After the Nice Monetary Disaster, the European Central Financial institution (ECB) prolonged its financial coverage toolbox to incorporate the usage of long-term loans to banks at rates of interest near zero and even unfavorable. These central financial institution interventions had been geared toward supporting the transmission of expansionary financial coverage and sure performed an important function in bolstering the monetary stability of the euro space, specifically by lowering the prospect of financial institution runs. Nonetheless, quantitative proof on the results of those interventions on monetary stability stays scant. On this put up, we quantify the effectiveness of central financial institution lending applications in supporting monetary stability by the lens of a novel structural mannequin mentioned on this paper.

Empirical Challenges in Assessing Central Financial institution Insurance policies

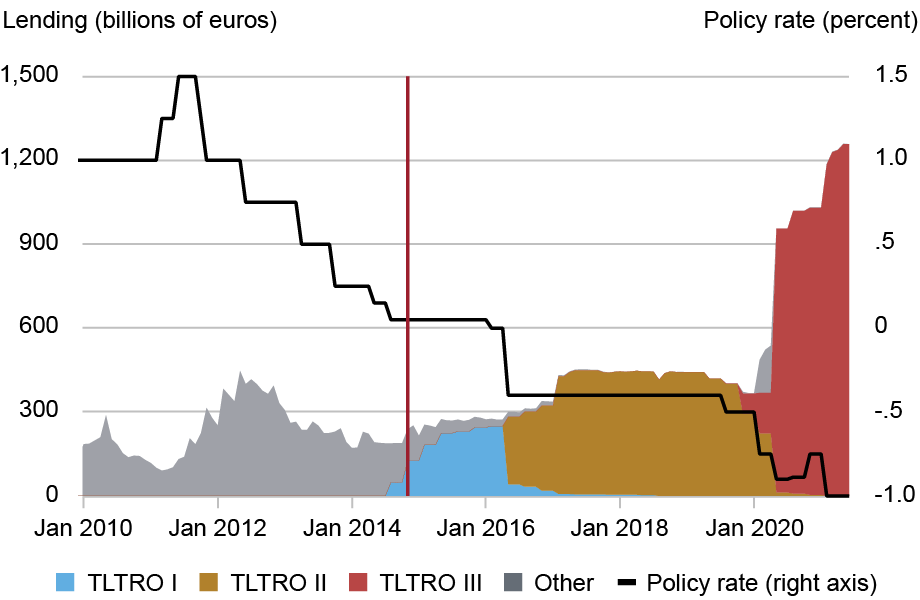

The chart beneath illustrates the evolution of ECB lending to banks in euro space nations, based mostly on a pattern of banks overlaying roughly half of the whole deposit and mortgage market. As we are able to see, most of this lending occurred after the euro space sovereign debt disaster. Lending quickly accelerated in the course of the COVID-19 pandemic, particularly when the central financial institution expanded its stability sheet whereas lowering the rate of interest at which banks may borrow from the central financial institution to as little as -1 % (comparable lending applications had been carried out by the Financial institution of Japan and the Financial institution of England). The quantitative easing amenities launched in parallel by the ECB and lots of central banks world wide, not like these lending operations, weren’t instantly geared toward bolstering the soundness of the banking system.

ECB Lending Amenities and the Coverage Charge

Notes: The chart presents the dynamics of the European Central Financial institution’s (ECB) lending and its coverage fee over 2010-2021. TLTRO I, II, and III correspond to the Focused Longer-Time period Refinancing Operations introduced respectively in June 2014, March 2016, and March 2019. The vertical purple line signifies the start of the pattern interval. Coverage fee is the borrowing fee utilized to refinancing operations over time. The chart is predicated on a pattern of banks similar to roughly 50 % of general mortgage and deposit volumes; this proportion can also be mirrored within the quantity of ECB funding that the pattern covers.

