Strain is constructing from the US for a Plaza Accord 2.0 as a part of the US President’s makes an attempt to ‘enhance’ the US commerce scenario. I exploit the time period ‘enhance’ cautiously as a result of the US President appears suppose that making it tougher and costly for US shoppers and companies to entry imports from overseas is a profit to the identical. Whereas Japan is being mentioned on this body, the actual US goal is China. Nevertheless, it’s unlikely that the US will be capable of bully China into agreeing to the same deal that the US successfully compelled on to Japan and different nations underneath the Plaza Accord 1.0 in 1985. Additional, the Plaza Accord 1.0 was extraordinarily disruptive – some say it brought about the asset worth bubble in Japan, which led to the secular stagnation, after the bubble burst. And, there may be little proof that it led to any important long-term advantages for the US anyway.

Plaza Accord 1.0

The historical past of the yen within the put up World Struggle 2 period is characterised by a number of US meddling.

When President Nixon shut the ‘gold window’ in August 1971, which successfully introduced the Bretton Woods system of mounted change charges that had operated within the interval for the reason that finish of World Struggle 2 to an finish, his motivation was in no small half because of the massive present account deficits the US had been working in opposition to Japan.

The US believed then that the currencies of their major buying and selling companions had been undervalued, notably the yen and the Deutschmark.

Instantly after the US devalued in mid 1971, they negotiated (in December 1971) the Smithsonian Settlement which was an try to get a number of nations to revalue their currencies and re-establish the mounted change charge regime deserted earlier that yr.

The settlement wasn’t sustainable given the modifications within the underlying commerce fundamentals that had introduced the system down within the first place and it was deserted in March 1973.

At that time, most nations floated their currencies, though the Japanese authorities was underneath intense home strain to forestall the foreign money from appreciating as a result of native corporations and many others didn’t desire a return to the big exterior deficits of the Sixties.

The Japanese industrialists had been mercantilist of their considering and thought that high-priced imports that the nation was barely capable of afford had been a very good factor.

The upshot was that Japan by no means actually floated on this interval.

Whereas the yen did respect considerably throughout the remainder of the Seventies, the 2 oil shocks actually broken its financial system and pushed the yen down in order that by the early Eighties, with export surpluses returning, there was a declare, notably from the US, that the foreign money was undervalued.

The US has a historical past of blaming everybody else for his or her ills, though the commerce deficits they had been working ought to have been seen for what they had been – a useful actual phrases of commerce.

Because the Japanese commerce surpluses grew, there was clearly robust yen demand in worldwide foreign money markets however there have been offsetting components which prevented it from rising in worth in keeping with the rising surpluses.

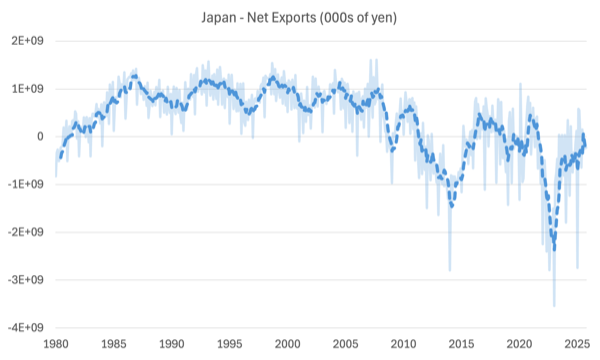

The next graph exhibits Japan’s web exports in opposition to the World (in 1000’s of yen) since January 1980 (to October 2025) – the Ministry of Finance publishes common – Commerce Statistics of Japan.

The info is month-to-month and I’ve light it and superimposed a 5-month transferring common (dotted line) to offer a clearer image of the pattern actions.

You may clearly see the rising surpluses within the late Seventies and into the Eighties.

