Good measures of labor market tightness are important to foretell wage inflation and to calibrate financial coverage. In an October 2024 publish, we launched a brand new indicator of labor market tightness and confirmed that it tracked wage inflation finest out of a broad vary of tightness measures. On this publish, we replace our index via 2025 and present that it additionally forecasts future wage inflation finest each out and in of pattern. As well as, we spotlight availability of the index as a new recurrently up to date characteristic on the New York Fed’s web site.

Watch because the economists behind the HPW Index describe the index, the way it compares to different measures, and its usefulness for policymakers.

Updating the HPW Index and Introducing a Month-to-month Collection

Many policymakers and practitioners have an interest within the tightness of the labor market—that’s, how tough it’s for corporations to search out staff—to forecast wage inflation. Nonetheless, conventional measures of labor market tightness, such because the unemployment charge or the ratio of vacancies to unemployed, have had blended efficiency in monitoring wage progress just lately. For instance, the unemployment charge shortly returned to its pre-pandemic stage after spiking in early 2020, whereas wage progress remained elevated at far above its pre-pandemic stage into 2022. As proven in our earlier publish, we are able to account for this elevated wage progress if we issue within the habits of employed job seekers, as on-the-job search is a key element of labor market tightness.

Particularly, we discover that two measures stand out of their potential to trace wage progress—the quits charge and vacancies per efficient searcher (V/ES), the place searchers embrace each the unemployed and the employed. We acquire the quits charge and job openings from the Job Openings and Labor Turnover Survey (JOLTS) and assemble efficient searchers from the Present Inhabitants Survey (CPS). Each measures incorporate employed job seekers’ exercise as a central enter. We construct on this perception by setting up the Heise, Pearce, Weber (HPW) Labor Market Tightness Index, which mixes the quits charge and V/ES utilizing as weights coefficients from a regression of wage progress on these two variables. The HPW Index tracks present and future wage progress finest out of a big vary of tightness measures.

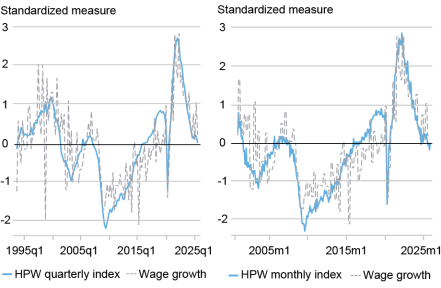

The chart under exhibits an up to date model of the HPW Index on the quarterly (left panel) and month-to-month (proper panel) frequency, via 2025:Q3 and November 2025, respectively. We evaluate the index to three-month wage progress from the Employment Value Index (ECI), with every sequence normalized to have a imply zero and a typical deviation of 1. The month-to-month HPW tightness sequence is constructed utilizing the month-to-month quits charge and V/ES weighted by the regression weights from the quarterly regression, for the reason that ECI is just obtainable at a quarterly frequency. A studying of 1 for both variable signifies that the measure is one normal deviation above its imply within the interval between 1990:Q2 and 2025:Q3. The chart exhibits that within the current interval each the HPW Index and wage progress have been comparatively flat, after trending downward from 2022 via 2024. The present studying of the month-to-month HPW Index (-0.01 in November 2025) signifies that wage pressures are at their long-run common.

The HPW Index Has Fallen to Its Lengthy-Run Common in Each the Quarterly and Month-to-month Collection

Notes: The HPW Index is computed as a weighted common of the quits charge and vacancies per efficient searcher, the place the weights are obtained as described in Desk 2 of Heise, Pearce, and Weber (2024, rev. March 2025). Wage progress is measured utilizing the three-month share change within the ECI for salaries and wages of personal trade staff. Each the HPW Index and wage progress are normalized to have a imply of zero and a typical deviation of 1. Quarterly knowledge are from the primary quarter of 1994 to 2025:Q3. Month-to-month knowledge are from December 2000 to November 2025.

Forecasting

Our earlier publish highlighted that our quarterly tightness index tracked wage progress contemporaneously, as proven within the chart above. Right here, we present that the HPW Index also can forecast wage inflation properly, utilizing solely the data obtainable in actual time.