Regardless of the size and direct impression on banks’ stability sheets, quantitative evaluation of the results of refinancing operations is hindered by a set of empirical challenges. First, to quantify the effectiveness of those interventions, one ought to evaluate comparable episodes the place central banks did or didn’t intervene. Nonetheless, these measures had been adopted when financial situations had been worsening, making it difficult to isolate the function of financial coverage. Second, financial institution runs will be averted even within the absence of an express central financial institution intervention, as depositors’ expectations of an intervention will be ample to assuage their fears and cease them from operating on a financial institution. All of this makes it troublesome to establish an appropriate benchmark within the knowledge (one during which financial situations are comparable however central banks don’t intervene and financial institution runs materialize), thereby calling for a extra formal analytical framework.

Monetary Stability and the Central Financial institution Lending Charge

A current paper by Albertazzi, Burlon, Jankauskas, and Pavanini overcomes these empirical challenges, quantifying the effectiveness of central financial institution lending applications by a structural framework of the euro space banking sector. The mannequin options demand and provide in imperfectly aggressive deposit and mortgage markets, in addition to debtors’ and banks’ default danger and the central financial institution’s funding facility. The construction of the mannequin allows the identification of all various situations, together with runs, that would have materialized, at every cut-off date and in every euro space nation banking sector. By permitting us to judge how these situations are affected by central financial institution interventions, this framework supplies a complete benchmark for extra in-depth coverage evaluation.

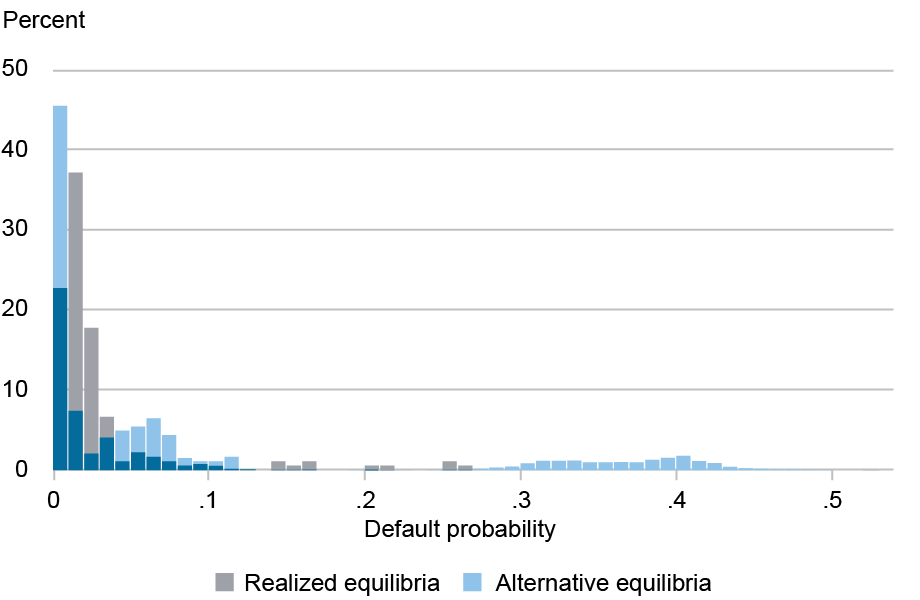

We begin by displaying our model-implied various situations. The chart beneath presents the distribution of historic and model-implied financial institution default possibilities in euro space nations over 2014-2021. Whereas the realized default possibilities (grey bars) exhibit substantial heterogeneity, the mannequin reveals that the choice situations are characterised by a visibly thicker proper tail (blue bars). Particularly, the mannequin unveils situations exhibiting financial institution default possibilities of as much as 50 %. Since excessive default danger probably carries massive financial welfare prices, it’s important to think about such circumstances whereas assessing financial coverage implications.

Realized and Various Financial institution Default Possibilities

Notes: The chart presents the distribution of realized and various equilibria. “Realized equilibria” mirror the information (December observations from 2014 to 2020 plus July 2021 for the balanced panel of thirty banks). “Various equilibria” are the situations implied by the mannequin. Darkish blue bars are the place the 2 equilibria overlap.

