Information releases for inflation have been scarce over the previous 4 months as a result of authorities shutdown. Because of this, till January 22 no private shopper expenditures (PCE) knowledge have been out there past September and the patron worth index (CPI) had many lacking entries for the one-month modifications for October and November. On this submit, we use an prolonged model of the New York Fed’s Multivariate Core Development (MCT) inflation mannequin to look at modifications in underlying inflation over this era. The MCT mannequin is well-suited to take action as a result of it decomposes sectoral inflation charges right into a pattern (“persistent”) and a transitory part. In distinction to core (ex-food and power) inflation, its intention is to take away all transitory components, thus figuring out the underlying pattern. As well as, because the mannequin can deal with lacking knowledge—like for October—it might produce values for pattern inflation for months the place little or no knowledge have been launched. Our findings counsel warning: whereas the fragmented knowledge from November initially signaled a deceleration in worth pressures, the mixing of December knowledge signifies that these reductions have been largely transitory. As soon as the complete knowledge set is used, the combination pattern for December stands at 2.83 %, a rise from 2.55 % in September.

Measuring Lacking Inflation Information

We begin by measuring month-on-month inflation charges for the final half of 2025. We’re primarily within the charges for October, November, and December, as little to no knowledge got here out over this era.

The statement equation of the MCT mannequin hyperlinks annualized month-on-month sector-specific inflation charges to widespread and sector-specific pattern and transitory elements:

the place τ(c,t) and τ(i,t) are the widespread and sector-specific tendencies that comply with a random stroll, and ε(c,t) and ε(i,t) are transitory elements which can be modeled as transferring common processes. The mannequin takes each sectoral CPI and PCE charges as enter. The equation above is for sectoral PCE inflation. CPI inflation sectors are modeled equally, however the identical tendencies and idiosyncratic elements as for PCE are included, as much as a relentless of proportionality that’s estimated together with the opposite mannequin parameters. Utilizing the pattern elements, we will compute the combination pattern:

the place the load ω(i,t) is the expenditure share of sector i. As we’re primarily within the pattern underlying core inflation, the weights for the sectors meals, gasoline, and utilities are set to zero. As well as, we compute pattern estimates for core items, nonhousing core providers, and housing utilizing the same aggregation scheme as for the combination pattern however tailor-made to the precise classes.

We estimate the mannequin 5 occasions primarily based on the will increase in knowledge availability described within the following desk. The ten/24/25 info set establishes a benchmark by utilizing solely the inflation knowledge out there throughout the shutdown. That is used to provide a nowcast for realized inflation in all elements for September and corresponding forecasts for October-December. Subsequent, we replace the knowledge set and our estimates each time a brand new CPI or PCE knowledge set is launched.

The Authorities Shutdown Created Vital Gaps in Inflation Information

| Launch Date | Newest CPI | Newest PCE |

|---|---|---|

| 10/24/2025 | September | August |

| 12/5/2025 | September | September |

| 12/18/2025 | November | September |

| 1/13/2026 | December | September |

| 1/22/2026 | December | November |

Notes: Every line exhibits the date at which the knowledge set was elevated and to which month the CPI or PCE launch corresponded. We observe that there was an extra PCE launch on 12/23/25 when the September PCE was revised. As this revision didn’t considerably change the outcomes relative to 12/18/25, we don’t embody it within the evaluation. The 01/22/26 PCE launch included knowledge for November in addition to October. Nevertheless, the info for October have been primarily based on interpolating between September and November, due to this fact we don’t embody it within the MCT mannequin.

Incorporating the November CPI and PCE releases requires extra care. Particularly, as there was no CPI launched for October, and solely an estimate for PCE in October, we can’t compute the month-on-month inflation charges for October and November (see the technical observe within the January 22 PCE launch); solely the bimonthly inflation price may be immediately computed from the worth indexes for September and November. To make sure that the elements are accurately measured, we modify the statement equation above for this era. Particularly, we modify the statement equation for the bimonthly inflation measurement in November as follows:

the place the unobserved month-on-month inflation charges for October and November, November, πi,t and πi,t-1, respectively, are modeled as above. With this modified statement equation, we will again out estimates for the pattern and transitory elements for October and November simply as within the authentic mannequin. Furthermore, we will additionally again out estimates (that’s, nowcasts) for the unobserved month-to-month PCE inflation charges πi,t and πi,t-1 for October and November. Along with a forecast for PCE inflation in December, this helps us reply the query of whether or not inflation is persistent or momentary.

