The White Home introduced final week that it’s “taking steps” to ban giant institutional traders from shopping for single-family houses. It’s unclear whether or not the President has authorized authority to do that with out motion from Congress. However setting apart that difficulty, let’s examine the deserves of the coverage.

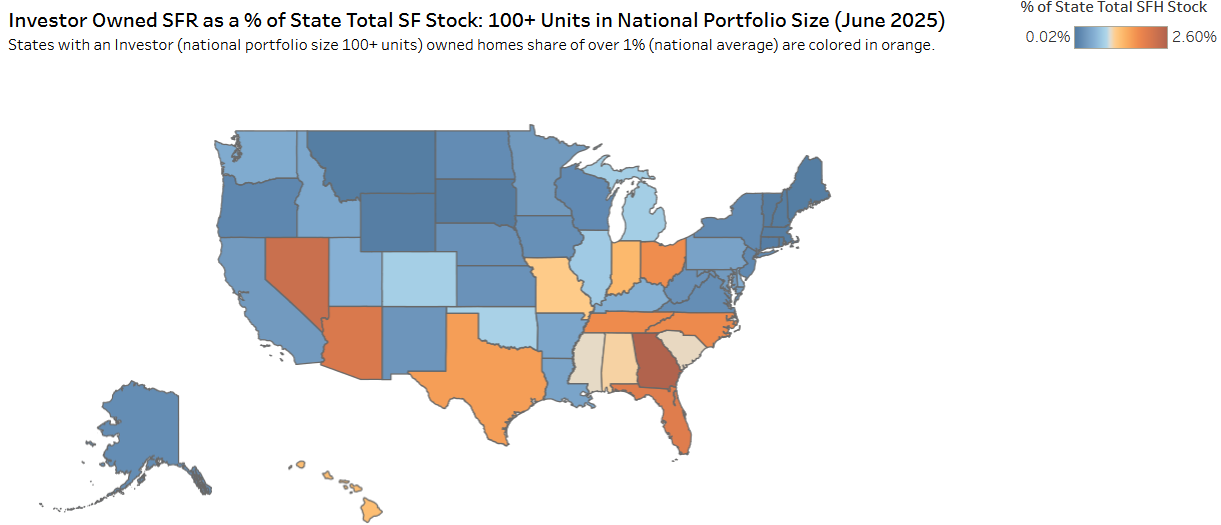

Many commentators have identified that institutional traders have such a small presence within the single-family market that it’s implausible to attribute a lot of the latest appreciation in home costs to their actions. Institutional traders, outlined as these proudly owning 100 or extra houses of their portfolios, personal much less than 1 % of the single-family housing inventory nationally and solely about three % of single-family houses for hire. Their buying actions have declined since 2022, however even on the peak the most important (1000+ houses) traders accounted for below three % of single-family home purchases nationally. Institutional traders matter extra in some markets than in others, however in no metro space do firms with 100+ house portfolios personal greater than 5 % of the single-family inventory. Determine 1 exhibits the massive investor possession share by state. All of the states in blue – the massive majority of them – have a big investor share lower than one % of single-family inventory.