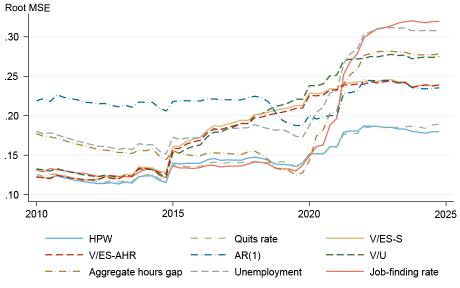

The chart under makes use of quarterly knowledge to research how properly numerous labor market tightness measures forecast subsequent quarter’s studying of the three-month ECI wage progress out-of-sample. For comparability, we additionally embrace outcomes from a mannequin that forecasts subsequent interval’s wage inflation based mostly on final interval’s wage inflation alone, in different phrases, assuming an AR(1) mannequin for wage inflation. Observe that the chart highlights only some of the tightness measures we thought of; see our accompanying Workers Report for a full record and extra detailed definitions.

HPW and the Quits Charge Present the Finest Out-of-Pattern Forecast of Wage Progress

Notes: HPW is the HPW Labor Market Tightness Index. The quits charge is from JOLTS. V/ES-S is vacancies per efficient searcher computed from JOLTS and CPS knowledge following Sahin (2020). V/ES-AHR is similar ratio however following Abraham, Haltiwanger, and Rendell (2020). The AR(1) mannequin forecasts wage progress utilizing its personal lag. V/U is the ratio of vacancies to unemployed. Mixture hours hole is from Faberman, Mueller, Sahin, and Topa (2020). Unemployment is the U‑3 unemployment charge. Each the U-3 and the job-finding charge for unemployed staff are computed from CPS knowledge. Collection don’t lengthen past 2024:This fall as a result of some sequence should not obtainable past that date.

We assemble the out-of-sample forecasts beginning with 2004:Q1 utilizing the info obtainable as much as 2003:This fall to foretell the following quarter’s ECI progress, after which roll this technique ahead to subsequent quarters. Given the predictions, we compute the squared distinction between our predicted wage progress and the realized wage progress in every quarter. We common these variations over forty-quarter rolling home windows, beginning with the window that ends in 2010:Q1. The vertical axis plots this root imply sq. error (root MSE) over time from 2010:Q1 onward. To interpret the chart, be aware {that a} decrease worth for a specific measure is sweet, within the sense that the measure would have been extra correct and made fewer errors as much as that cut-off date than a measure with a better worth.

The chart exhibits that previous to the COVID interval, the quits charge and the HPW Index have been the measures with one of the best forecasting efficiency, however many different tightness measures carried out practically as properly. In 2020, the quits charge and HPW separate from the opposite measures of tightness and change into unambiguously one of the best out-of-sample predictors of wage progress. Towards the tip of our pattern, HPW modestly outperforms even quits in forecasting wage inflation. They’re the one two measures to persistently outperform the AR(1) mannequin.

Conventional tightness measures corresponding to vacancies over unemployment (V/U) additionally do a comparatively good job in predicting wage progress till about 2015, when V/U begins to falter. The regular deterioration within the forecasting efficiency of vacancy-based measures corresponding to V/U and V/ES by itself aligns with earlier work discovering that the connection between vacancies and different labor market variables has shifted over time.

Conclusion

Our findings recommend that the HPW Index and the quits charge are one of the best predictors of wage progress within the subsequent quarter. Going ahead, the net characteristic launched at present will replace each a quarterly and a month-to-month sequence of HPW together with the ECI, to trace wage pressures in actual time. The mannequin is estimated on the quarterly frequency as a consequence of wage info, however with month-to-month releases of CPS and JOLTS knowledge the HPW Index can also be launched on the month-to-month stage to offer a recurrently up to date abstract of the state of the U.S. labor market.

Sebastian Heise is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jeremy Pearce is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jacob P. Weber is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Methods to cite this publish:

Sebastian Heise, Jeremy Pearce, and Jacob P. Weber, “Measuring Labor Market Tightness: Knowledge Replace and New Net Characteristic,” Federal Reserve Financial institution of New York Liberty Avenue Economics, January 8, 2026, https://doi.org/10.59576/lse.20260108

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).