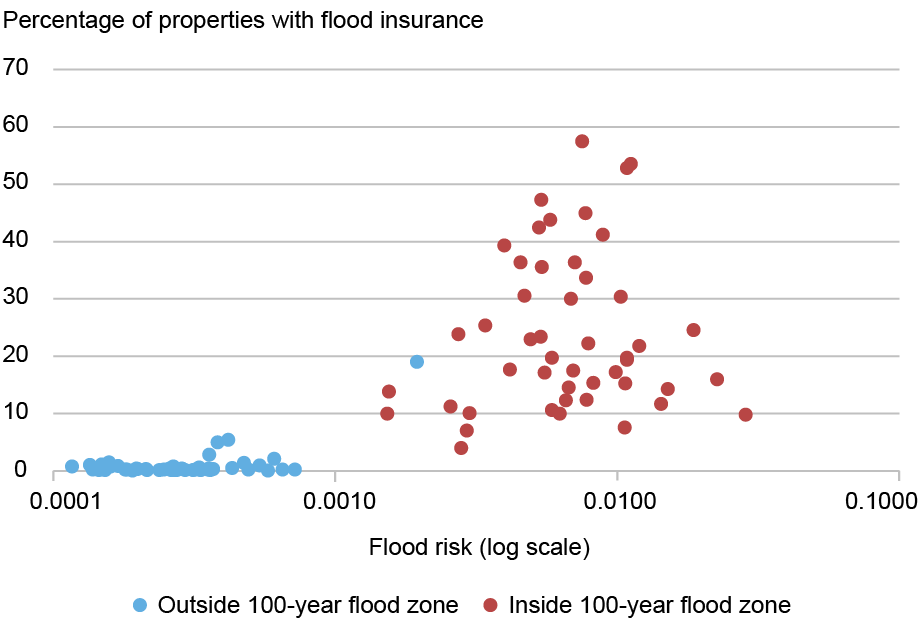

Properties exterior an official 100-year flood zone can nonetheless buy flood insurance coverage from the NFIP, however that is fairly uncommon in apply. Each underlying flood threat and the presence of a flood insurance coverage mandate are vital drivers of flood insurance coverage adoption. The chart beneath appears to be like on the relationship between flood threat, flood mandates, and flood insurance coverage adoption. For every of the contiguous forty-eight states, we compute the typical flood threat and flood insurance coverage take-up charges for properties inside a 100-year flood zone (crimson) and out of doors a 100-year flood zone (blue). Not all properties inside a 100-year flood zone have flood insurance coverage, both as a result of they don’t have a mortgage or as a result of they’ve fallen out of compliance. On common, properties in official flood zones are uncovered to excessive flood threat relative to properties exterior of official flood zones—the exception being Louisiana, the place even the typical property exterior of an official flood zone faces excessive flood threat. Additionally, flood insurance coverage is extra widespread in areas (1) the place the typical flood threat is excessive, and (2) topic to the insurance coverage mandate.

Flood Danger and Insurance coverage Take-Up, In and Out of Flood Zones

Notes: Some extent on the plot represents a state-flood zone mixture. Flood threat in a state-flood zone is computed because the unweighted imply of properties’ common annual loss (AAL) as a proportion of their insurable worth, as estimated by CoreLogic.

On the state-level, it’s troublesome to establish if flood zone designations have any significant influence on insurance coverage take-up or whether or not the upper insurance coverage take-up charges are pushed purely by greater flood threat. Utilizing extra granular knowledge in our personal evaluation, we discover a vital distinction in flood insurance coverage take-up throughout flood zones: a property exterior a 100-year flood zone is 15 share factors much less prone to have flood insurance coverage than a property inside a flood zone, even once we management for native measures of flood threat.

Implications for Mortgage Lending

What are the implications of uninsured flood threat for monetary intermediaries and the mortgage market? Within the related Employees Report, we discover to what extent mortgage lenders have responded to flood threat for loans secured by properties exterior an official flood zone. We discover that within the mixture, mortgage lenders are conscious of flood threat exterior of official flood zones. For example, mortgage lenders have decrease mortgage origination charges for properties with moderate-to-high flood threat exterior FEMA’s official flood zones, relative to in any other case comparable properties with low-to-no flood threat and likewise positioned exterior FEMA’s official flood zones. Not all lenders reply in the identical approach although. Massive banks have managed their publicity by lowering their originations whereas non-banks have executed so by promoting and securitizing these mortgages. In line with this truth, we doc greater progress charges for non-banks’ market share in high-flood threat census tracts than low-flood threat census tracts.

Ultimate Phrases

On this submit, we’ve emphasised that (1) substantial flood threat exists even for properties exterior of the mandated insurance coverage areas, and (2) there are vital variations in flood insurance coverage take-up between properties inside and out of doors the mandated insurance coverage areas. Mortgage lenders are conscious of this predominantly uninsured flood threat and have taken actions to handle their exposures.

Kristian Blickle is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Evan Perry, a former analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group, is a Ph.D. pupil in Environmental Economics at Yale College.

João A.C. Santos is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this submit:

Kristian S. Blickle, Evan Perry, and João A.C. Santos, “Flood Danger and Flood Insurance coverage,” Federal Reserve Financial institution of New York Liberty Avenue Economics, August 7, 2025, https://libertystreeteconomics.newyorkfed.org/2025/08/flood-risk-and-flood-insurance/

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).