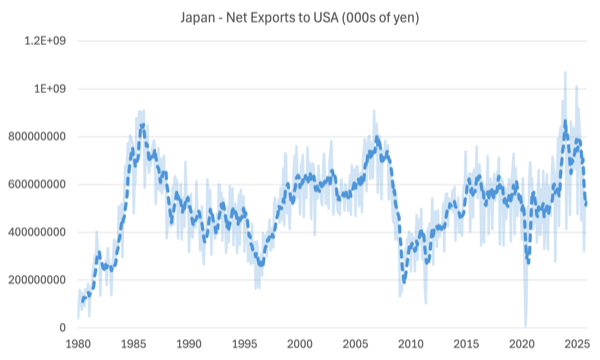

The following graph exhibits Japan’s web exports to the US over the identical interval.

A few of these offsetting components had been managed by the US – for instance, the upper US coverage rates of interest – which had been the work of US Federal Reserve boss Paul Volcker on the time.

Satirically, at the moment the IMF had been making an attempt to claim their neo-liberal stamp on world governments and along with its greatest ‘shareholder’ (the US authorities) they pushed closely for deregulation of capital flows between nations.

Because the restrictions on worldwide capital mobility had been relaxed, the big surpluses Japan had been accumulating courtesy of their commerce energy manifested in massive outflows on the Capital Account of its Steadiness of Funds because the Japanese pursued asset constructing alternatives in different currencies.

These web outflows thus diminished the surplus demand for the yen within the foreign-exchange market and that was the primary cause the yen didn’t respect regardless of the rising commerce surpluses.

However the US authorities was nonetheless obsessive about the notion that the yen (and different currencies) had been overvalued and that this was the primary cause for his or her persistent commerce deficits.

The mass consumption mentality of the US households was largely ignored on this debate.

Enter the so-called – Plaza Accord – duly named as a result of it was signed on the Plaza Resort in New York Metropolis.

The US was actually liable for the appreciating US greenback on the time.

Volcker’s charge rises and Reagan’s fiscal enlargement in 1981-84, created enticing funding alternatives within the US, which led to robust capital influx, which, in flip, pushed up the US greenback parity.

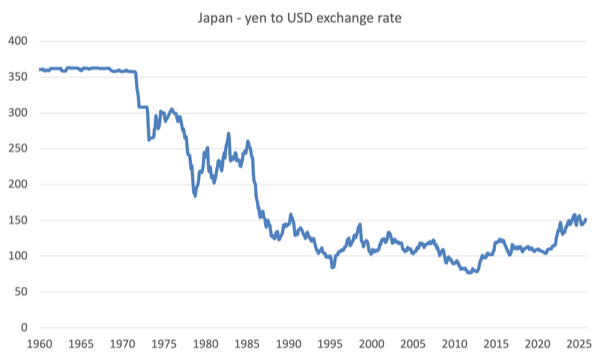

The next graph exhibits the historical past of the yen to USD change charge from January 1960 to October 2025.

The flat part (360 yen to the greenback) was the Bretton Woods parity imposed by the US occupation forces.

The yen appreciated sharply when the mounted change charge system was deserted.

Between October 1978 and the February 1985, the USD appreciated 41 per cent in opposition to the yen (with related actions in opposition to the Deutschmark, Franc and Pound).

By 1985, with the US greenback persevering with to understand and its commerce deficit rising, the US politicians shifted from opposing any organised foreign money realignment to actively supporting the notion.

There have been a number of forces pressuring the US authorities to withstand any organised depreciation.

1. The monetary markets had been benefiting from the upper greenback.

2. Reagan thought-about any reducing of the parity would jeopardise his anti-inflation marketing campaign.

Many massive US Producers demanded that they obtain safety from what they seen as hostile change charge actions.

But, as neoliberalism was now rife, the thought of reintroducing tariffs and import quotas (and different types of commerce safety) was thought-about to be ideologically unsound.

And the US President responded and cooked up a plan, which materialised because the Plaza Accord.