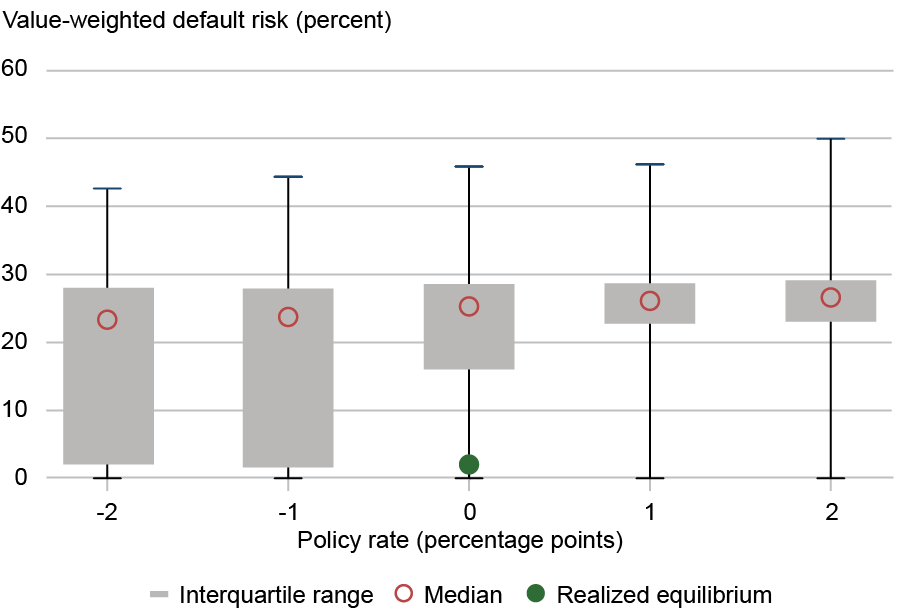

How did the central financial institution lending applications impression monetary stability? Our framework sheds gentle on this query. We mannequin the provision of central financial institution funding by various the charges at which the central financial institution lends to banks, offering a secure supply of financing in instances of misery when flighty uninsured deposits might depart the banks. We use counterfactual simulations of the mannequin to quantify the shadow worth of the central financial institution’s interventions, documenting what would have occurred to banks’ fragility if these insurance policies had been kind of accommodative. We discover {that a} 1 proportion level enhance within the fee at which banks borrow from the central financial institution will increase banks’ default chance by, on common, 1.8 proportion factors. The chart beneath illustrates this impact by displaying the distributions of situations with greater (optimistic numbers) and decrease (unfavorable numbers) coverage charges. We are able to see that when the funding fee will increase, the distribution of default possibilities shifts upward, with a pronounced impact on the higher tail (most) and the interquartile vary. This highlights substantial stability good points stemming from central financial institution lending at decrease charges.

Banks’ Default Danger Will increase with Increased Coverage Charges

Notes: The chart shows the distribution of equilibria for every stage of the coverage fee and throughout country-year situations of banks’ default possibilities in ranges. The black line exhibits the complete vary of the distribution, the grey space the interquantile vary, the purple empty circle the median, and the inexperienced stable circle the median of the realized equilibrium.

