A 2012 Liberty Road Economics submit famous that U.S. financial coverage displays a stunning diploma of seasonal conduct: over the 1987-2008 interval, the Federal Reserve was more likely to decrease rates of interest (or abstain from elevating charges) within the first month of every quarter than within the two subsequent months. 13 years later, we revisit that evaluation to research whether or not the seasonal sample in financial coverage nonetheless holds at this time, within the wake of a fee mountaineering cycle, a pandemic, a surge in inflation, and a second spherical of fee hikes. We discover that the sample has certainly continued; nonetheless, not like within the earlier pattern interval, it may be utterly defined by the timing of the FOMC calendar.

A Seasonal Sample in FOMC Selections

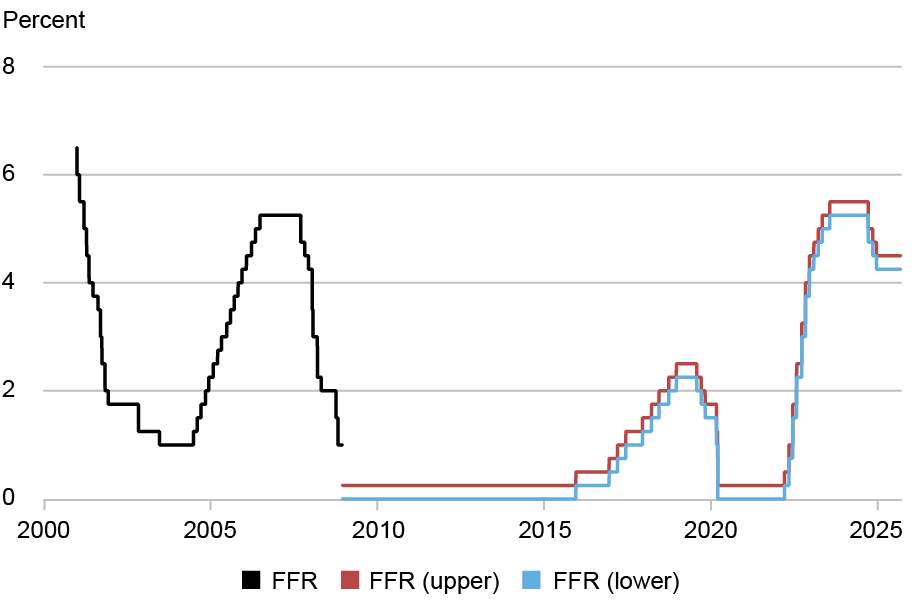

On this submit, we give attention to a twenty-five-year pattern interval: January 2000 to July 2025. Be aware that earlier than October 2008—the endpoint of the interval coated within the earlier submit—the FOMC carried out financial coverage by asserting a goal for the federal funds fee (FFR or funds fee). After October 2008, the FOMC carried out coverage by speaking a goal vary for the funds fee.

As proven within the chart under, since 2008, the funds fee spent six years on the zero decrease sure, earlier than a reasonable mountaineering cycle within the late 2010s, one other return to the zero decrease sure through the COVID pandemic, and a a lot steeper mountaineering cycle beginning in 2022. Whereas the funds fee declined by round 600 foundation factors over the twenty-five-year interval studied within the 2012 weblog submit, it solely declined, on web, by 125-150 foundation factors since 2000.

