Understanding how short- and long-term property are priced is likely one of the elementary questions in finance. The time period construction of threat premia permits us to carry out internet current worth calculations, take a look at asset pricing fashions, and doubtlessly clarify the sources of many cross-sectional asset pricing anomalies. On this publish, I assemble a forward-looking estimate of the time period construction of threat premia within the company bond market following Jankauskas (2024). The U.S. company bond market is a perfect laboratory for finding out the connection between threat premia and maturity due to its massive measurement (standing at roughly $16 trillion as of the top of 2024) and since the maturities are properly outlined (in distinction to equities).

Extracting Threat Premia from Yields

The forward-looking nature of yields, mixed with the wealthy literature on anticipated default possibilities (Campbell, Hilscher, and Szilagyi [2008]; Feldhütter and Schaefer [2018]), permits us to extract anticipated returns with out counting on historic worth info. This characteristic offers highly effective empirical benefits as a result of in brief historic samples realized returns could also be pushed by a number of recessionary durations (for instance, the International Monetary Disaster), structural shifts within the risk-free fee, or time-variation in threat premia, thereby biasing estimates of short- and long-duration returns.

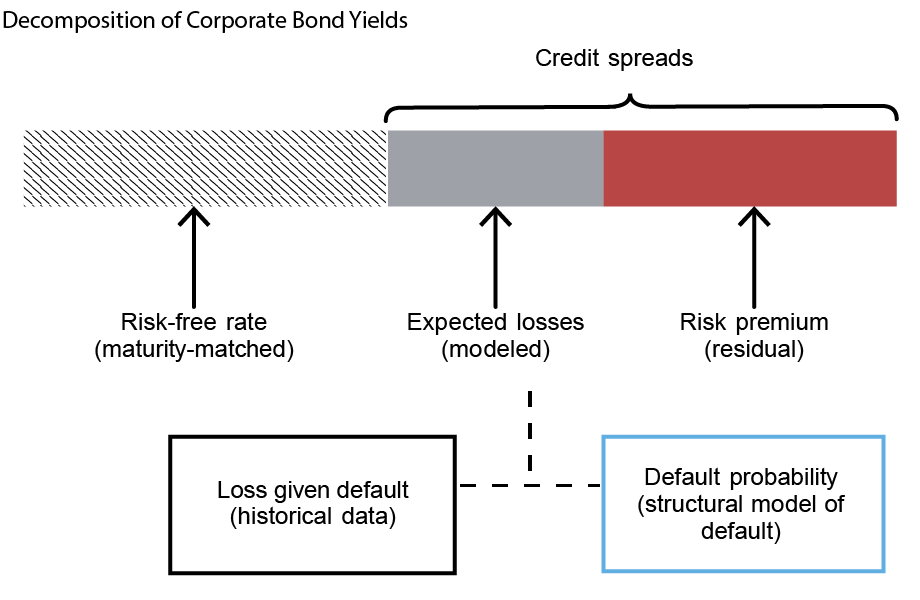

The important thing enter within the threat premium calculations is the anticipated default loss element. The company bond yield consists of three essential components, as depicted within the determine under: the maturity matched risk-free fee, anticipated default losses, and a threat premium. The latter two parts represent credit score spreads, that are instantly observable within the knowledge. The anticipated default element is estimated utilizing a structural mannequin of default following Feldhütter and Schaefer (2018), together with historic knowledge on loss given default. The benefit of utilizing a structural mannequin to assemble anticipated losses is that it offers ex-ante time-varying measures of threat premia for a variety of maturities and companies. The ensuing time-series and cross-sectional patterns can make clear how buyers worth various kinds of threat.