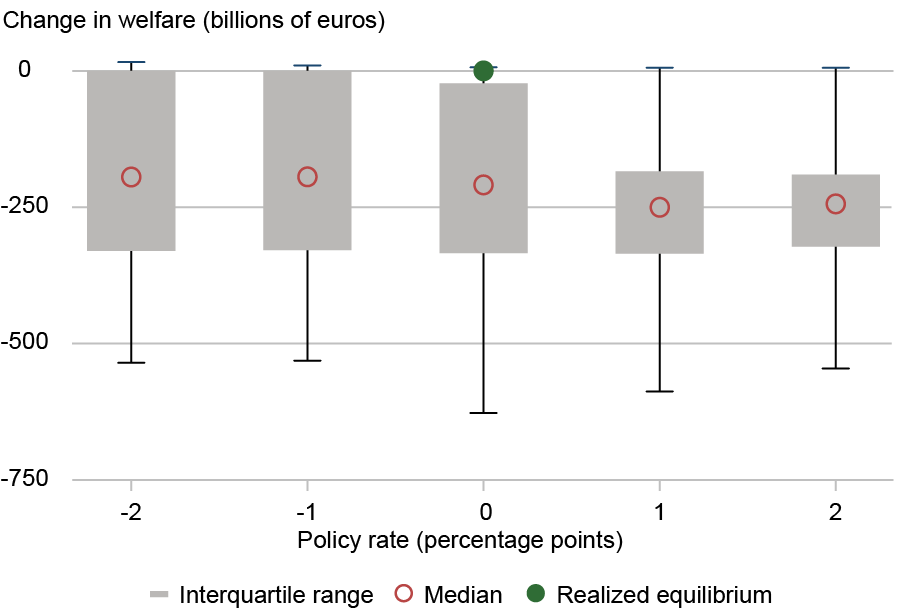

The great evaluation of central financial institution interventions considers not solely banks’ default possibilities but in addition the prices of those applications. We consider the interventions utilizing a welfare idea that instantly incorporates the financial results on anticipated deposit insurance coverage prices, financial institution earnings, and deposit and lending charges, which have an effect on the well-being of depositors and debtors. The chart beneath exhibits the distribution of welfare throughout situations and various coverage charges. These distributions largely mirror these of default possibilities: situations with excessive bank-run dangers are related to massive potential welfare losses (mirrored within the tails).

Welfare Outcomes Enhance with Decrease Coverage Charges

Notes: The chart shows the distribution of equilibria for every stage of the coverage fee and throughout country-year situations of whole welfare in deviation from the realized equilibrium in billions of euros. The black line exhibits the complete vary of the distribution, the grey space the interquantile vary, the purple empty circle the median, and the inexperienced stable circle the median of the realized equilibrium.

We observe that decrease lending charges result in financial good points, suggesting that the central financial institution lending applications had been welfare-improving. This impact was primarily pushed by lowered financial institution danger, decrease anticipated deposit insurance coverage prices, and decreased lending charges for households and corporations. On the similar time, since decrease coverage charges had been additionally transmitted to deposit charges, a lot of the unfavorable results are borne by depositors. Whereas the general welfare acquire was optimistic, the multifaceted nature of financial coverage highlights the trade-offs policymakers face.

Conclusion

On this put up, we quantify the impression that ECB lending amenities had on the euro space banking sector’s monetary stability. To beat empirical challenges within the evaluation of those interventions, we depend on the novel mannequin of Albertazzi, Burlon, Jankauskas, and Pavanini (2025), which allows the restoration of other situations and simulation of various coverage counterfactuals. The mannequin simulations present that these insurance policies had been significantly efficient in lowering the danger of unwarranted and self-fulfilling runs and bettering general welfare.

Tomas Jankauskas is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ugo Albertazzi is an adviser within the Directorate Common Macroprudential Coverage and Monetary Stability on the European Central Financial institution.

Lorenzo Burlon is a head of part within the Directorate Common Financial Coverage on the European Central Financial institution.

Nicola Pavanini is a professor of finance and industrial group at Tilburg College.

The best way to cite this put up:

Tomas Jankauskas, Ugo Albertazzi, Lorenzo Burlon, and Nicola Pavanini, “The Shadow Worth of Central Financial institution Lending,” Federal Reserve Financial institution of New York Liberty Road Economics, October 16, 2025, https://doi.org/10.59576/lse.20251016

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York, the Federal Reserve System, the European Central Financial institution, or the Eurosystem. Any errors or omissions are the accountability of the creator(s).