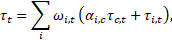

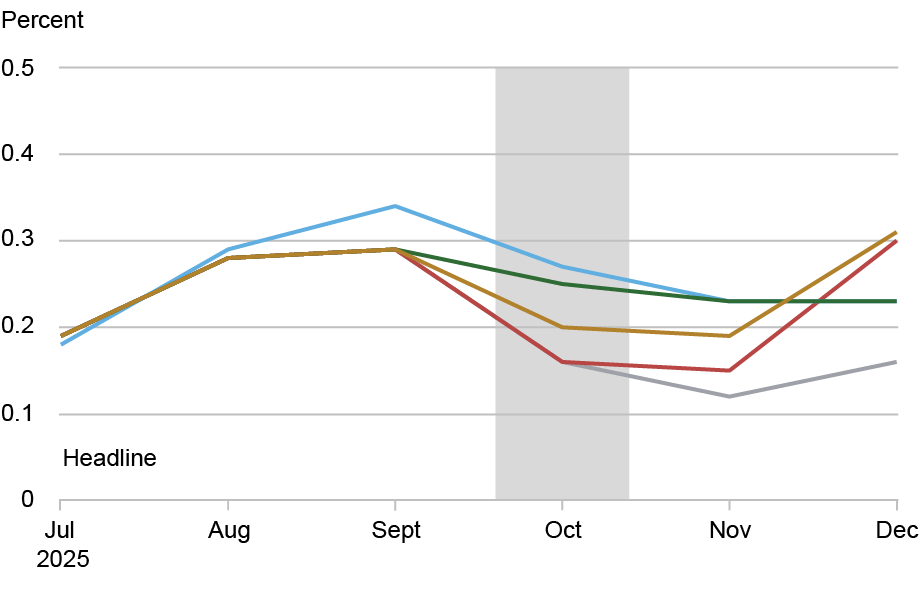

The nowcasts and forecasts for headline and core PCE inflation are proven within the following chart, the place the totally different traces describe the estimates for the totally different info units. We discover that the PCE launch for September (12/05/25) had restricted affect on the forecasts for October-December when in comparison with our October baseline. In distinction, the November CPI launch (12/18/25) vastly reduces the PCE nowcasts and forecasts for October via December; that’s, the November nowcast for headline inflation is almost 50 % decrease (falling from 0.23 to 0.12) when in comparison with the benchmark. For core inflation, the drop is barely decrease however nonetheless sizable (from 0.23 to 0.13).

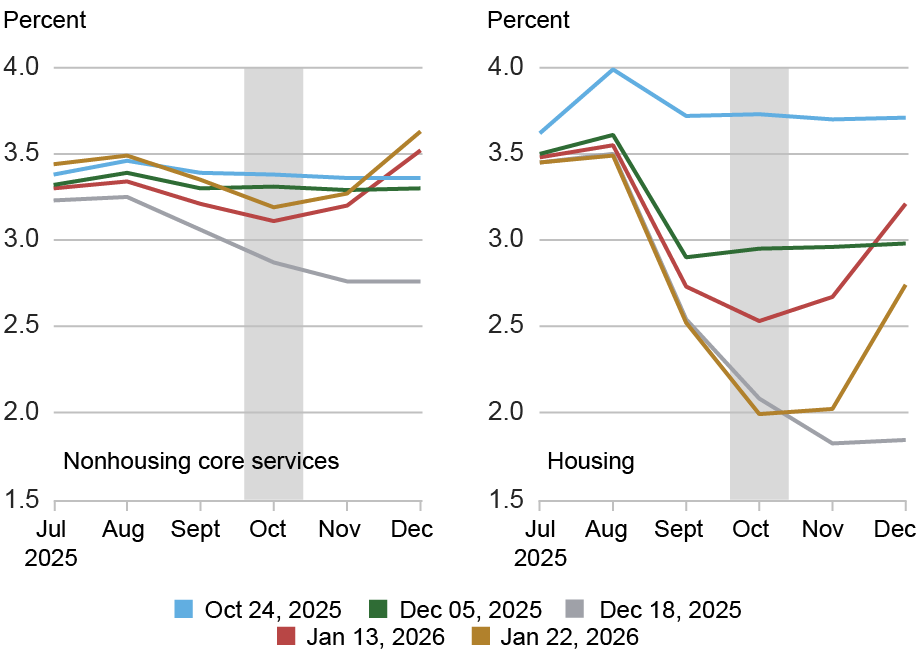

November and December Information Gave Opposing Messages About Inflation Dynamics

Notes: The chart plots PCE inflation nowcasts and forecasts for the knowledge units out there on 10/24/25, 12/05/25, 12/18/25, 01/13/26, and 01/22/26 as indicated by the totally different coloured traces. The vertical grey bar signifies that no CPI/PCE knowledge have been out there for this era. The highest panel gives estimates for headline PCE inflation and the underside panel for core PCE inflation.

The December CPI launch (01/13/26) modifications the optimistic impression that the November CPI gives. Based mostly on December knowledge, the nowcast for November moved upward barely, however most significantly, the December nowcast now exceeds the benchmark forecasts for December, thus erasing any reductions in inflation steered by intermediate knowledge releases. This holds each for headline and core PCE inflation.

