In a earlier put up, we documented how, over the previous 5 many years, the everyday U.S. financial institution has advanced from an entity primarily targeted on deposit taking and mortgage making to a extra diversified conglomerate additionally incorporating a wide range of nonbank actions. On this put up, we present that an vital driver of the evolution of this new organizational type is the will of banks to effectively handle liquidity wants.

Managing Liquidity Threat By way of Diversification

A particular trait of economic intermediaries is their publicity to liquidity threat. An influential educational paper demonstrated that banks can handle liquidity extra effectively by combining deposit-taking and credit-extension actions. That is because of the imperfect correlation between liquidity calls for from surprising deposit withdrawals and altering credit score wants, enabling the financial institution to carry fewer total liquid property, relative to 2 entities every specializing in deposits and lending.

This theoretical framework, initially utilized to a conventional financial institution, can also be related to fashionable, diversified U.S. banking companies working as financial institution holding firms (BHCs) with each financial institution and nonbank subsidiaries. When financial institution and nonbank associates of BHCs face liquidity outflows which can be comparatively uncorrelated, the BHCs can afford to carry decrease liquidity buffers relative to unbiased, separate entities specializing in these actions. In different phrases, by diversifying throughout financial institution and nonbank actions, BHCs economize on their liquidity holdings and optimize the administration of their liquidity dangers. Per this concept, our examine, “The Nonbank Footprint of Banks,” exhibits that banking companies with a extra in depth nonbank presence can higher handle their liquidity wants.

Financial institution and Nonbank Subsidiaries Present Mutual Liquidity Assist

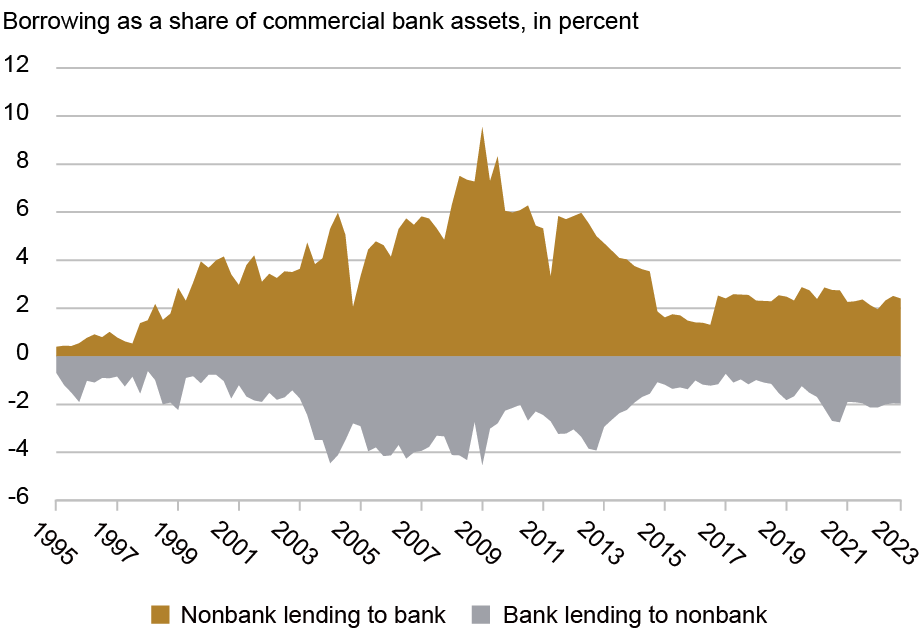

If financial institution and nonbank subsidiaries function in a means that helps each other’s liquidity wants, then we should always observe a big quantity of intracompany borrowing and lending between affiliated banks and nonbanks. The chart under studies such intracompany transfers, aggregated for your entire U.S. banking trade. The realm above the horizontal axis exhibits what share of business financial institution property are funded with intracompany borrowing from affiliated nonbanks (gold space). The realm under the horizontal axis shows the extent of lending by business financial institution subsidiaries (“detrimental” borrowing) to affiliated nonbanks (grey space). The extent of those intracompany transfers varies over time, averaging about 5 % of financial institution subsidiaries’ complete property. These numbers are economically important, offering adequate proof to corroborate the idea of lively liquidity assist between financial institution and nonbank subsidiaries.

Intensive Borrowing and Lending Between Affiliated Banks and Nonbanks

Notes: This chart plots intracompany borrowing and lending for business financial institution subsidiaries as a share of property utilizing a balanced panel of financial institution holding firms from 1995 to 2022. The gold space above the horizontal axis exhibits what share of business financial institution property are funded with intracompany borrowing from affiliated nonbanks. The grey space under the axis shows the extent of lending by business financial institution subsidiaries to affiliated nonbanks.

Subsidiaries Fund Every Different in Occasions of Stress

The existence of intracompany transactions doesn’t show per se that BHCs broaden their nonbank footprints as a deliberate liquidity technique. For instance, the flows may very well be as a result of operational comfort, like a nonbank affiliate depositing surplus money with its financial institution sibling. So, subsequent, we examine whether or not inside funding will increase during times of heightened want.