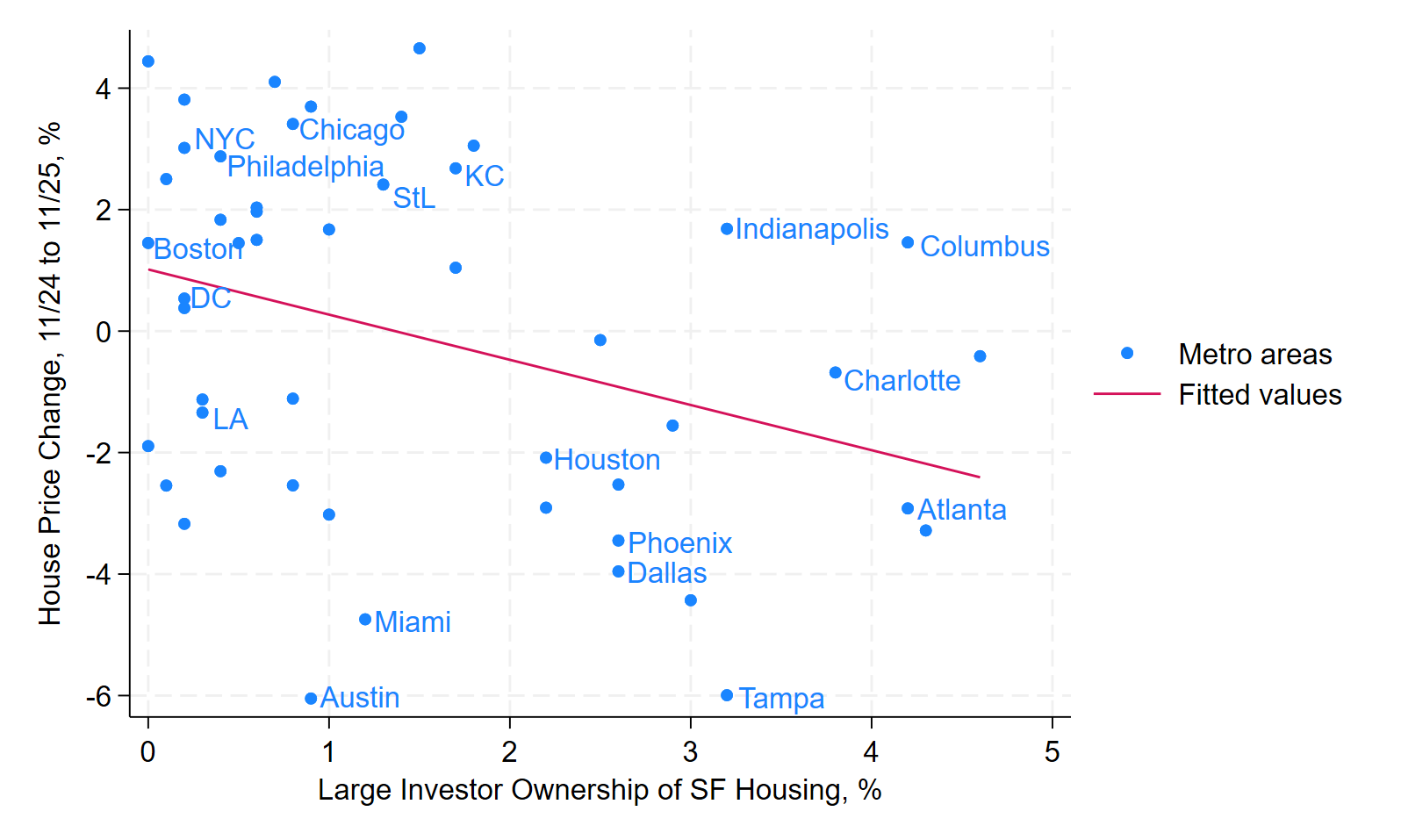

If we zoom out to the most important 50 metro areas, the identical correlation holds, although a bit extra weakly. Locations with extra giant institutional investor possession of single-family houses noticed bigger value declines over essentially the most lately out there 12-month interval (Determine 3).

Determine 1: Massive Investor SF Possession Share by State

Supply: AEI Housing Heart

What commentators have thus far left unsaid is simply how useful the small quantity of institutional funding is for the American housing market. It’s not simply not a massive downside; it’s not an issue in any respect, however somewhat one thing to be welcomed.

Institutional traders assist make the housing market extra liquid and fewer cyclical. They improve the standard of the housing inventory, usually at decrease value than smaller renovation outfits. They make fascinating neighborhoods accessible for households that might not afford to purchase in these neighborhoods. More and more, they’re straight rising housing provide.

Institutional traders first began to take curiosity in single-family homes in 2012, on the backside of the final housing cycle. They’re much less capital-constrained than smaller traders, not to mention most owner-occupiers. In consequence, they’re higher ready to make use of money reserves to determine good offers and the market and purchase them at costs that make sense over the long term. The flexibility of institutional traders to help the housing market after a monetary disaster will assist forestall future liquidity issues within the mortgage finance sector from spiraling right into a housing crash.

Why have institutional traders solely emerged as gamers in single-family housing so lately? Economists level to technological advances equivalent to cloud computing and cellular connectivity which have helped with acquisition and administration of single-family homes. Machine studying (synthetic intelligence) might have helped develop forecast fashions for acquisition as nicely. To make sure, some patrons grew to become overconfident of their forecast fashions and ended up shedding some huge cash — most famously Zillow. However Zillow’s mannequin was to purchase low and promote pricey, somewhat than handle rental properties. Most institutional traders are inclined to concentrate on specific neighborhoods or cities to scale back the per-unit prices of property administration.

Mortgage underwriting requirements tightened dramatically after the Nice Recession, making it tough for youthful People and people with a variety of revenue from “aspect gigs” and self-employment to qualify. In consequence, homeownership charges declined. By making extra single-family houses out there to renters, buy-to-rent institutional traders have helped households that might not afford to purchase or qualify for a mortgage to maneuver into fascinating neighborhoods.

The latest and cautious paper on the topic finds that enormous institutional traders barely elevate home buy costs and cut back rents. The impact on costs is really tiny: for each share level of the overall single-family housing inventory owned by giant institutional traders, home costs go up 1.7 %. Since these traders personal lower than one % of the single-family housing inventory nationally, counterfactually eliminating all giant investor possession of single-family housing would lower nationwide home costs by lower than 1.7 %. And even Trump shouldn’t be proposing to pressure traders to promote what they already personal.

The impact on rents is barely greater: for each share level of the single-family rental inventory that institutional traders personal, rents fall 0.7 %. Since institutional traders personal about three % of the nationwide single-family rental inventory, the overall impact on rents is round destructive two %. Whereas small traders substitute to some extent for big traders, the Coven paper nonetheless finds that enormous traders enhance the overall provide of single-family rental houses by 0.5 for each house that they buy.

