The time period “exorbitant privilege” emerged within the Sixties to explain the benefits derived by the U.S. financial system from the greenback’s standing because the de facto world reserve forex. On this publish, we study the exorbitant privilege that accrued to the Netherlands within the eighteenth century, when the Dutch guilder loved world reserve forex standing. We present how the personal actions of monetary establishments created and maintained this privilege, even within the absence of a central financial institution. Whereas privilege benefited the Dutch monetary system in some ways, it additionally laid the seeds of later monetary disaster.

Origins of the Netherlands’ Exorbitant Privilege

A rustic’s exorbitant privilege permits it to borrow and lend utilizing its personal forex on extra favorable phrases than different international locations utilizing their native currencies. Because the U.S. has been the only beneficiary of exorbitant privilege since World Battle II, researchers look to historical past to grasp privilege’s determinants. Prior research have examined the exorbitant privilege loved by the UK within the nineteenth century, when the British pound was the worldwide reserve forex. We concentrate on the expertise of the Netherlands within the seventeenth and eighteenth centuries, because the Netherlands had a unique monetary system from the UK on the time and from the U.S. as we speak. Specifically, because the Netherlands didn’t have a central financial institution and its monetary intermediaries have been nonbank monetary establishments (NBFIs), its exorbitant privilege grew out of the personal actions of those NBFIs, as we present beneath.

The position of the Dutch guilder as the worldwide reserve forex allowed the Netherlands to have the bottom prevailing charge of curiosity in Europe, as international traders have been extra keen to alternate their surpluses for monetary belongings within the Netherlands. One consequence was that international traders left massive deposits with the main service provider banks of Amsterdam. Since these deposits paid no curiosity, they offered these corporations with a supply of low-cost funding.

Hope & Co.: A Case Examine of Exorbitant Privilege

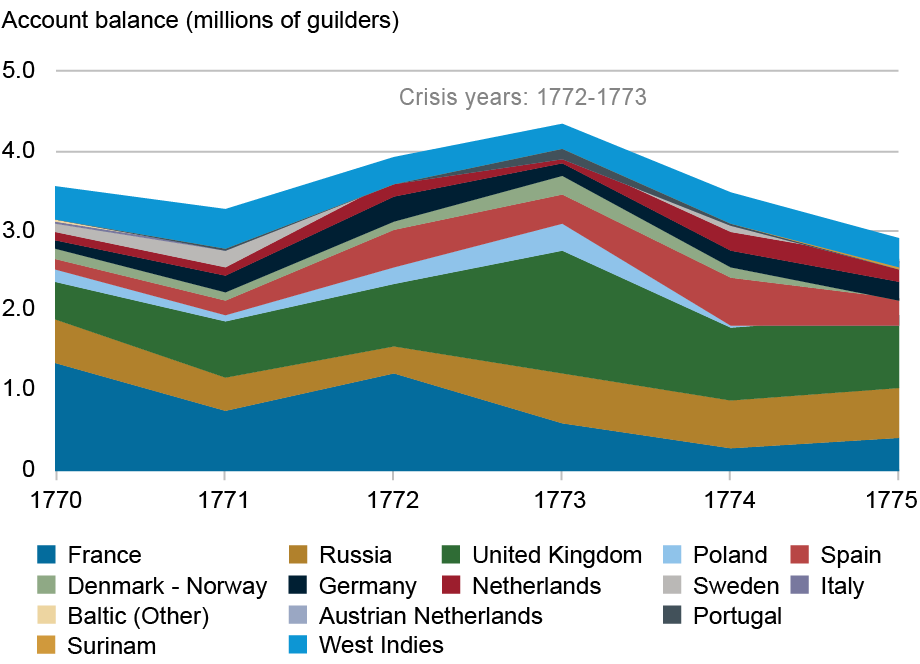

To supply a extra granular view of how the Dutch system operated, we analyze the ledgers of Hope & Co., the most important personal monetary agency within the Netherlands within the early 1770s, when Amsterdam was possible nonetheless the most important monetary heart in Europe. Hope was a broker-dealer, buying and selling in commodities, securities, and cash markets; it additionally issued securities and was one of many main cross-border funds suppliers. Between 1770 and 1775, greater than 1,200 lively worldwide purchasers maintained accounts with Hope, most of which contained callable, non-interest-bearing balances, like wholesale deposits in trendy instances.

About 20 % of Hope’s purchasers held balances however transacted sometimes. A few of these purchasers, significantly these removed from Amsterdam resembling in Russia or the West Indies, might have been utilizing their accounts as a protected, offshore retailer of worth. These accounts additionally served as a method of fee, for the reason that Financial institution of Amsterdam (AWB), the first entity for clearing cash market transactions, restricted international corporations from holding accounts with it.