Financial Coverage Easing and Tightening Cycles over the Previous 25 Years

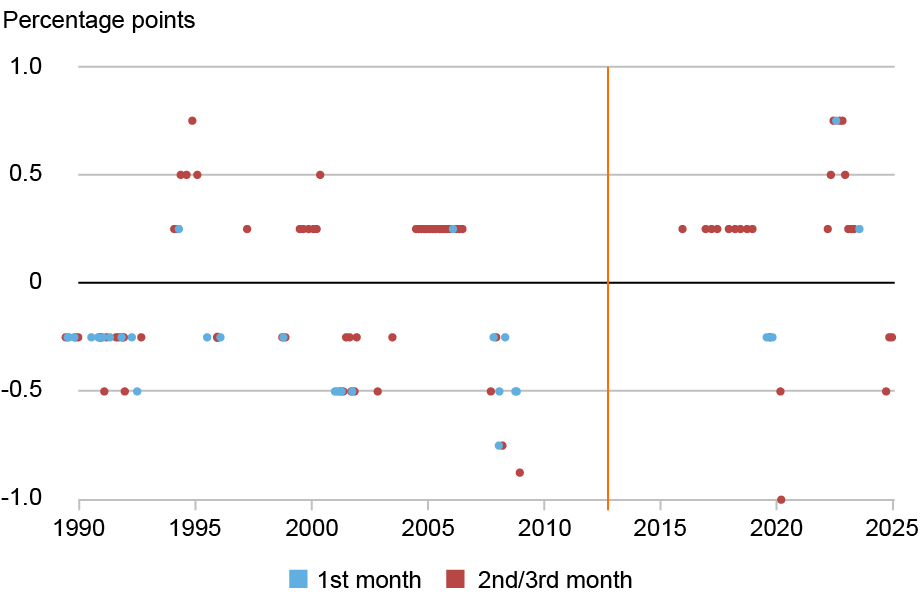

Regardless of the notable occasions which have occurred since 2012, surprisingly, we discover that adjustments within the funds fee have exhibited basically the identical seasonal conduct over the previous twenty-five years as they did over the 1987-2008 interval. This sample is illustrated within the chart under, which exhibits the upward and downward adjustments within the goal federal funds fee made at every assembly for the reason that late Eighties (we embrace unscheduled conferences with fee adjustments however exclude conferences with no change within the goal fee).

We are able to see that conferences held within the first month of 1 / 4 (blue dots) are over-represented when there are decreases within the goal fee (i.e., damaging values within the chart) and under-represented when there are will increase within the goal fee. Moreover, this sample broadly persists after October 2012, when the unique weblog submit was revealed (marked by a vertical line). Most strikingly, there are a lot of extra crimson dots than blue dots within the prime proper space of the chart—current tightening of coverage virtually all the time occurred in both the second or third month of the quarter.

Modifications within the Federal Funds Goal: 1st Month of a Quarter versus 2nd/third Months

Be aware: The orange vertical line marks the discharge (October 2012) of the unique Liberty Road Economics submit on seasonality in financial coverage.

We are able to make this level extra exactly by accumulating these adjustments for every calendar yr. The desk under exhibits the full proportion level change within the federal funds fee goal for FOMC conferences within the first month of the quarter (January, April, July, and October), in contrast with the full change over the remaining eight months of the yr (we omit years wherein there was no change within the goal funds fee). The funds fee declined by 4 proportion factors, in complete, throughout conferences within the first month of every quarter since 2000. Throughout conferences within the remaining eight months of every yr, the funds fee elevated by virtually 3 proportion factors. For the reason that authentic weblog submit was revealed in 2012, the funds fee elevated by 50 foundation factors within the first month of the quarter however rose by 375 foundation factors in all different months. Thus, the seasonal sample seems to be intact.

Annual Modifications within the Federal Funds Goal: 1st Month versus 2nd/third Months