Foreclosures are a disproportionate channel by which institutional traders purchase houses. For instance, INVH reported that 37 % of the homes they acquired between September 2015 and September 2016 had been from distressed gross sales. Usually, giant traders renovate houses earlier than renting them out. Invitation Properties reported spending about $39,000 per bought house on renovations in 2021. Massive traders might have a comparative benefit in shopping for and renovating houses as a result of they’ve full-time groups working in particular areas in response to established procedures and shopping for supplies in bulk. Thus, giant institutional traders enhance the common high quality of the US housing inventory.

More and more, giant institutional traders develop whole housing provide straight, via build-to-rent developments. Within the Q2 2024 final yr, build-to-rent (BTR) developments had been 7.2 % of all single-family home begins. BTR isn’t helpful for getting renter households entry to fascinating neighborhoods, however it’s particularly helpful for rising general housing provide, lowering each sale costs and rents as a result of the rental and for-sale markets are linked. When BTR drives down rents via new provide in the marketplace, that encourages some households to hire somewhat than purchase and reduces for-sale costs for patrons of the remaining houses in the marketplace. BTR has been particularly fascinating in unfreezing a housing market challenged by mortgage lock-in. Sadly, HUD Secretary Invoice Pulte reportedly desires to crack down on BTR in addition to institutional purchases of current houses.

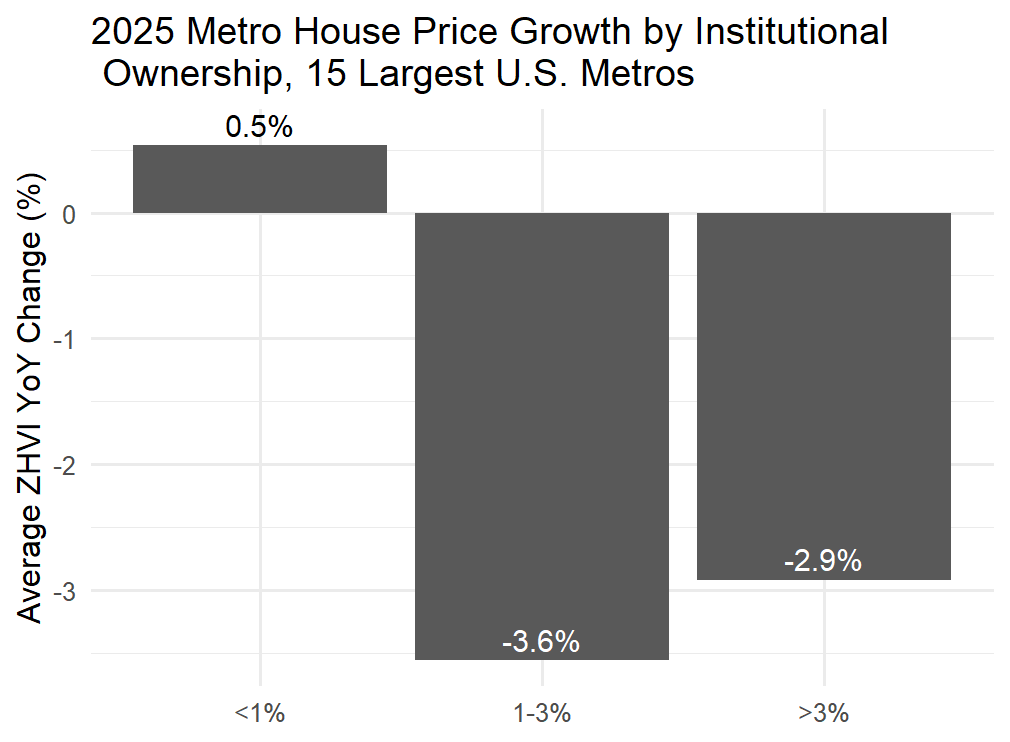

Previously yr, housing costs have declined essentially the most in markets the place giant institutional traders are concentrated. If we take a look at the most important 15 metro areas within the nation, home costs have grown 0.5 % within the markets with below one % institutional possession and fallen 3.6 % within the markets with 1-3 % institutional possession. In the one market with over three % possession (Atlanta), costs have fallen 2.9 %.*

Whereas correlation doesn’t equal causation, these knowledge actually forged doubt on any claims that banning institutional funding will cut back home costs.

Left- and right-wing populists that need to ban institutional possession of single-family houses will harm the common American in the event that they get their approach. Institutional traders are rising housing provide and making housing markets extra liquid and fewer unstable. They assist youthful households and people of modest revenue achieve entry to fascinating neighborhoods. Their upward impression on costs is tiny, and will even have reversed as soon as we take into account the brand new impression of build-to-rent improvement.

* These knowledge are my very own calculations primarily based on knowledge from the AEI Housing Heart and the Zillow Housing Worth Index. The ZHVI covers the 12 months from November 2024 to November 2025.