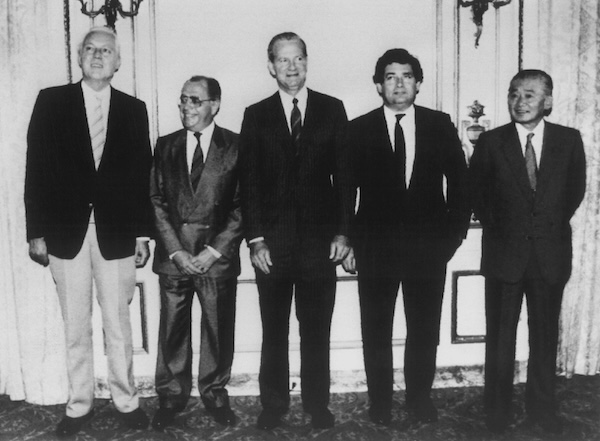

Conferences in early 1985 between the massive 5 nations (G5) agreed on some managed US depreciation.

The plans had been formalised on September 22, 1985, the place senior officers (Ministry of Finance and Central Banks) from France, Japan, West Germany, the US and the UK met and agreed to depreciate the US greenback in opposition to the yen and the mark.

The central banks would interact in official intervention in foreign-exchange markets to make sure the currencies moved within the route outlined within the Accord.

Whereas it was all smiles for the press (from left are Gerhard Stoltenberg of West Germany, Pierre Bérégovoy of France, James A. Baker III of america, Nigel Lawson of Britain, and Noboru Takeshita of Japan), the very fact is that the US bullied and coerced Japan into signing the Accord.

The Japanese financial system was lastly starting to ship materials prosperity to its inhabitants after years of wrestle following the disaster it introduced upon itself because of its aggression throughout World Struggle 2.

Officers knew that in the event that they bowed to US calls for to understand the foreign money it will successfully carry its development interval to a halt and curtail its export sector.

Nevertheless, the US insisted and threatened commerce litigation and restrictions in opposition to the Japanese exporters.

Historical past tells us that the depreciation of the US greenback in opposition to the Yen, whereas it made US manufactured items cheaper in world markets didn’t basically alter the commerce stability in opposition to Japan.

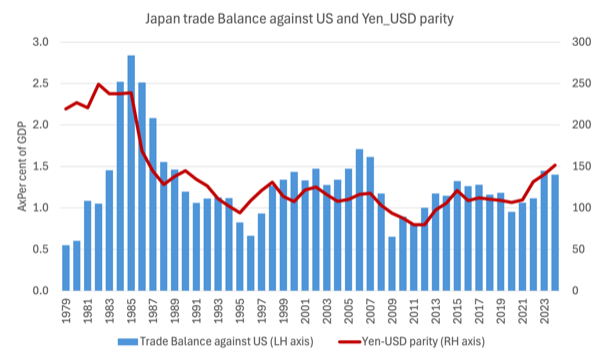

The next graph exhibits the evolution of the Japanese commerce stability (blue bars) with the US from 1979 to 2024 and it Yen/USD parity (purple line) over the identical interval (right-hand axis).

In 1985, the 239 Yen purchased $US1 and by 1988 the Yen had appreciated to 128 (a 46 per cent appreciation).

It’s clear that the bi-lateral commerce stability didn’t react very a lot in any respect.

The US Federal Reserve additionally diminished rates of interest to encourage a weakening of the USD.

There are debates about why that consequence occurred together with complaints by the US that Japan imposed import restrictions.

Probably the most salient cause was that the appreciating yen generated the – Endaka – a recession induced by an overvalued yen.

The response from the coverage makers to the lack of export competitiveness was to chop rates of interest and introduce a big fiscal enlargement to offset the lack of exports.

This was a comparatively massive stimulus and fuelled the asset worth bubbles in Japan’s monetary and actual property markets by means of the late Eighties.

The Financial institution of Japan lower charges by round 3 per cent and held the decrease charges by means of to 1989.

By 1987, the recession was gone and the financial system was booming once more.