The remaining 80 % of Hope’s purchasers tended to maintain massive balances (see chart beneath)—however solely quickly. In some circumstances, purchasers positioned funds in anticipation of enormous outlays (resembling purchases of international items when the Dutch East India delivery fleet returned to Amsterdam). In different circumstances, they held funds in three way partnership accounts, anticipating to make use of them for enterprise ventures. Lastly, purchasers held monies for future curiosity funds on bonds in addition to in anticipation of hypothesis or different alternatives.

Overseas Depositors Held Massive Balances with Hope & Co.

Notes: The chart reveals balances in accounts held by international depositors at Hope & Co. by area of origin. The pattern interval is 1770-75.

The non permanent nature of deposits implies that, on the particular person shopper stage, deposit balances have been unstable over time (see chart beneath), with a coefficient of variation (in different phrases, the usual deviation of an account stability divided by the common stability) of 73 % on common. Nonetheless, if purchasers didn’t withdraw deposits on the similar time, Hope’s massive base of worldwide depositors afforded a substantial amount of diversification, in order that for the complete portfolio, the coefficient of variation was simply 30 %.

Particular person Account Balances Have been Extremely Risky

Notes: The chart reveals the coefficient of variation of balances in accounts held by international depositors at Hope & Co. by area of origin, averaged over all accounts within the area. One area with a unfavourable common stability is excluded. The pattern interval is 1770-75.

Along with offering a liquidity reserve, Hope’s cross-border deposits shaped a secure base of zero-interest funding for its personal actions. Certainly, the Hopes have been in a position to fund about two-thirds of the agency’s liabilities curiosity free. On condition that the Hopes anticipated to realize a 3-4 % return on passive funding in a typical yr, the deposit balances might have generated 15-25 % of the agency’s immense annual income. Hope & Co. appears to have stored about half of this funding in working capital for its core companies and the opposite half on deposit with AWB. It was the most important transactor with the AWB, utilizing its AWB deposits to repeatedly buy short-term payments on the cash market, lend cash in opposition to securities or commodities, and speculate out there by itself account.

Advantages for the Dutch Economic system

Plentiful international funds helped make sure that the Dutch Republic had the bottom rate of interest in Europe, which helped the nation to offset declining balances of merchandise commerce through its massive exports of monetary providers resembling funds, credit score, insurance coverage, and brokerage. It additionally had essentially the most liquid cash markets in Europe, since corporations like Hope might settle for or low cost payments profitably, even when margins have been very skinny.

As well as, Amsterdam turned a supplier of world protected belongings. Political or monetary turmoil in neighboring international locations tended to attract in extra deposits for safekeeping. This allowed Hope & Co. and different massive retailers in Amsterdam to perform as personal “lenders of final resort” and stabilize the Dutch financial system in durations of disaster. For instance, Hope & Co. was in a position to backstop the Amsterdam cash markets through the worst months of the key monetary disaster of 1772‑73. It did so by shopping for at a reduction a big quantity of riskier payments of alternate coming to the market, rising its share in discounting riskier payments from 10 % earlier than the disaster to 25 % on the top of the disaster.

In flip, the stabilizing results of interventions by massive service provider banks incentivized the movement of latest cross-border deposits throughout crises from corporations in search of a protected place to retailer their cash. Certainly, deposits at Hope & Co. surged in 1772-73 (see first chart above). This phenomenon is much like the movement of deposits into the fashionable U.S. banking system throughout disaster durations.

Ultimate Ideas

The exorbitant privilege loved by the Dutch within the eighteenth century arose from the position of the guilder as the worldwide reserve forex and the actions of NBFIs that offered protected belongings to foreigners and huge home corporations. In flip, the NBFIs profited from this association by accessing zero-interest-rate funding and helped to stabilize the Dutch monetary system throughout crises.

Exorbitant privilege, nonetheless, generally is a double-edged sword. The supply of low-cost cash resulted in dangerous conduct by massive, extremely leveraged wholesale gamers and a monetary disaster in 1772, resulting in boom-and-bust cycles in such belongings as plantation mortgages, international sovereign lending, and leveraged bets on the efficiency of equities. As soon as the guilder misplaced its reserve forex standing on the flip of the nineteenth century resulting from struggle and revolution, the Netherlands was now not in a position to finance its large debt at low charges, and its perch on the prime of worldwide public finance collapsed.

Stein Berre is a principal examiner within the Federal Reserve Financial institution of New York’s Supervision Group.

Asani Sarkar is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Methods to cite this publish:

Stein Berre and Asani Sarkar, “Dutch Deal with: The Netherlands’ Exorbitant Privilege within the Eighteenth Century,” Federal Reserve Financial institution of New York Liberty Avenue Economics, October 7, 2025, https://doi.org/10.59576/lse.20251007

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).