Period Varies Considerably Throughout Company Bonds

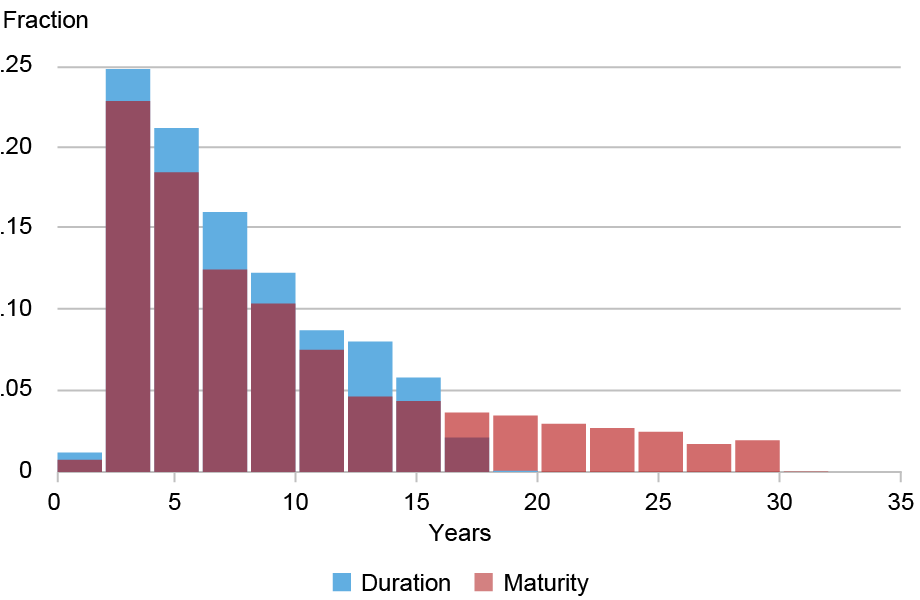

Company bonds show substantial variation in length, starting from only a few years to over fifteen years, as proven within the chart under. This length dispersion is helpful as a result of it permits for the development of duration-based bond portfolios that diversify idiosyncratic threat and isolate the results of length. I kind these portfolios as of June annually and preserve their composition mounted for a yr. The typical length of such portfolios is reported within the desk. The shortest-duration portfolios have a median length of just one to 2 years, whereas the longest-duration decile has a median length nearer to 14 years. These values function reference factors when referring to short- and long-duration threat premia within the subsequent evaluation.

Distribution of Bond-Month Observations Throughout Maturity and Period

Notes: The chart presents the distribution of the info pattern (2002-20) month-to-month observations by length and maturity. The length is measured utilizing the usual Macaulay length generally used within the company bond literature. Bonds with maturities lower than one yr or above thirty years are excluded. The darkish pink bars are the place the 2 histograms overlap.

Common Period in Period Deciles

| Low | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | Excessive | Excessive-Low |

|---|---|---|---|---|---|---|---|---|---|---|

| 1.3 | 2.4 | 3.4 | 4.2 | 5.1 | 6.0 | 7.1 | 8.8 | 11.5 | 14.1 | 12.7 |

Notes: The desk reviews the typical durations of company bonds within the knowledge pattern (2002-20) sorted every June into length deciles. Bonds with maturities lower than one yr or above thirty years are excluded.