Is It Development?

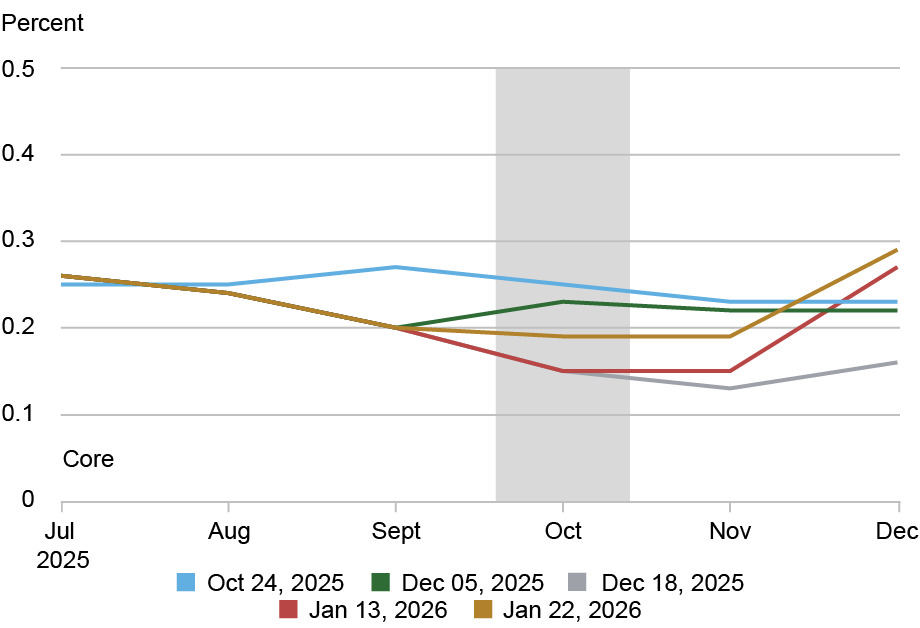

The nowcasts and forecasts that we mentioned combine transitory and pattern elements. This leaves open the chance that the documented variations stemming from the November and December CPI releases are merely transitory. For example, measurement error launched by knowledge assortment throughout or simply after the federal government shutdown might clarify the variations. To research this chance, we extract the pattern estimates from the MCT for the totally different knowledge releases. The estimates are proven within the following chart. The highest left panel exhibits the combination tendencies for every launch.

November and December Information additionally Impacted Development Estimates

Notes: The panel chart plots pattern inflation estimates for various info units that have been out there on 10/24/25, 12/05/25, 12/18/25, 01/13/26, and 01/22/26 are indicated by the totally different coloured traces. The vertical grey bar signifies that no CPI/PCE knowledge have been out there for this era.

We discover a comparable sample to that for the PCE nowcasts: the November CPI vastly lowered the pattern estimate, whereas the December CPI returns the pattern to its benchmark degree established by the pre-shutdown info set dated 10/24/25. Not solely is the combination pattern estimate for December roughly unchanged from its October forecast, however it elevated relative to the September estimate. Particularly, the December MCT stands at 2.83 % whereas the September estimate was 2.55 %.

Wanting on the pattern elements for various broadly outlined sectors—core items, nonhousing core providers, and housing—exhibits that the patterns noticed for the combination are replicated throughout sectors. There are variations concerning the submit December degree, which is both above its September degree (core items and nonhousing providers) or beneath (housing). However the conflicting results of the November and December CPI releases are seen in every sector-specific pattern.

We conclude that the modifications documented within the PCE nowcasts and forecasts throughout the totally different CPI releases will not be solely because of transitory elements however are very a lot pushed by modifications within the pattern elements of the mannequin.