To raised perceive the drivers of intracompany transfers, we checked out a selected occasion by which business banks had completely different ranges of publicity to a liquidity shock: In the summertime of 2007, asset-backed business paper (ABCP) conduits skilled misery. Some business banks had been vital sponsors of such conduits, and so on the time of misery, these banks confronted important liquidity wants. We then ran the next experiment: we in contrast two units of banks, all in BHCs with an analogous nonbank footprint, however one set was extremely uncovered to the ABCP misery whereas the opposite was not. Based on our prior, we should always have noticed the primary set of banks improve its borrowing from the nonbank associates—and that is precisely what we discovered.

What’s extra, those self same banks borrowed much less from the Federal Reserve’s emergency liquidity amenities, indicating that the supply of funding from the nonbank associates decreased the necessity for official-sector assist. A back-of-the-envelope calculation signifies that funding from nonbank associates decreased borrowing from the Fed by about $176 billion—a big quantity, contemplating that complete borrowings from the Federal Reserve peaked at about $700 billion in 2008.

Do BHCs Create Nonbank Subsidiaries to Profit from Liquidity Synergies?

A testable prediction of the liquidity synergy motive is {that a} BHC’s nonbank operations can be sized in response to the worth of liquidity provision by these nonbank associates. Particularly, if inside liquidity sharing is a key motivation for integrating nonbanks right into a BHC, then a diminished worth of this “insurance coverage” ought to immediate a BHC to cut back its nonbank footprint. Conversely, if the nonbank footprint is unrelated to liquidity insurance coverage, its decreased worth mustn’t lead to adjustments to the BHC’s organizational construction.

We take a look at this prediction by analyzing the impact of a regulatory “shock” that considerably decreased the worth of partaking in inside funding transactions between financial institution and nonbank associates of BHCs. Particularly, as a part of the Dodd-Frank Act, a subset of BHCs grew to become topic to the so-called “residing wills” mandate, which requires detailing their decision plans within the occasion of failure. Crucially, the regulation explicitly discouraged funding interdependence between financial institution and nonbank subsidiaries, thus representing an exogenous (detrimental) shock to the worth of inside funding.

BHCs internalized this decrease worth. As an illustration, in its 2015 plans, Goldman Sachs wrote that it had “devoted substantial assets to decreasing … the variety of inside transactions which switch threat and positions from one GS Group entity to a different.” Equally, J.P. Morgan wrote in its 2019 plans: “Amongst different enhancements, we … executed actions to simplify materials intercompany funding relationships and scale back interconnectedness.”

We look at how a BHC’s nonbank footprint modified within the quarters and years after the residing wills regulation, by evaluating BHCs that had been topic to the regulation with those who weren’t. The outcomes are displayed within the chart under, for 4 distinct measures of a BHC’s nonbank footprint: the property of nonbank subsidiaries as a share of complete BHC property; the variety of nonbank subsidiaries; the variety of distinctive nonbank enterprise traces; and the dimensions of intracompany funding flows between banks and nonbanks. The BHCs topic to the regulatory “therapy” exhibited a marked lower in every of those 4 measures after the regulation (the purple line within the charts), with respect to a “management” group (the blue line within the charts). This end result suggests {that a} BHC’s incentive to eliminate nonbank subsidiaries is carefully tied to the worth of the liquidity offered by these subsidiaries.

Financial institution Holding Corporations Cut back Their Nonbank Footprints Following “Residing Wills” Mandate

Distinctive Nonbank Actions

Log Intercompany Balances

Supply: Authors’ calculations.

Notes: The chart plots the trajectories of the result variables for the therapy group and for the artificial management group related to every consequence. To make parallel developments extra obvious, there’s a vertical shift of the artificial management trajectory in order that the pre-treatment trajectories of the artificial management and the therapy are overlaid on high of one another. The vertical line corresponds to 2011:Q3, which is the ultimate “pre-treatment” interval earlier than residing wills had been introduced in 2011:This fall.

Remaining Ideas

Because the Nineteen Eighties, BHCs have built-in hundreds of nonbank monetary establishments into their operations, transferring past conventional depository and lending providers. Our examine paperwork this growth, implying that the textbook mannequin of a business financial institution is outdated. This truth presents a brand new perspective on the evolution of economic intermediation and the rise of nonbanks, revealing that a good portion of this development has occurred inside the boundaries of U.S. banking companies.

Our evaluation signifies that environment friendly liquidity administration is a core driver of economic intermediation as BHCs purchase or shed nonbank subsidiaries primarily based on their liquidity providers. This means that rules that limit banks’ actions are more likely to shift intermediation towards nonbank entities outdoors the banking perimeter. Paradoxically, banks themselves play an important function in enabling this shift, by supplying liquidity to unaffiliated nonbanks, as proven in earlier posts (right here, right here, and right here). The broad takeaway is that, even when rules can set up clear authorized boundaries between banks and nonbanks, they might fail at separating them operationally. Dangers that had been supposed to be faraway from the banking sector might merely resurface in a distinct and extra advanced type.

Nicola Cetorelli is head of Monetary Intermediation within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Saketh Prazad is a former analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The way to cite this put up:

Nicola Cetorelli and Saketh Prazad, “Banks Develop a Nonbank Footprint to Higher Handle Liquidity Wants,” Federal Reserve Financial institution of New York Liberty Avenue Economics, November 18, 2025, https://doi.org/10.59576/lse.20251118b

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).