The Slope of the Threat Premia Time period Construction

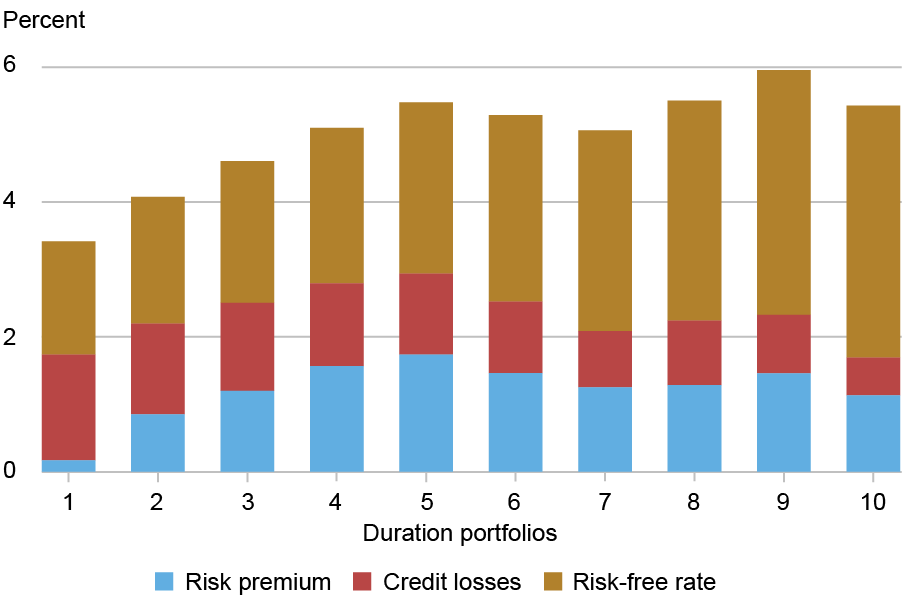

The following chart presents the decomposition of yields into the danger premium, credit score loss, and risk-free fee parts throughout the totally different length portfolios. The typical time period construction of yields is upward-sloping, with a lot of the slope concentrated between portfolios 1 and 5 and pushed primarily by the upward slope of the risk-free fee (depicted in gold). In distinction, the credit score spreads, that’s, the sum of the blue and pink areas, are considerably hump-shaped.

My evaluation decomposes the credit score spreads utilizing a structural default mannequin. The primary discovering is that the time period construction of the danger premium is upward sloping (depicted in blue). For the reason that common risk-free fee time period construction additionally has a optimistic slope, the full anticipated returns are strongly upward-sloping, yielding a time period premium of roughly 3.4 %. Most of this time period premium is pushed by the slope of the risk-free fee (2.1 %), however a considerable half comes from the slope of the danger premia (1.3 %). Importantly, the contribution of the danger premium is economically significant: it constitutes as much as 20 % of long-term bond yields, and as much as 30 % of whole anticipated returns (the sum of the risk-free fee and the danger premium). The optimistic threat premia slope is in line with classical behavior and long-run threat fashions, which hyperlink asset maturity to greater threat publicity.

Threat-Free Price and Threat Premium Time period Constructions Are Each Upward Sloping

Notes: The chart presents the typical yields, credit score spreads, and decomposition of credit score spreads into the danger premia and credit score losses parts by length decile based mostly on the structural default mannequin of Feldhütter and Schaefer (2018).

Absolutely the measurement of threat premia falls properly inside an inexpensive financial magnitude. Quick-term bonds, with durations of 1 to 2 years, carry a premium near 0 %. This modest short-term threat premium signifies that buyers don’t deal with company bonds strikingly in another way from short-term authorities bonds, regardless of company bonds’ substantial heterogeneity. At longer horizons, the danger premium is far more substantial: it peaks at round 1.8 % at intermediate horizons (4 to 6 years) and ranges off at roughly 1.5 % for the longest length portfolios (twelve years and extra). This nonlinear impact is essentially pushed by the truth that most long-term bonds are issued by the most secure issuers.

At first look, the danger premia might seem small, particularly if one compares them with the fairness time period construction estimates of 10-20 % reported in Weber (2018). A part of the distinction arises as a result of the bond returns are internet of the maturity-matched risk-free fee. As well as, the fairness threat premium arguably displays compensation for upside dangers, to which bonds have restricted publicity.

Conclusion

On this publish, I quantify the form of the forward-looking time period construction within the U.S. company bond market. General, the proof from the market highlights that threat premia, whereas modest in absolute measurement, play a significant function in shaping the time period construction of returns. The upward-sloping profile of each the risk-free fee and the danger premium generates a sizeable time period premium, with the latter accounting for a nontrivial share of long-term yields. These findings recommend that the company bond market offers a very good laboratory for finding out how buyers are rewarded with various kinds of threat, providing worthwhile insights into each asset pricing principle and sensible portfolio allocation.

Tomas Jankauskas is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

cite this publish:

Tomas Jankauskas, “Estimating the Time period Construction of Company Bond Threat Premia,” Federal Reserve Financial institution of New York Liberty Road Economics, February 24, 2026, https://doi.org/10.59576/lse.20260224

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).