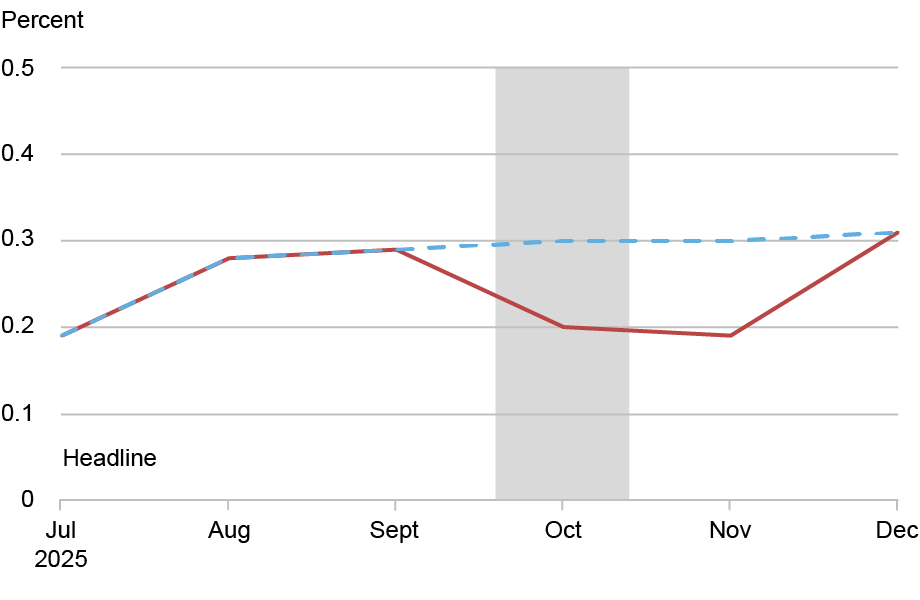

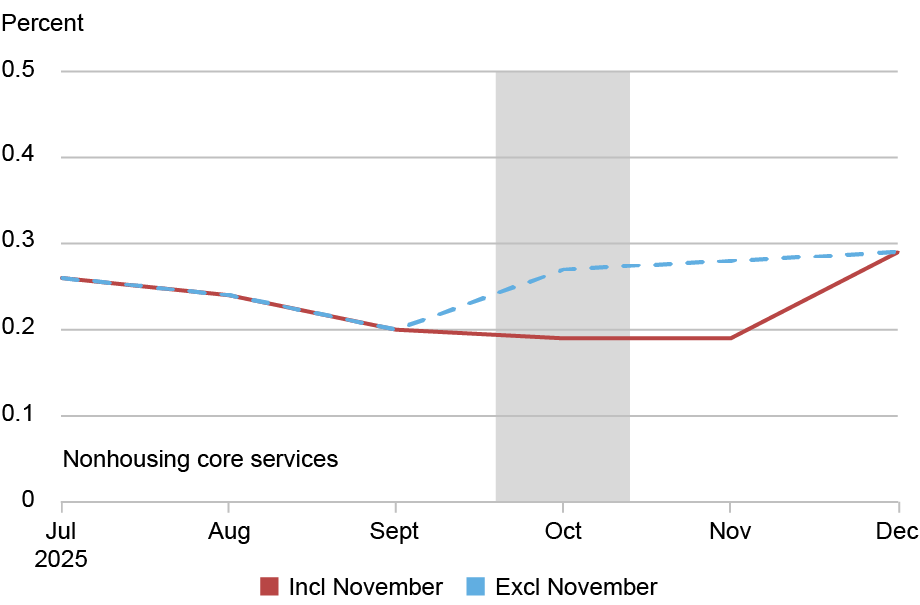

Was November CPI Uncommon?

Given the findings above, it’s pure to ask whether or not the November CPI and PCE releases have been uncommon. Certainly, on the time of the CPI launch, quite a few economists and market analysts raised substantial considerations in regards to the reliability of the discharge, noting that vital gaps in knowledge assortment—brought on by the latest federal authorities shutdown—possible distorted the inflation figures. Many worth observations sometimes gathered in October have been lacking, and delayed knowledge assortment in November meant that some costs have been solely captured later within the month, together with throughout heavy vacation discounting, which may artificially decrease reported inflation. This raised skepticism amongst consultants who warned that the headline slowdown might not replicate true underlying worth tendencies and could possibly be an artifact of the disrupted methodology slightly than a real shift in inflation dynamics.

To review the influence of the November CPI in additional element, we evaluate our newest nowcast, primarily based on the knowledge out there on 01/22/26, with a nowcast that’s computed after setting the November CPI and PCE to lacking. The subsequent chart exhibits the comparability for the PCE nowcasts. We discover that PCE headline and core nowcasts omitting the November CPI launch indicate that headline and core PCE inflation have been practically fixed, or barely growing over the September-November interval.

November CPI/PCE Inflation Was Unusually Low

Notes: The chart plots month-to-month PCE inflation nowcasts and forecasts for the knowledge set out there on 01/22/26, both together with (stable line) or excluding (dashed line) November CPI and PCE. The vertical grey bar signifies that no CPI/PCE knowledge have been out there for this era.

The big downward revision within the pattern estimates leads us to conclude that the November knowledge have been certainly uncommon, possible reflecting the delays in knowledge assortment brought on by the shutdown. However as a result of these points have been momentary, we see the pattern estimates from our MCT mannequin that incorporate December knowledge as a dependable sign of the present state of inflation. By that measure, inflation was shut to three % by the tip of 2025.

Martín Almuzara is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Geert Mesters is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Easy methods to cite this submit:

Martin Almuzara and Geert Mesters, “Seeing By means of the Shutdown’s Lacking Inflation Information,” Federal Reserve Financial institution of New York Liberty Road Economics, February 17, 2026, https://doi.org/10.59576/lse.20260217

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).