| Yr | Complete Change | 1st Month of Quarter | 2nd/third Months of Quarter |

| 2000 | 1.00 | 0.00 | 1.00 |

| 2001 | -4.75 | -2.00 | -2.75 |

| 2002 | -0.50 | 0.00 | -0.50 |

| 2003 | -0.25 | 0.00 | -0.25 |

| 2004 | 1.25 | 0.00 | 1.25 |

| 2005 | 2.00 | 0.00 | 2.00 |

| 2006 | 1.00 | 0.25 | 0.75 |

| 2007 | -1.00 | -0.25 | -0.75 |

| 2008 | -4.13 | -2.50 | -1.63 |

| 2015 | 0.25 | 0.00 | 0.25 |

| 2016 | 0.25 | 0.00 | 0.25 |

| 2017 | 0.75 | 0.00 | 0.75 |

| 2018 | 1.00 | 0.00 | 1.00 |

| 2019 | -0.75 | -0.50 | -0.25 |

| 2020 | -1.50 | 0.00 | -1.50 |

| 2022 | 4.25 | 0.75 | 3.50 |

| 2023 | 1.00 | 0.25 | 0.75 |

| 2024 | -1.00 | 0.00 | -1.00 |

| Complete | -1.13 | -4.00 | 2.88 |

| Since 2012 | 4.25 | 0.50 | 3.75 |

As mentioned within the authentic submit, this stunning consequence may very well be a matter of coincidence, with the schedule of FOMC conferences falling right into a sure alignment with the timing of mountaineering and easing cycles. Over the 1987-2008 interval, there occurred to be extra FOMC conferences within the first month of every quarter during times when the fed funds goal was falling, in comparison with durations when the speed was rising. For instance, in 2005—through the 2004-2006 tightening cycle—there have been no FOMC conferences held within the first month of the quarter. The prior weblog submit, nonetheless, discovered that eradicating years wherein there have been significantly few or many FOMC conferences scheduled within the first month of every quarter didn’t get rid of the statistical and financial significance of the seasonal variations.

Right here, we examine this problem in a barely completely different approach. For every year, we calculate the full change within the funds fee. We then think about a counterfactual world wherein this complete change was distributed evenly throughout the FOMC conferences that occurred in that yr, taking the schedule of conferences as given (we embrace unscheduled conferences the place a change within the goal funds fee occurred). The outcomes are proven within the desk under.

Counterfactual Annual Modifications within the Federal Funds Goal:

1st Month versus 2nd/third Months

| Yr | Complete Change | 1st Month of Quarter | 2nd/third Month of Quarter |

| 2000 | 1.00 | 0.12 | 0.88 |

| 2001 | -4.75 | -1.73 | -3.02 |

| 2002 | -0.50 | -0.06 | -0.44 |

| 2003 | -0.25 | -0.06 | -0.19 |

| 2004 | 1.25 | 0.16 | 1.09 |

| 2005 | 2.00 | 0.00 | 2.00 |

| 2006 | 1.00 | 0.25 | 0.75 |

| 2007 | -1.00 | -0.25 | -0.75 |

| 2008 | -4.12 | -2.06 | -2.06 |

| 2015 | 0.25 | 0.12 | 0.12 |

| 2016 | 0.25 | 0.09 | 0.16 |

| 2017 | 0.75 | 0.09 | 0.66 |

| 2018 | 1.00 | 0.12 | 0.88 |

| 2019 | -0.75 | -0.28 | -0.47 |

| 2020 | -1.50 | -0.50 | -1.00 |

| 2022 | 4.25 | 1.06 | 3.19 |

| 2023 | 1.00 | 0.12 | 0.88 |

| 2024 | -1.00 | -0.25 | -0.75 |

| Complete | -1.13 | -3.06 | 1.93 |

| Since 2012 | 4.25 | 0.57 | 3.67 |

On this counterfactual world, the totality of fee adjustments over 2000-2024 resulted in a 306 foundation level decline within the first month of the quarter and an increase of 193 foundation factors in all different months. This can be a differential of about 5 proportion factors, as in comparison with 6.88 proportion factors within the desk above. Thus, whereas the timing of FOMC conferences can account for a big fraction of the seasonality noticed over this complete interval, there’s nonetheless virtually 200 foundation factors that isn’t defined by timing.

In distinction, since 2012 the counterfactual path of adjustments within the funds fee is sort of precisely the identical because the historic path proven within the desk above. In actuality, there was a complete enhance of fifty foundation factors within the first month of the quarter as in comparison with a rise of 57 foundation factors within the counterfactual train. In all different months there was an increase of three.75 proportion factors as in comparison with 3.67 proportion factors within the counterfactual train. This means that the seasonal sample we have now noticed since 2012 is actually defined in full by the timing of FOMC conferences alone. Thus, beneath additional scrutiny, we are able to conclude that the “extra seasonality” famous within the authentic submit doesn’t seem to have endured past 2012.

Richard Okay. Crump is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Keshav Dogra is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Dennis Kongoli is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this submit:

Richard Crump, Keshav Dogra, and Dennis Kongoli, “Is Financial Coverage Nonetheless Seasonal? ,” Federal Reserve Financial institution of New York Liberty Road Economics, November 19, 2025, https://doi.org/10.59576/lse.20251119

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).