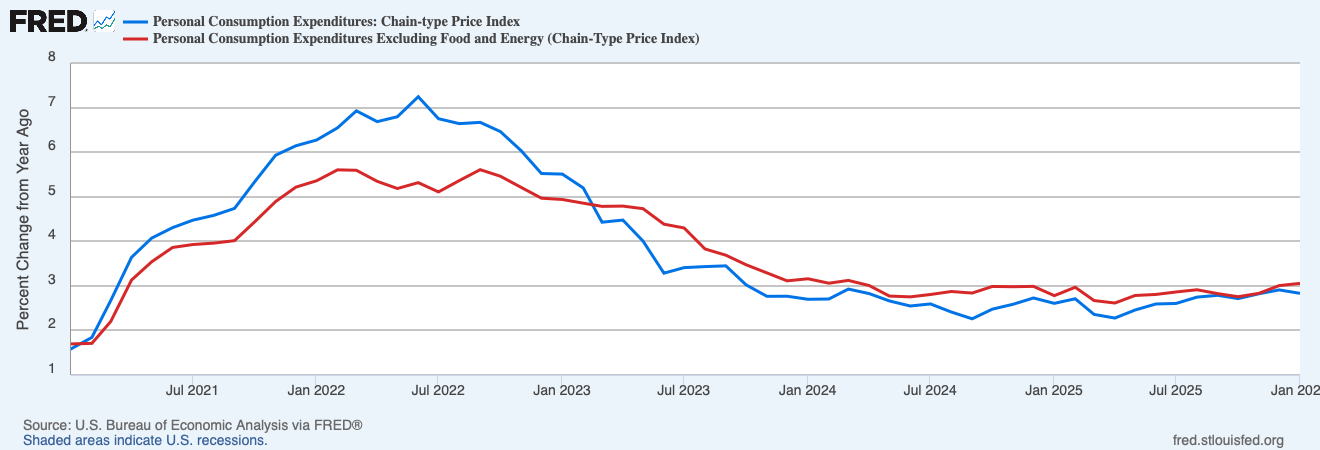

Inflation ticked down in January, the most recent information launched Friday from the Bureau of Financial Evaluation reveals. But it surely nonetheless stays nicely above the Federal Reserve’s goal. The Private Consumption Expenditures Worth Index (PCEPI), which is the Fed’s most well-liked measure of inflation, grew at an annualized fee of three.4 % in January 2026, down from 4.4 % within the final month of 2025. The PCEPI grew at an annualized fee of three.5 % over the prior three months and a pair of.8 % over the prior yr.

Core inflation, which excludes risky meals and power costs, remained elevated. Core PCEPI grew at an annualized fee of 4.5 % in January 2026. It grew at an annualized fee of three.7 % over the prior three months and three.1 % over the prior yr.

Breaking It Down

The traditional view is that tariffs have pushed up costs during the last yr. If that have been the case, we’d count on items costs to develop a lot quicker than companies costs. It’s simpler to import a hat than a haircut, and tariffs will typically trigger each overseas and home hat producers to boost their costs. Overseas hat producers increase their costs to cowl some portion of the tariff. Home hat producers increase their costs as a result of they know overseas hat producers will be unable to underbid them given the tariff.

Items costs grew at an annualized fee of 0.5 % in January, and have been up 1.3 % year-over-year. For comparability, items costs grew at a median annualized fee of -0.1 % per yr over the five-year interval simply previous to the pandemic. That means items costs have grown about 1.4 share factors quicker than traditional during the last yr.

Companies costs grew at an annualized fee of 4.6 % in January, and have grown 3.5 % during the last yr. Over the five-year interval simply previous to the pandemic, companies costs grew at a median annualized fee of two.3 % per yr. Therefore, companies costs have grown about 1.2 share factors quicker than traditional during the last yr. Furthermore, the surplus progress of companies costs can now not be defined by the housing part, which tends to lag broader worth actions. Housing costs grew 3.2 % during the last yr, which is round 10 foundation factors slower than noticed over the five-year interval simply previous to the pandemic.

Though items costs have grown a bit quicker than companies costs, the distinction — simply 20 foundation factors — is comparatively small. Recall that headline PCEPI inflation is round 80 foundation factors above the Fed’s two-percent objective. The accessible proof means that inflation is comparatively widespread. It’s not primarily as a result of tariffs.

Competing Targets

Elevated inflation is simply one of many considerations Fed officers will probably be discussing at this week’s Federal Open Market Committee assembly. They’re additionally involved concerning the comparatively gradual job progress noticed during the last yr.

“There isn’t any dismissing the weak spot of job creation in 2025,” Fed Governor Christopher Waller mentioned final month. Knowledge launched since then would appear to verify his fears that the robust January “report could comprise extra noise than sign.” The financial system misplaced 92,000 jobs in February, almost wiping out the outsized good points in January.

Congress has tasked the Fed with delivering worth stability and most employment. But it surely has largely left it to the Fed to find out what these phrases imply and find out how to steadiness the 2 targets when they’re in battle.

The Fed explains the way it will take care of diverging targets in its 2025 Assertion on Longer-Run Objectives and Financial Coverage Technique:

The Committee’s employment and inflation aims are typically complementary. Nevertheless, if the Committee judges that the aims usually are not complementary, it follows a balanced strategy in selling them, making an allowance for the extent of exits from its targets and the possibly completely different time horizons over which employment and inflation are projected to return to ranges judged in step with its mandate. The Committee acknowledges that employment could at instances run above real-time assessments of most employment with out essentially creating dangers to cost stability.

The so-called “balanced strategy” would appear to counsel it is going to place equal weight on the 2 targets. However the “extent of exits” and “completely different time horizons” affords a number of flexibility. And the particular consideration given to employment within the final line suggests the Fed would possibly put extra weight on employment in observe.

What Ought to Be Carried out?

My very own view is that the financial system is at or close to full employment in the meanwhile, with low job progress reflecting demographic modifications and elevated immigration enforcement. If I’m appropriate, the Fed shouldn’t fear concerning the labor market. As an alternative, it ought to give attention to getting inflation again down to focus on. The Iran battle could complicate the Fed’s job, by including short-term supply-driven inflation (which it ought to ignore) to the everlasting demand-driven inflation seen within the January launch (which it ought to deal with). If supply-driven inflation emerges, and I think it is going to, the Fed might want to parse the info fastidiously in an effort to decide the extent of the inflation drawback and, correspondingly, the extent to which it ought to reply to above-target inflation.

It’s extremely unlikely that Fed officers will modify their coverage fee on Wednesday. The CME Group at the moment places the chances at simply 0.9 %. However one ought to pay shut consideration to what Fed officers sign of their post-meeting assertion and what Chair Powell tells the press. That will give us a greater sense of how Fed officers are decoding the incoming information — and what they intend to do about it.