The increase coincided with a interval of over-the-top neoliberal rest of banking guidelines which inspired wild hypothesis.

Nevertheless, the huge enlargement and liberating up of lending restrictions noticed important credit score development feeding into actual property costs (tripling between 1985 and 1989).

The – Japanese asset worth bubble – burst in spectacular trend in late 1991 (early 1992) following 5 years during which the actual property and share market boomed past perception.

The collapse in 1991-92 marked the start of what has been termed the – Misplaced Many years – which was marked by a pattern slowdown in financial development, deflation, and for the needs of this put up, cuts in actual wages as nominal wages stagnated.

Mainstream economists declare that the bubble and the burst had been as a consequence of extreme home stimulation slightly than something to do with the Plaza Accord.

However the reality is that the Plaza Accord intentionally undermined the Japanese financial system to learn the US lobbying pursuits.

The proof appears to help the view that it was not the macroeconomic stimulus that brought about the asset worth bubble however slightly it was the monetary deregulation within the Seventies and Eighties that was the wrongdoer.

The work of Takeo Hoshi and Anil Kashyap – Japan’s Monetary Disaster and Financial Stagnation – (revealed in 2004 within the Journal of Financial Views, 18(1), 3-26) famous that:

1. The neoliberal monetary deregulation allowed bigger firms to hunt funds from international capital markets.

2. The home banks shifted their lending to actual property loans main to an enormous rise in mortgage credit score.

3. Additional, there was a “aware coverage of Japanese banks to maintain extending credit score to corporations even when the prospects for being repaid are restricted.”

Additional, the yen appreciation, nonetheless, was not sufficient for the US.

Through the Seventies, Japan’s industrial ingenuity noticed it develop into the chief within the manufacturing of semiconductors, which it had declared to be a ‘precedence business’.

The – Semiconductor business in Japan – boomed because of cooperative preparations between business and the state.

The Japanese authorities offered important funding funds to increase the business.

By the Eighties, Japan produced round 50 per cent of the semiconductors on this planet and it turned a bigger business than the semiconductor sector within the US.

The US couldn’t hack that.

Japan was rising so quick and main the world in cutting-edge innovation that the paranoia within the US mounted.

The Japanese had been accused of commerce dumping – which simply mirrored the truth that the Japanese producers might produce higher merchandise at less expensive costs as a result of their productiveness was increased and their wages decrease.

The end result of those tensions was the 1986 US-Japan Semiconductor Commerce Settlement, which compelled Japan, underneath the specter of commerce restrictions from the US, to comply with restrict their exports of its semiconductors, improve their costs, and assure a particular US market share within the Japanese home market.

Historical past tells us that the US chip makers couldn’t cite any proof that they had been unable to promote into the home market in Japan.

It’s the identical argument as for motor autos.

The US producers have been unable to provide merchandise which can be enticing to Japanese shoppers and producers.

There are tales that the Japanese authorities, to keep away from expensive and damaging litigation that the US authorities had threatened in opposition to Japanese producers, required these producers to purchase US chips – which they did after which simply left them in storage as a result of they weren’t appropriate for his or her goal.

The US authorities additionally slapped 100 per cent tariffs on some Japanese reminiscence chips in 1987, additional damaging the Japanese export commerce.

It was no marvel that Japan’s share of the worldwide semiconductor market fell dramatically in subsequent years.

The economists who declare that the Financial institution of Japan ought to have tightened financial coverage to help the Plaza Accord targets not often point out the social instability that an entrenched recession would have created.

The Japanese shifted demand from exports to home demand, which was in keeping with the calls for of the US.

The issue although was that the US producers had been lower than the duty and their merchandise might achieve no important traction within the Japanese market.

Conclusion

That is on-going work as I analyse the impacts of Trump’s tariffs, notably on the Japanese motorcar business.

That’s sufficient for right now!

(c) Copyright 2025 William Mitchell. All Rights Reserved.